Are you looking for a simple and effective way to grow your wealth over the long term? Look no further than index funds. These low-cost investments track a specific market index, such as the S&P 500, providing you with diversified exposure to a wide range of companies. Investing in index funds is a popular strategy for both seasoned investors and those just starting their financial journey. By understanding the basics of index fund investing and following a few key steps, you can unlock the potential for long-term growth and achieve your financial goals.

This comprehensive guide will walk you through the fundamentals of index fund investing, from choosing the right funds to building a diversified portfolio. We’ll delve into the benefits and risks associated with this approach, providing you with the knowledge and confidence to make informed decisions. Whether you’re a beginner investor or simply seeking to expand your investment horizons, this article will equip you with the tools and insights needed to navigate the world of index funds and harness their power for long-term success.

Understanding Index Funds and Their Benefits

Index funds are a type of mutual fund or exchange-traded fund (ETF) that tracks the performance of a specific market index, such as the S&P 500 or the Nasdaq 100. Instead of trying to beat the market by actively picking stocks, index funds aim to match the returns of their underlying index. This passive investment approach offers several key benefits for long-term investors.

Diversification: Index funds provide broad diversification by investing in a wide range of companies within the index. This helps to mitigate risk by reducing the impact of any single company’s performance on your overall portfolio.

Low Costs: Index funds are known for their low expense ratios, which are the annual fees charged to manage the fund. Lower costs mean more of your investment goes towards generating returns.

Transparency: Index funds are highly transparent, as their holdings are publicly disclosed and closely track the underlying index. Investors can easily understand the composition of the fund and how it aligns with their investment goals.

Long-Term Growth Potential: By tracking the performance of a broad market index, index funds offer the potential for long-term growth aligned with the overall market.

Overall, index funds provide a simple, cost-effective, and diversified way to invest in the stock market. Their passive approach and focus on long-term growth make them a suitable choice for investors seeking to build wealth over time.

Choosing the Right Index Funds for Your Goals

Index funds are a great way to invest for the long term, as they offer diversification and low costs. But with so many index funds to choose from, how do you pick the right ones for your goals?

Here are a few factors to consider:

- Your investment goals: Are you saving for retirement, a down payment on a house, or your children’s education? Understanding your goals will help you determine the right time horizon for your investments and the level of risk you’re comfortable with.

- Your risk tolerance: Are you comfortable with the potential for greater returns, but also the possibility of greater losses? Or do you prefer to minimize risk, even if it means lower potential returns? Your risk tolerance will influence the types of index funds you invest in.

- Investment time horizon: How long do you plan to invest your money? Generally, the longer your time horizon, the more risk you can take on. If you’re investing for the long term, you may be able to invest in more volatile index funds.

- Investment strategy: Do you want to invest in a diversified portfolio of index funds, or do you want to focus on specific sectors or industries? Your investment strategy will determine the specific index funds you choose.

- Fees: Index funds generally have low fees, but there are still differences in expense ratios. Choose index funds with low expense ratios to maximize your returns.

Once you’ve considered these factors, you can start to narrow down your choices. There are many different types of index funds available, including:

- Broad market index funds: These track a broad market index, such as the S&P 500 or the Nasdaq 100.

- Sector-specific index funds: These track a specific sector of the market, such as technology, healthcare, or energy.

- International index funds: These track international markets, such as the MSCI EAFE Index.

- Bond index funds: These track a variety of bond indexes, such as the Barclays Aggregate Bond Index.

By choosing the right index funds for your goals, you can create a diversified and cost-effective portfolio that can help you reach your financial goals.

Determining Your Investment Time Horizon

Before you even think about selecting index funds, you must determine your investment time horizon, which is the length of time you plan to keep your money invested. This is crucial for making informed investment decisions and choosing the right strategy for your goals.

Your time horizon dictates your risk tolerance. A longer time horizon allows for greater risk-taking, as you have more time to recover from potential market downturns. Conversely, a shorter time horizon requires a more conservative approach, as you’ll have less time to make up for losses.

