Are you approaching retirement age and wondering if you should hang up your hat or keep working a few more years? The decision to retire is a personal one, but it’s important to consider all factors, including the financial benefits of delaying retirement. While you may be eager to enjoy your golden years, delaying retirement can significantly impact your long-term financial security, offering a wealth of benefits that can enhance your lifestyle and ensure a more comfortable future.

While the idea of relaxing and pursuing hobbies is enticing, delaying retirement allows you to continue building your nest egg, maximizing your savings and investments. This extended time in the workforce gives you the opportunity to accumulate more wealth, ensuring a more comfortable retirement filled with financial freedom and peace of mind. Additionally, delaying retirement can help you avoid depleting your retirement savings prematurely, allowing your nest egg to grow and potentially generate larger returns over time. Let’s explore the specific financial benefits that can come with delaying retirement.

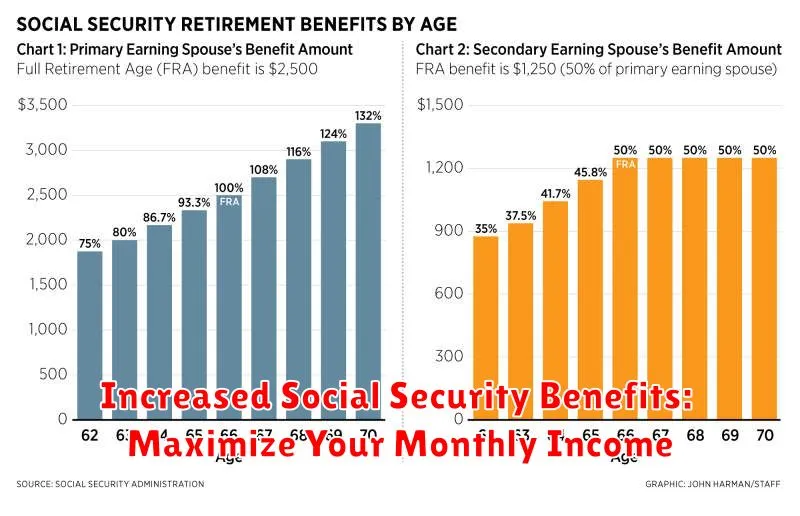

Increased Social Security Benefits: Maximize Your Monthly Income

One of the most compelling financial benefits of delaying retirement is the potential for increased Social Security benefits. The Social Security Administration (SSA) offers a delayed retirement credit for those who wait to claim benefits beyond their full retirement age (FRA). This credit can significantly boost your monthly income, providing you with a more comfortable and secure financial future.

The SSA calculates your benefits based on your earnings history and your age at retirement. If you claim benefits before your FRA, your payments will be permanently reduced. However, if you delay your retirement, your benefits will increase by 8% per year for every year you wait beyond your FRA. This means that waiting just two years beyond your FRA can increase your monthly benefits by 16%.

For example, if your FRA is 67 and you claim benefits at 70, your monthly payments will be 24% higher than they would have been at 67. This extra income can make a substantial difference in your retirement lifestyle, allowing you to pursue your passions, travel, or simply enjoy a more comfortable standard of living.

In addition to the increased monthly payments, delaying retirement also gives you the opportunity to earn more money before you stop working. This can further bolster your retirement savings and provide you with even more financial security.

It’s important to note that the decision to delay retirement is a personal one, and it’s essential to consider your individual circumstances and financial goals. However, if you are financially able to wait, delaying retirement can be a smart move to maximize your Social Security benefits and secure a more comfortable financial future.

