In today’s fast-paced world, financial independence is often considered a distant dream. However, it is a crucial aspect of achieving a fulfilling life and gaining control over your future. Financial independence means having enough financial resources to live comfortably without relying on others or your job. It offers the freedom to pursue your passions, make decisions without financial constraints, and enjoy a sense of security and peace of mind. This article will delve into the significance of financial independence and provide actionable steps to help you achieve this coveted goal.

Achieving financial independence is not an overnight process but a journey that requires commitment, planning, and consistent effort. It involves developing sound financial habits, understanding your financial situation, and implementing strategies for saving, investing, and managing your money wisely. The benefits of financial independence are far-reaching, extending beyond mere financial security to encompass personal growth, career satisfaction, and overall well-being. By embracing the principles of financial independence, you can empower yourself to shape a brighter future and achieve your financial aspirations.

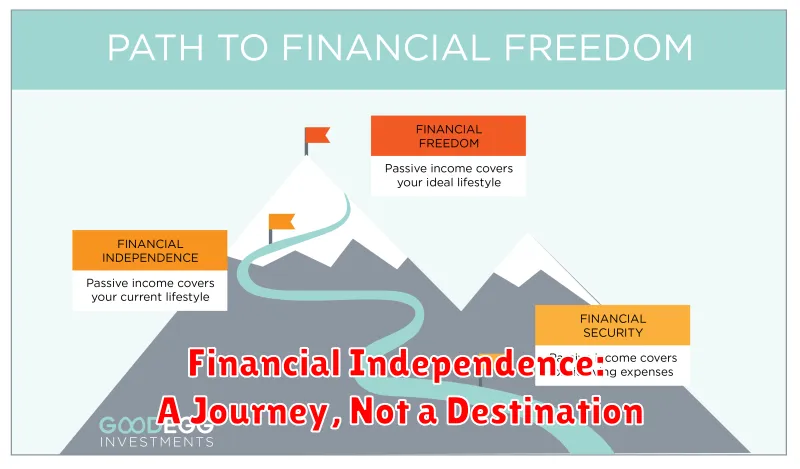

Defining Financial Independence

Financial independence is the state of having enough financial resources to live comfortably without relying on others or working for someone else. It means having enough money to cover your basic needs, such as food, shelter, and healthcare, and also having the means to pursue your passions and goals.

Many people define financial independence as reaching a point where they have enough passive income to cover their expenses. Passive income refers to income that is earned without actively working, such as rental income, dividends, or interest payments. Others may define it as having enough savings to live on for a certain period of time, such as 10 years or more.

Financial independence is not about having a huge amount of money; it’s about having enough to live a comfortable life on your own terms. It’s about having the freedom to choose how you spend your time and money without having to worry about financial constraints.

The Benefits of Being Financially Independent

Financial independence offers a myriad of benefits that extend far beyond simply having money. It provides the freedom and security to pursue your passions, achieve your goals, and live a fulfilling life.

Reduced Stress and Anxiety: When you’re financially independent, you’re not constantly worrying about bills, debt, or unexpected expenses. This reduces stress and allows you to enjoy greater peace of mind.

Increased Control over Your Life: Financial independence gives you the freedom to make choices that align with your values and priorities. You can choose your career, pursue your hobbies, and travel without being constrained by financial limitations.

Greater Job Security: If you’re not reliant on a specific job for your income, you have the flexibility to pursue opportunities that offer greater satisfaction or a better work-life balance. You’re less likely to feel trapped in a job you dislike.

Improved Health and Well-being: Financial stress can have a negative impact on both physical and mental health. Financial independence can help alleviate this stress, leading to a healthier and happier life.

Generational Impact: Financial independence allows you to build a strong foundation for future generations. You can provide support to your children and grandchildren, and ensure their financial security.

In conclusion, financial independence is not just about having money; it’s about gaining control over your life, reducing stress, and creating a more fulfilling and secure future for yourself and your loved ones.

Financial Freedom vs. Financial Independence

While often used interchangeably, financial freedom and financial independence are distinct concepts.

Financial freedom is a broader term that encompasses a feeling of not being restricted by finances. It allows you to pursue your passions, travel, or make major life choices without financial constraints. It’s about having the freedom to do what you want, when you want.

Financial independence, on the other hand, is more specific and focuses on achieving financial security. It signifies having enough passive income from investments, savings, or other sources to cover your expenses without relying on a job. This means you have the freedom to choose your work or even retire early.

In essence, financial independence is a key stepping stone to financial freedom. Achieving financial independence provides the foundation for financial freedom by removing the financial burden and allowing you to pursue your goals with greater flexibility.