For example, if you’re investing for retirement decades away, you can afford to be more aggressive and invest in funds with higher growth potential, even if they come with higher volatility. On the other hand, if you’re saving for a down payment on a house in a few years, you’ll need to prioritize stability and choose funds with lower risk profiles.

To determine your time horizon, consider your financial goals, your age, and your risk tolerance. Once you have a clear understanding of your time horizon, you can start researching index funds that align with your investment objectives.

Opening a Brokerage Account

Before you can start investing in index funds, you’ll need to open a brokerage account. A brokerage account allows you to buy and sell securities, including index funds. There are many different brokerage firms to choose from, so it’s important to compare features, fees, and investment options before making a decision.

Here are some factors to consider when choosing a brokerage firm:

- Fees: Brokerage firms charge fees for various services, such as trading commissions, account maintenance fees, and inactivity fees. Some firms offer commission-free trading for certain types of investments, including index funds.

- Investment options: Make sure the brokerage firm offers the index funds you want to invest in. Some firms have a limited selection of index funds, while others offer a wide range of options.

- Research tools: Some brokerage firms provide research tools that can help you make informed investment decisions. These tools may include market data, stock quotes, and analyst reports.

- Customer service: It’s important to choose a brokerage firm with good customer service. You should be able to easily contact a representative if you have any questions or need assistance.

Once you’ve chosen a brokerage firm, you’ll need to open an account. The process typically involves providing personal information, such as your name, address, and Social Security number. You may also need to provide proof of identity and residency. Some brokerage firms require a minimum deposit to open an account.

Researching and Selecting an Index Fund

After deciding to invest in index funds, you need to do your research to find the right ones for your portfolio. There are several factors to consider, such as the index the fund tracks, the fund’s expense ratio, and the fund’s performance history.

One of the most important factors to consider is the index the fund tracks. There are many different types of indexes, each with its own investment focus. For example, some indexes track the performance of the entire stock market, while others track specific sectors, industries, or asset classes. You should choose an index that aligns with your investment goals and risk tolerance.

Another important factor to consider is the fund’s expense ratio. This is the annual fee charged by the fund manager to cover the costs of running the fund. A lower expense ratio means that you’ll pay less in fees, which can make a big difference in your returns over time.

Finally, it’s important to consider the fund’s performance history. Past performance is not a guarantee of future results, but it can give you an idea of how the fund has performed in the past. Look for funds that have a consistent track record of strong performance.

When researching and selecting an index fund, it’s important to use a combination of resources, including financial websites, brokerage platforms, and financial advisors. This can help you get a comprehensive understanding of the different index funds available and make an informed decision about which one is right for you.

Making Your Initial Investment

The first step in investing in index funds is deciding how much you want to invest. There’s no magic number, and it’s important to choose an amount that is comfortable for you and aligns with your financial goals. Consider your income, expenses, and savings goals when making your decision.

Start small if you’re new to investing. You can gradually increase your contributions as you become more comfortable with the process. Investing regularly, even small amounts, can help you build wealth over time thanks to the power of compounding.

You’ll also need to choose the index fund you want to invest in. This involves considering your investment goals and risk tolerance. For instance, if you’re aiming for long-term growth, you might prefer a broad market index fund like the S&P 500 or the total stock market. There are also index funds focused on specific sectors, like technology or healthcare.

Once you’ve selected your index fund, you’ll need to open an investment account with a brokerage firm. Many reputable online brokerages offer commission-free index fund trading, making it more affordable to start investing. Make sure to research and choose a firm that aligns with your needs and investment goals.

Finally, you’ll need to actually purchase shares of the index fund. Most online brokerages allow you to buy and sell index funds quickly and easily. You can choose to invest a lump sum or set up automatic recurring investments to build your portfolio over time.

Developing a Consistent Investment Strategy

Investing in index funds is a great way to achieve long-term growth, but it’s crucial to have a consistent investment strategy. A well-defined strategy provides structure and helps you stay disciplined in your investment journey. Here’s how to develop one:

1. Define Your Financial Goals: Start by clearly outlining what you aim to achieve through investing. Are you saving for retirement, a down payment on a house, or a child’s education? Defining your goals will guide your investment decisions and timeline.