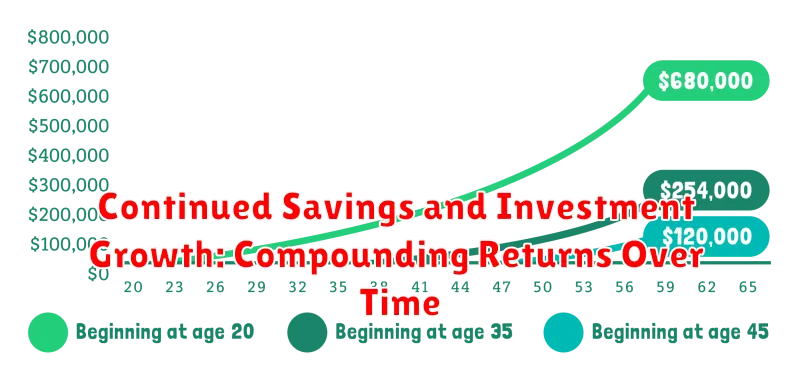

Continued Savings and Investment Growth: Compounding Returns Over Time

One of the most significant advantages of delaying retirement is the potential for continued savings and investment growth. The power of compounding allows your money to grow exponentially over time. The longer you work and contribute to your savings, the more time your investments have to compound and generate returns.

Imagine you invest $10,000 annually with a 7% annual return. If you retire at 65, you’ll have about 20 years for your investments to grow. However, delaying retirement by just 5 years to age 70 extends the compounding period by 5 years, potentially resulting in a significantly larger nest egg.

The impact of compounding is especially pronounced over the long term. It’s like a snowball rolling down a hill, gathering more snow as it goes. By delaying retirement, you give your snowball more time to gather size and momentum, leading to substantial financial benefits.

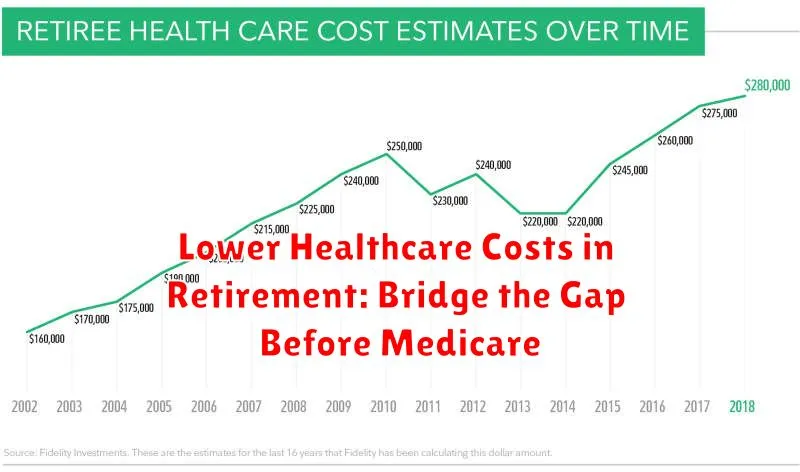

Lower Healthcare Costs in Retirement: Bridge the Gap Before Medicare

One of the biggest financial concerns for retirees is the cost of healthcare. Medicare, the government-funded health insurance program for people over 65, doesn’t cover everything. There are copays, deductibles, and out-of-pocket expenses that can quickly add up.

By delaying retirement, you can give yourself more time to save for these healthcare expenses. This is especially important if you’re planning to retire before you’re eligible for Medicare at age 65. You can use this extra time to build up a health savings account (HSA) or other savings account specifically for healthcare costs.

Here are some strategies to consider:

1. Contribute to a Health Savings Account (HSA): HSAs are tax-advantaged accounts that can be used for healthcare expenses. You can contribute to an HSA even if you’re not currently enrolled in a high-deductible health plan, and the money grows tax-free.

2. Purchase a Long-Term Care Insurance Policy: These policies can help cover the costs of long-term care services, such as assisted living or nursing home care, which can be very expensive.

3. Save Aggressively: Aim to save as much as possible in the years leading up to retirement. This will give you a larger nest egg to draw from when you need it.

By taking these steps, you can help ensure that you have the financial resources to cover your healthcare needs in retirement.