Steps to Achieve Financial Independence

Financial independence is the ability to live comfortably without relying on others for financial support. It is a goal that many people strive for, and it can be achieved with planning and effort. Here are some steps to achieve financial independence:

1. Create a budget and track your spending. The first step to achieving financial independence is to understand where your money is going. Create a budget that tracks your income and expenses. This will help you identify areas where you can cut back on spending.

2. Save money regularly. Once you have a budget in place, it’s important to start saving money regularly. Set a goal for how much you want to save each month, and stick to it. You can automate your savings by setting up automatic transfers from your checking account to your savings account.

3. Invest your savings. Once you have saved a significant amount of money, it’s time to start investing. Investing your savings can help your money grow over time. There are many different investment options available, so it’s important to do your research and choose the right investments for your needs.

4. Pay down debt. Debt can be a major obstacle to financial independence. Make a plan to pay down your debt as quickly as possible. Focus on paying down high-interest debt first, such as credit card debt.

5. Increase your income. If you want to achieve financial independence sooner, you may need to increase your income. This could involve getting a raise at your current job, taking on a second job, or starting your own business.

6. Seek professional advice. If you are struggling to achieve financial independence, it may be helpful to seek professional advice from a financial advisor. A financial advisor can help you develop a plan and make smart financial decisions.

Achieving financial independence takes time and effort, but it is a worthwhile goal. By following these steps, you can put yourself on the path to financial freedom.

Creating a Budget and Tracking Expenses

One of the most crucial steps towards achieving financial independence is creating a budget and tracking your expenses. A budget acts as a roadmap for your finances, helping you allocate your money wisely and reach your financial goals. It’s essential to understand where your money is going and how to make conscious choices to control your spending.

Start by tracking your expenses for a month or two. Use a spreadsheet, budgeting app, or a simple notebook to record every penny you spend. This step will give you a clear picture of your current spending habits and identify areas where you can cut back. Once you have a good understanding of your expenses, you can create a budget that aligns with your financial goals.

A well-structured budget should include all your income sources and planned expenses. Categorize your expenses into fixed costs like rent, utilities, and loan payments, and variable costs like groceries, entertainment, and clothing. Allocate a specific amount for each category and stick to it as much as possible. Remember to factor in savings and emergency funds in your budget.

The key to effective budgeting is consistency. Regularly review your spending and make adjustments as needed. Utilize tools like budgeting apps or online platforms to simplify the process. Tracking your expenses and adhering to your budget will provide you with a sense of control over your finances, leading you closer to financial independence.

Building an Emergency Fund

An emergency fund is a crucial component of financial independence. It acts as a safety net, providing a financial cushion to handle unexpected expenses or income disruptions. Having an emergency fund ensures you can navigate unforeseen situations without derailing your financial progress.

How to Build an Emergency Fund:

- Set a Goal: Determine the desired amount for your emergency fund. Aim for three to six months’ worth of essential expenses.

- Automate Savings: Set up automatic transfers from your checking account to a dedicated savings account.

- Identify Savings Opportunities: Cut unnecessary expenses, like subscriptions or dining out, to free up funds for your emergency fund.

- Prioritize: Make saving for your emergency fund a priority. Treat it like an essential bill.

- Increase Savings Regularly: As your income grows, increase your emergency fund contributions gradually.

Building an emergency fund might seem daunting, but even small, consistent contributions can make a significant difference over time. Remember, a robust emergency fund is a cornerstone of financial independence, giving you peace of mind and the flexibility to handle life’s unexpected turns.

Managing Debt Effectively

One crucial aspect of achieving financial independence is effectively managing your debt. Debt can be a significant burden, hindering your progress towards financial freedom. To manage debt effectively, it’s vital to develop a comprehensive strategy that addresses your financial situation.

Firstly, create a budget that outlines your income and expenses. This allows you to identify areas where you can cut back to allocate more funds towards debt repayment. Consider utilizing budgeting apps or spreadsheets to track your spending and identify areas for improvement.

Next, prioritize your debts based on interest rates. Focus on paying down high-interest debts first, as they accumulate interest more rapidly. Consider using strategies like the debt snowball or avalanche method to systematically reduce your debt burden.

Furthermore, explore debt consolidation options, such as balance transfers or debt consolidation loans. These options can help you lower interest rates and simplify your repayment process. However, ensure you carefully research and compare different options before making a decision.

Lastly, avoid accumulating new debt while you’re actively paying down existing debts. It’s essential to resist the temptation of impulse purchases or unnecessary credit card spending. Maintaining a strict budget and practicing mindful spending habits will prevent you from falling back into a cycle of debt.

By effectively managing your debt, you can gain control over your finances and accelerate your journey towards financial independence. Remember that consistency and discipline are key to overcoming debt and achieving your financial goals.