2. Determine Your Risk Tolerance: How comfortable are you with market fluctuations? A higher risk tolerance might allow you to invest in more volatile index funds, while a lower risk tolerance might favor more conservative options. Understand your risk profile to make informed choices.

3. Establish a Time Horizon: How long do you plan to invest? A longer time horizon allows you to ride out market fluctuations and benefit from compounding returns. Consider your financial goals and adjust your investment strategy accordingly.

4. Set Up Automatic Investments: Automation is key to consistency. Setting up regular contributions to your index funds, even small amounts, will help you build a strong foundation over time. This disciplined approach avoids impulsive decisions and keeps you on track.

5. Review and Adjust Regularly: Your investment strategy isn’t set in stone. As your life circumstances change, you may need to review and adjust your goals, risk tolerance, or investment allocation. Regular review helps ensure your strategy remains aligned with your evolving needs.

Understanding Expense Ratios and Their Impact

When investing in index funds, you’re essentially buying a basket of securities that tracks a specific market index, like the S&P 500. While index funds are generally considered low-cost investment options, it’s crucial to understand the concept of expense ratios and their impact on your returns.

An expense ratio represents the annual fee charged by the fund manager for managing the fund. It’s expressed as a percentage of the fund’s assets under management (AUM). For example, an expense ratio of 0.50% means that the fund manager will take 0.50% of your investment each year to cover their operational costs, including administration, trading, and research.

While expense ratios may seem small, they can have a significant impact on your long-term returns. Over time, even a small difference in expense ratios can compound and result in a substantial difference in your overall investment growth. Imagine two index funds, both tracking the same index, but one with an expense ratio of 0.10% and the other with 0.50%. Over a 30-year period, the fund with the lower expense ratio could significantly outperform the higher-cost fund, even with identical market performance.

When selecting index funds, always compare expense ratios to find the most cost-effective options. Generally, lower expense ratios are more beneficial, but remember to consider other factors like the fund’s track record, liquidity, and investment strategy. By prioritizing low-cost funds with reasonable fees, you can maximize your potential returns and achieve long-term financial goals.

Benefits of Dollar-Cost Averaging

Dollar-cost averaging (DCA) is a popular investment strategy that involves investing a fixed amount of money at regular intervals, regardless of the market’s current price. This approach can be particularly beneficial for long-term investors, especially those who are new to investing or lack the time or expertise to actively manage their portfolio.

Here are some key benefits of DCA:

- Reduces the impact of market volatility: DCA helps to smooth out the ups and downs of the market by averaging your purchase price over time. This can help you avoid buying high and selling low, which is a common mistake among investors.

- Disciplined investing: DCA encourages a disciplined approach to investing by requiring you to invest regularly, even when the market is down. This can help you stay on track with your investment goals over the long term.

- Less stress: DCA can help reduce the stress associated with investing by eliminating the need to constantly monitor the market and make timing decisions.

- Easier to manage: DCA simplifies the investing process by removing the need to make complex buy and sell decisions. This can be especially helpful for busy individuals who lack the time or expertise to actively manage their portfolio.

It’s important to note that DCA is not a guaranteed path to success. The market can go up or down over the long term, and there is always the risk of loss. However, DCA can be a valuable tool for long-term investors looking to build wealth steadily over time.

Staying Consistent for Long-Term Growth

Consistency is key to achieving long-term growth with index funds. The stock market is volatile, with ups and downs in the short term. But over the long term, the market has historically trended upwards. This means that if you stay invested, you’ll likely see your investment grow over time, even if you experience some short-term losses.

To stay consistent, you need to have a long-term investment plan and stick to it. Don’t let emotions like fear or greed dictate your investment decisions. Instead, focus on your goals and the long-term potential of your investments. This means buying and holding your index funds for a significant period of time, even if the market experiences short-term fluctuations.