Greater Financial Security: A Larger Nest Egg for Peace of Mind

One of the most significant advantages of delaying retirement is the opportunity to build a larger nest egg. By working longer, you can continue to save and invest, allowing your money to grow exponentially through compounding returns. This increased financial security provides a sense of peace of mind, knowing you have a solid foundation for your future years.

Delaying retirement gives you more time to contribute to your retirement accounts, such as 401(k)s and IRAs. This can translate to a significantly larger balance at retirement, offering greater financial flexibility and independence.

Moreover, delaying retirement allows you to take advantage of the “power of compounding,” a key principle in investing. The longer your money grows in the market, the more it can compound, leading to substantial wealth accumulation over time.

A larger nest egg also provides a buffer against unexpected expenses, such as medical bills or home repairs, in retirement. Having this financial cushion can alleviate stress and worry, allowing you to enjoy your retirement years to the fullest.

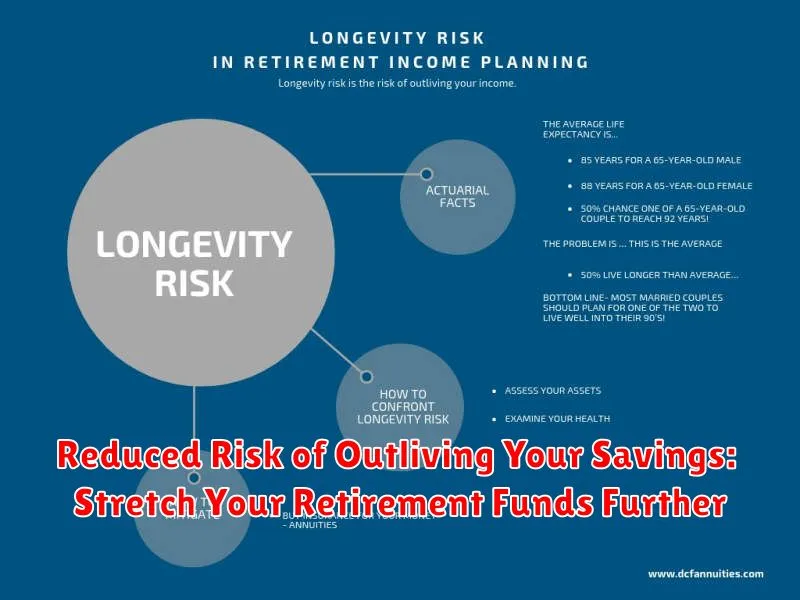

Reduced Risk of Outliving Your Savings: Stretch Your Retirement Funds Further

One of the biggest anxieties associated with retirement is the fear of running out of money before the end of your life. Delaying retirement can significantly reduce this risk, allowing you to stretch your retirement funds further and enjoy a more secure financial future.

By working longer, you continue to accrue savings and investments, giving your portfolio more time to grow. This extended growth period can translate into a larger nest egg, providing you with a more substantial income stream during retirement.

Furthermore, delaying retirement reduces the number of years you’ll need to draw from your savings. This reduces the pressure on your retirement funds and lessens the chances of running out of money during your golden years.

The benefits of delaying retirement go beyond just financial security. You may also experience a greater sense of personal fulfillment, continue to enjoy cognitive stimulation through work, and contribute to society for a longer period.

Opportunities for Part-Time Work: Stay Active and Supplement Your Income

Delaying retirement allows you to explore part-time work opportunities, offering a flexible and fulfilling way to stay active and supplement your income. Engaging in part-time work can provide several financial benefits, including:

- Increased Savings: Part-time earnings can be used to bolster your retirement nest egg, allowing you to save more and retire comfortably.

- Reduced Dependence on Retirement Funds: By working part-time, you can minimize your reliance on retirement savings, ensuring they last longer.

- Financial Flexibility: Part-time work gives you the flexibility to manage your expenses and adjust to any unexpected financial situations.

- Reduced Retirement Age: Working part-time can help you postpone retirement for longer, potentially allowing you to retire earlier than initially planned.