Investing for the Future

Financial independence is a vital component of a secure and fulfilling future. It allows you to pursue your passions, make informed decisions, and live life on your own terms. A key aspect of achieving financial independence is investing. Investing involves allocating your money to assets with the potential to grow over time, creating wealth and ensuring your financial well-being.

Investing offers several advantages for your future:

- Growth potential: Investments can appreciate in value over time, providing you with substantial returns.

- Passive income: Certain investments, such as stocks or real estate, can generate passive income streams.

- Financial security: Investing helps build a safety net for unexpected events, ensuring you have the financial resources to navigate life’s challenges.

- Retirement planning: Investing is crucial for securing your retirement years, providing financial freedom and enabling you to enjoy your golden years.

When considering investing, remember to:

- Start early: The power of compounding works best when you start investing early.

- Diversify: Spreading your investments across different asset classes reduces risk and maximizes potential returns.

- Be patient and disciplined: Investing is a long-term game. Avoid impulsive decisions and stick to your investment plan.

- Seek professional advice: Consider consulting a financial advisor to receive personalized guidance and tailor your investment strategy to your goals and risk tolerance.

Investing is a fundamental step towards building a secure and prosperous future. By taking a proactive approach and making informed investment decisions, you can pave the way for a life of financial freedom and fulfillment.

Generating Multiple Streams of Income

Financial independence is the ultimate goal for many, and one of the most effective ways to achieve it is by generating multiple streams of income. Instead of relying on a single source of income, diversifying your income streams provides a safety net, reduces financial vulnerability, and allows for greater financial freedom.

Here are some key benefits of generating multiple streams of income:

- Increased Financial Security: Having multiple income streams mitigates the risk associated with relying solely on one source. It cushions you against unexpected financial shocks, such as job loss or business downturns.

- Financial Freedom and Flexibility: Diversified income streams allow for greater financial flexibility. You have more options to pursue your passions, travel, or invest, without feeling financially constrained.

- Accelerated Wealth Building: Multiple income streams can significantly accelerate wealth building. The additional income can be used to pay off debt faster, invest in assets, or build an emergency fund.

- Passive Income Potential: Some income streams, such as investments or online businesses, can generate passive income. This means you earn money without actively working, providing a significant boost to your financial freedom.

There are various ways to generate multiple income streams, including:

- Side Hustles: Explore freelance work, online tutoring, driving for ride-sharing services, or starting a small business.

- Investments: Diversify your investments in stocks, bonds, real estate, or other asset classes to generate passive income.

- Rental Income: Consider renting out a spare room, property, or equipment for additional income.

- Affiliate Marketing: Promote products or services online and earn commissions on sales generated through your referrals.

- Online Businesses: Create and sell digital products, such as ebooks, online courses, or templates.

The key is to identify opportunities that align with your skills, interests, and available time. Remember, generating multiple streams of income takes effort and planning. It’s a journey that requires dedication and perseverance, but the rewards of financial independence are well worth it.

Setting SMART Financial Goals

Financial independence is a state of being free from financial worries, where you have enough money to meet your needs and wants. It’s a feeling of security and peace of mind, knowing that you can achieve your financial goals without relying on anyone else.

Setting SMART financial goals is crucial for achieving financial independence. SMART stands for Specific, Measurable, Attainable, Relevant, and Time-Bound.

By defining your goals in this way, you create a clear roadmap for your financial journey.

Specific

Instead of simply saying, “I want to save more money,” be specific about the amount you want to save and what you will save for. For example, “I want to save $10,000 in the next two years to put down a deposit on a new house.”

Measurable

Your financial goals should be measurable so you can track your progress. For example, you could set a goal to increase your savings rate by 5% each year.

Attainable

Make sure your goals are achievable based on your current financial situation. Set realistic targets that you can realistically achieve within a given timeframe.

Relevant

Ensure your financial goals are aligned with your overall financial objectives and life aspirations. If your goal is to retire early, then investing for retirement is relevant, but if your goal is to travel the world, then saving for travel is more relevant.

Time-Bound

Set deadlines for your financial goals. Having a timeframe helps you stay motivated and hold yourself accountable.

The Role of Discipline and Patience

Financial independence is a journey that requires unwavering discipline and an abundance of patience. It’s not a get-rich-quick scheme but rather a long-term commitment to building a secure future.

Discipline is the cornerstone of financial success. It involves making conscious and deliberate choices about your spending, saving, and investing. This means resisting impulsive purchases, sticking to a budget, and consistently putting money aside for your goals. It also means making sacrifices and prioritizing long-term financial well-being over short-term gratification.

Patience is equally crucial. Building wealth takes time and effort. It requires the ability to weather market fluctuations, resist the temptation to withdraw funds prematurely, and trust in the power of compounding over time. Financial independence is not a sprint, but a marathon, and it’s essential to be patient and persistent throughout the journey.