One strategy for consistent investing is dollar-cost averaging. This involves investing a fixed amount of money in your index fund at regular intervals, regardless of the market’s current performance. This helps you avoid trying to time the market and ensures that you are investing consistently over time.

Consistency is not just about your investment strategy, but also about your mindset. You need to be patient and disciplined, understanding that long-term growth takes time. Avoid chasing short-term gains and be prepared for some bumps along the way. This will help you stay invested for the long haul and maximize your returns.

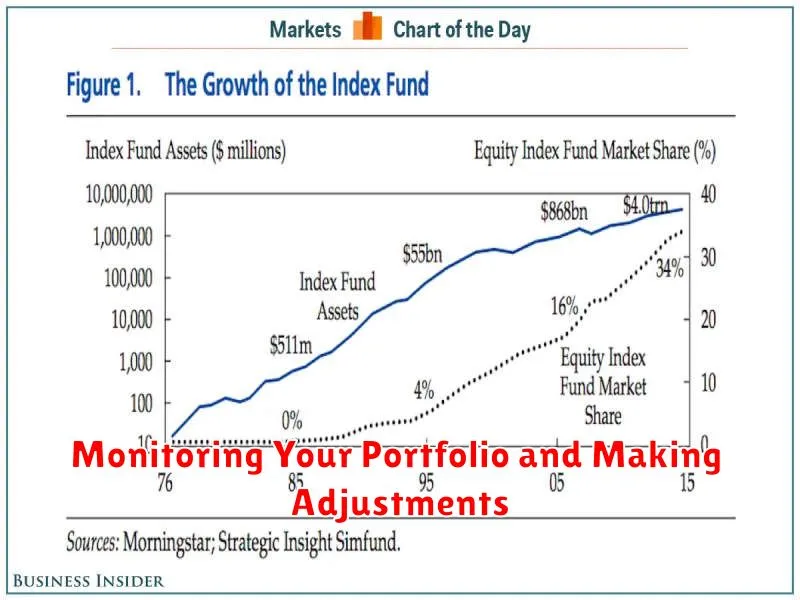

Monitoring Your Portfolio and Making Adjustments

While index funds are designed for long-term growth, it’s crucial to periodically monitor your portfolio and make adjustments as needed. This involves reviewing your investment goals, risk tolerance, and overall market conditions.

One aspect to consider is your asset allocation. As time passes, the mix of your assets may drift away from your original plan. For example, if you started with a 80% stock and 20% bond allocation, market fluctuations might shift this balance. Regularly rebalancing your portfolio ensures it aligns with your intended risk profile.

You should also be aware of market cycles and how they might impact your investments. While the long-term trend of the stock market is generally upward, short-term fluctuations are inevitable. If the market experiences a significant downturn, you might consider adjusting your allocation to a more conservative strategy to protect your capital.

Lastly, it’s important to periodically review your investment goals. As your circumstances change, so might your financial aspirations. For instance, if you’re nearing retirement, you might consider shifting to a more conservative investment strategy to preserve your savings.

By regularly monitoring your portfolio and making necessary adjustments, you can stay on track towards your long-term financial goals. Remember, investing in index funds is a marathon, not a sprint. Patience and discipline are key to achieving success.