Beyond the financial benefits, part-time work offers the opportunity to:

- Stay Engaged: Part-time work allows you to stay mentally and socially engaged, combating boredom and isolation.

- Learn New Skills: New work experiences can provide you with valuable skills and knowledge, keeping your mind sharp and adaptable.

- Maintain Social Connections: Part-time work can be a great way to maintain social connections and build new relationships.

If you are considering delaying retirement, explore the potential of part-time work. It can be a rewarding and financially beneficial way to enjoy your later years.

More Time for Personal Pursuits: Enjoy Your Golden Years to the Fullest

Delaying retirement can provide the financial freedom to fully immerse yourself in your personal pursuits. Imagine waking up each morning without the pressure of a 9-to-5 job, knowing you have the time and resources to explore your passions. Whether it’s traveling the world, pursuing hobbies, or simply enjoying quality time with loved ones, delaying retirement allows you to savor these golden years to the fullest.

With a larger nest egg, you can afford to indulge in experiences that may have been financially out of reach before. Take that dream trip to Europe, finally learn to play the guitar, or volunteer your time to a cause you’re passionate about. The possibilities are endless when you have the financial security to pursue your personal goals.

Stronger Legacy Planning: Leave a Lasting Impact on Your Loved Ones

Delaying retirement can significantly strengthen your legacy planning efforts, allowing you to leave a more substantial and lasting impact on your loved ones. By working longer, you have more time to accumulate wealth, which can be used to secure their financial future. This could mean providing for their education, helping them achieve their dreams, or simply ensuring their financial stability.

The additional years of income also allow you to build a more robust estate. This could involve investing in assets like property or stocks, which appreciate over time. You can also contribute more to retirement accounts, providing your beneficiaries with a greater inheritance.

Moreover, delaying retirement allows you to actively manage your finances and investments, ensuring that your wealth is properly allocated and protected. This proactive approach safeguards your legacy and minimizes the risk of financial hardship for your loved ones after your passing.

The decision to delay retirement is a personal one. However, it’s important to understand the potential benefits it offers for your legacy planning. By extending your working life, you can leave a more secure and prosperous future for your loved ones, ensuring they can thrive and continue to build their own legacy.

Mental and Physical Health Benefits: Staying Engaged and Active

Working longer can have significant positive impacts on your mental and physical health. Staying engaged and active in the workforce can provide a sense of purpose and accomplishment, which can boost your mood and overall well-being. Continuing to use your skills and knowledge can keep your mind sharp and prevent cognitive decline. Moreover, staying active in a work environment can encourage physical activity, leading to improved physical health and fitness.

Research has shown a strong correlation between staying active in work and reduced risk of depression and dementia. Many individuals find satisfaction and fulfillment in their work, and retiring early can lead to feelings of isolation and loneliness. By remaining engaged in the workforce, you can maintain social connections and keep your mind active, contributing to a healthier and happier life.

The benefits of staying active go beyond mental well-being. Studies have shown that individuals who work longer tend to have better physical health. This is due to several factors, including the need to stay physically active in the workplace, the continuation of health insurance coverage, and the potential for access to company fitness programs. Delaying retirement can also help you maintain a healthy weight, reduce the risk of chronic diseases, and improve your overall health and longevity.

Reduced Reliance on Savings: Delay Withdrawals for Long-Term Growth

One of the most compelling financial benefits of delaying retirement is the potential to reduce your reliance on savings. By continuing to work even a few extra years, you can significantly increase your retirement nest egg. This allows you to withdraw less from your savings during retirement, ensuring that your money lasts longer.

Furthermore, delaying retirement gives your investments more time to grow. Compound interest works wonders over the long term, and the extra years you spend working and saving can make a significant difference in your overall wealth. This can provide you with greater financial security and peace of mind in your later years.

Delaying retirement can also help you avoid the risk of running out of money. It allows you to take a more conservative approach to withdrawing from your savings, ensuring that you have enough to cover your expenses for the rest of your life.

{kind=link}