The good news is that discipline and patience are skills that can be developed. By setting clear financial goals, establishing routines, and actively managing your finances, you can cultivate these habits and pave the way for a financially secure future.

Overcoming Obstacles on the Path to Financial Independence

The journey to financial independence is not always smooth sailing. Along the way, you’ll encounter various obstacles that can test your resolve. However, by acknowledging these hurdles and developing effective strategies to overcome them, you can stay on track and achieve your financial goals.

One common obstacle is lack of knowledge. Many people simply don’t have the financial literacy needed to make informed decisions about their money. It’s crucial to educate yourself about budgeting, investing, debt management, and other essential financial concepts.

Another obstacle is fear. Fear of the unknown, fear of making mistakes, and fear of losing money can paralyze you and prevent you from taking action. To overcome this, it’s important to set realistic goals, break down large tasks into smaller steps, and celebrate your progress along the way.

Procrastination is another common roadblock. It’s easy to put off saving and investing for later, but time is of the essence when it comes to building wealth. To combat procrastination, establish a routine, automate your savings, and hold yourself accountable.

Life’s unexpected events can also throw a wrench in your plans. Job loss, medical emergencies, and family issues can derail your progress. Building an emergency fund and having a contingency plan in place can help you weather these storms.

Finally, remember that financial independence is a marathon, not a sprint. You’re not going to become financially independent overnight. Be patient, persistent, and don’t give up on your goals.

Maintaining Financial Independence Long-Term

Financial independence isn’t just about achieving a certain level of wealth; it’s about establishing a sustainable lifestyle that allows you to live comfortably without relying on external financial support. This means going beyond simply accumulating assets and focusing on long-term financial strategies that ensure your financial security well into the future.

A key aspect of maintaining financial independence is consistent income generation. This might involve diversifying your income streams through investments, side hustles, or even starting a business. However, it’s equally important to manage your expenses wisely. Creating a realistic budget and sticking to it, even as your income grows, is crucial. This ensures that you’re living within your means and avoiding unnecessary debt.

Furthermore, building an emergency fund acts as a safety net for unexpected expenses, preventing you from dipping into your savings. The ideal emergency fund should cover 3-6 months of living expenses. Additionally, it’s essential to protect your assets through insurance. Health insurance, property insurance, and other relevant insurance policies offer financial protection against unforeseen events, safeguarding your financial stability.

Finally, remember that financial independence is an ongoing journey, not a destination. The world is constantly changing, and so are the financial landscape and your needs. Regularly reviewing and adjusting your financial plan ensures that it remains relevant and effective in meeting your long-term goals. By staying proactive and adapting your strategies as necessary, you can maintain your financial independence for years to come.

Financial Independence: A Journey, Not a Destination

Financial independence is often portrayed as a finish line – a point where you’ve accumulated enough wealth to live comfortably without working. While this is a desirable outcome, it’s important to understand that financial independence is not a destination, but a journey. It’s a continuous process of building healthy financial habits, making informed decisions, and actively managing your money to achieve a sense of freedom and security.

The journey to financial independence is not about accumulating vast sums of money; it’s about gaining control over your finances and aligning your spending with your values. It’s about creating a life where money doesn’t dictate your choices, but rather empowers you to pursue your passions and live life on your own terms.

Embracing this journey involves a shift in mindset: from chasing the next big purchase to prioritizing long-term financial stability. It’s about developing financial literacy, setting realistic goals, and actively working towards them. It’s about making smart financial decisions today, so you can enjoy greater freedom and peace of mind tomorrow.

Celebrating Your Financial Successes

Achieving financial independence is a significant milestone, and it’s essential to recognize and celebrate your progress along the way. Every step you take, no matter how small, deserves acknowledgment. Celebrating your wins, big or small, boosts your motivation, reinforces positive habits, and fuels your journey toward financial freedom.

Financial milestones can be anything from paying off a debt to saving a certain amount of money. Celebrate every success, no matter how big or small. A simple dinner out with your loved ones, a small reward for yourself, or even just taking the time to reflect on your accomplishment can make a difference. These small acts of celebration reinforce the positive feelings associated with financial progress, making you more likely to continue on your path.

Celebrating your successes also serves as a reminder of the progress you’ve made, helping to keep you motivated when you encounter challenges. Financial independence is a marathon, not a sprint. There will be setbacks and obstacles along the way. By celebrating your victories, you create a positive and encouraging environment for yourself, making it easier to stay focused on your goals and overcome any hurdles that come your way.

Remember, financial independence is about more than just money. It’s about achieving peace of mind, freedom, and control over your life. Celebrate your successes to acknowledge your hard work and dedication, and to fuel your journey towards a brighter financial future.

{kind=link}