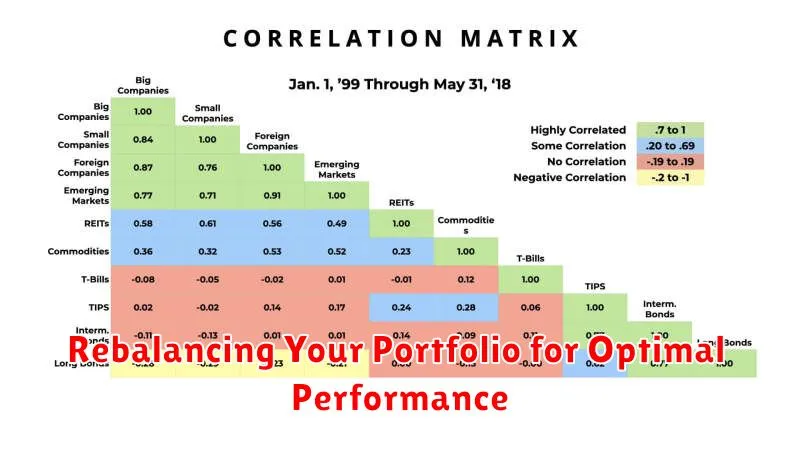

Rebalancing Your Portfolio for Optimal Performance

Rebalancing is an essential part of long-term investing with index funds, especially as your portfolio grows and market conditions change. It involves adjusting your asset allocation back to your original target percentages. This helps maintain your desired risk level and ensures your portfolio remains diversified.

The goal of rebalancing is to capture profits from investments that have outperformed and to reduce risk by reinvesting in underperforming sectors. Imagine your portfolio is a pie chart, with different slices representing different asset classes like stocks, bonds, and real estate. As the market fluctuates, the size of these slices may change, disrupting your original allocation.

Rebalancing involves buying more of the underperforming assets and selling some of the overperforming ones, bringing the pie chart back to its original proportions. This allows you to take advantage of potential future gains in the underperforming sectors while mitigating risk by reducing your exposure to the overperforming ones.

The frequency of rebalancing depends on your individual investment strategy and risk tolerance. Some investors choose to rebalance annually, while others do it quarterly or even monthly. It’s recommended to review your portfolio at least once a year and rebalance if necessary. Remember, a well-rebalanced portfolio helps you stay on track towards your long-term financial goals.

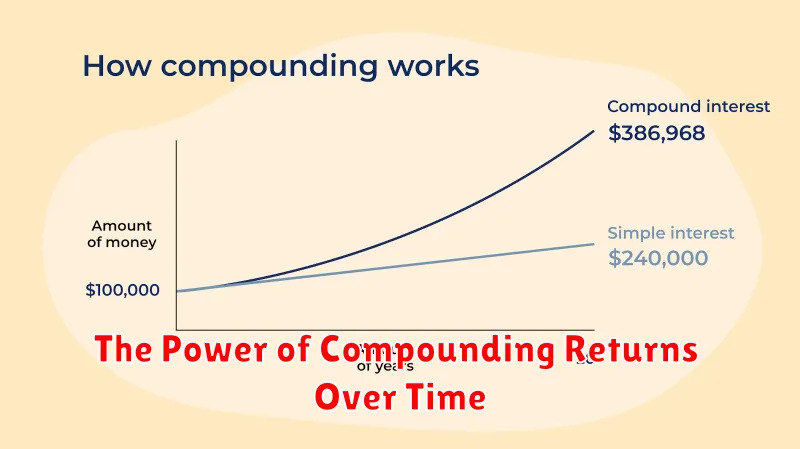

The Power of Compounding Returns Over Time

Index funds are a great way to invest for the long term. They offer diversification, low fees, and the potential for strong returns. But perhaps the most important factor in index fund investing is the power of compounding returns.

Compounding is the process of earning interest on your investment, and then earning interest on that interest. It’s like a snowball rolling downhill, getting bigger and bigger over time. The earlier you start investing and the longer you stay invested, the more time your money has to compound.

For example, let’s say you invest $10,000 in an index fund that earns an average annual return of 10%. After one year, your investment will be worth $11,000. In year two, you’ll earn 10% on $11,000, which is $1,100. So, your investment will be worth $12,100. And so on. As you can see, the power of compounding can make a big difference over time.

The earlier you start investing, the more time your money has to compound. The key is to invest consistently over time and let compounding do its magic. Even small amounts of money can grow into significant sums over time.

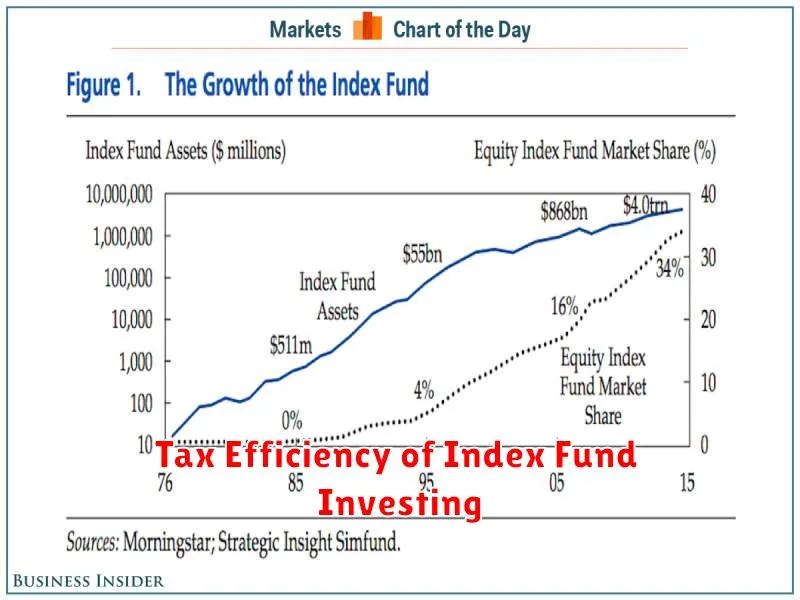

Tax Efficiency of Index Fund Investing

Index funds are known for their low expense ratios, but they also offer significant tax advantages over actively managed funds. This tax efficiency stems from their passive investment approach, which minimizes trading activity and, consequently, taxable events.

Lower Turnover Rates: Index funds aim to mirror a specific market index, such as the S&P 500, which generally involves minimal trading. Actively managed funds, on the other hand, frequently buy and sell securities in an attempt to outperform the market. This constant trading generates more taxable capital gains distributions for investors in actively managed funds.

Tax-Loss Harvesting Opportunities: Since index funds are broadly diversified, they offer opportunities for tax-loss harvesting. This strategy involves selling losing investments to offset capital gains, thereby reducing your overall tax liability. Actively managed funds, with their concentrated portfolios, may limit these opportunities.

Tax-Efficient Distributions: Index funds typically distribute dividends and capital gains less frequently than actively managed funds. This can be advantageous for investors seeking to minimize their tax obligations. The infrequent distributions also provide more flexibility for investors to manage their tax liability throughout the year.

Long-Term Growth: The tax efficiency of index funds contributes to their long-term growth potential. By minimizing taxable events, more of your investment returns are reinvested, compounding over time. This is particularly beneficial in tax-deferred accounts like 401(k)s and IRAs.

While index funds offer significant tax advantages, it is important to remember that individual tax situations can vary. Consulting a qualified tax advisor is recommended to ensure you are utilizing the most tax-efficient strategies for your investment portfolio.

Common Mistakes to Avoid When Investing

Investing in index funds is a smart strategy for long-term growth, but even seasoned investors can make mistakes. Here are some common pitfalls to avoid:

Trying to time the market: The idea that you can predict market movements is a dangerous one. Market timing is notoriously difficult, and even professionals often get it wrong. Instead of trying to time the market, focus on building a diversified portfolio and staying invested for the long haul.

Panicking during market downturns: Market corrections are a normal part of the investment cycle. It’s tempting to sell your investments during a downturn, but this can lead to significant losses. Remember that markets tend to rebound over time, so stay calm and avoid making hasty decisions.

Chasing returns: The temptation to jump on hot investment trends is strong, but chasing returns can lead to risky investments. Stick to your investment strategy and focus on diversifying your portfolio across different asset classes.

Ignoring fees: Fees can eat into your returns over time. Choose index funds with low expense ratios and avoid funds with high management fees.

Not rebalancing your portfolio: Over time, your portfolio’s asset allocation may drift from your initial plan. Rebalance your portfolio regularly to ensure it aligns with your risk tolerance and investment goals.

By avoiding these common mistakes, you can increase your chances of success in the long run.

{kind=link}