Feeling overwhelmed by debt? You’re not alone. Many people struggle with multiple debts, from credit cards to student loans. The good news is that there are strategies to help you get out of debt and take control of your finances. One popular method is the debt snowball, a simple yet effective approach that can help you pay off your debts faster and gain momentum along the way.

In this article, we’ll delve into the debt snowball method, explaining how it works, its advantages, and how to implement it. We’ll also explore other debt repayment strategies to help you find the best approach for your specific situation. Whether you’re just starting your debt journey or looking for ways to accelerate your progress, this guide will provide valuable insights and practical steps to help you achieve financial freedom.

Understanding the Debt Snowball Method

The debt snowball method is a popular strategy for paying off multiple debts. It involves listing your debts from smallest to largest balance, then making minimum payments on all of them except for the smallest one. You then put as much extra money as possible towards the smallest debt, paying it off as quickly as possible. Once the smallest debt is paid off, you take that monthly payment amount and add it to the payment on the next smallest debt, and so on. This creates a “snowball” effect, where the amount of money you’re paying towards your debts gets bigger and bigger with each payoff.

The debt snowball method is based on the idea of psychological motivation. Seeing yourself quickly pay off smaller debts can be very rewarding and encouraging. This can help you stay motivated to keep making payments and eventually pay off all your debts.

Listing Your Debts From Smallest to Largest

The first step in using the debt snowball method is to list all of your debts, from smallest to largest balance. This can seem daunting, but it’s essential to get a clear picture of your financial situation.

To create your debt list, start by gathering all of your credit card statements, loan agreements, and any other documentation that outlines your outstanding debts. Then, make a table with columns for the following information:

- Creditor: This is the name of the company or individual you owe money to (e.g., Chase Bank, Student Loan Provider).

- Debt Type: This indicates the type of debt (e.g., credit card, student loan, personal loan).

- Balance: This is the current amount you owe.

- Interest Rate: This is the annual percentage rate (APR) of the debt.

- Minimum Payment: This is the minimum amount you are required to pay each month.

Once you’ve gathered all of your debt information, order it from smallest balance to largest balance. This will form the foundation for your debt snowball strategy.

Making Minimum Payments on All Debts

Before you start using the debt snowball method, you might be tempted to just make the minimum payment on all of your debts and hope that you can eventually pay them all off. However, this is often not the best strategy.

Making only the minimum payments will likely mean that you’re stuck in a cycle of debt for a long time. This is because minimum payments are often very low, especially for credit cards. Most of your payment will go toward interest charges, and only a small amount will go toward the principal balance. This means you’ll be paying more interest over time, and it could take you much longer to pay off your debt.

The debt snowball method is a better strategy because it helps you to focus on getting out of debt as quickly as possible. It’s important to make at least the minimum payment on all of your debts, but by paying more than the minimum on one debt each month, you’ll be able to reduce your balance faster.

Focusing Extra Payments on the Smallest Debt

The debt snowball method encourages you to focus extra payments on the smallest debt first. This can be a powerful motivator, as it provides a sense of accomplishment as you quickly pay off smaller debts. This can help you gain momentum and stay committed to your debt repayment plan.

By tackling the smallest debt first, you can quickly achieve a sense of progress. This can be a powerful motivator, as it gives you a sense of control over your finances and reinforces your commitment to becoming debt-free.

When you pay off a debt, it frees up more cash flow. This allows you to allocate even more extra payments toward the next smallest debt, further accelerating your debt repayment journey. It’s like a snowball rolling downhill, gathering momentum as it goes.

Repeating the Process Until All Debts Are Paid Off

Once you’ve made your minimum payments on all of your debts, you’ll start focusing on the smallest debt first. This is where the snowball method gets its name. You’ll make the minimum payment on all of your debts except the smallest one, and you’ll throw every extra dollar you have at the smallest debt. As you pay down the smallest debt, you’ll start to see a significant reduction in your total debt, which will motivate you to keep going. This will also give you a sense of accomplishment, and the momentum will help you keep going even when things get tough.

Once the smallest debt is paid off, you’ll take the minimum payment that you were making on that debt, and add it to the minimum payment on the next smallest debt. You’ll now be making a larger payment on that next smallest debt, and you’ll continue to pay the minimum on all other debts. You’ll continue to repeat this process until you have paid off all of your debts.

Advantages of the Debt Snowball Method

The debt snowball method is a popular way to pay off debt. It involves listing your debts from smallest to largest balance, then making minimum payments on all of your debts except the smallest one. You then throw all of your extra money at that smallest debt until it’s paid off. Once that debt is gone, you roll the payment amount from that debt onto the next smallest debt, and so on. This process continues until you pay off all of your debts.

One of the biggest advantages of the debt snowball method is that it can be very motivating. Seeing your debts disappear one by one can give you a sense of accomplishment and keep you motivated to keep going. This is especially helpful for people who are feeling overwhelmed by their debt.

Another advantage of the debt snowball method is that it can help you build momentum. By focusing on paying off the smallest debts first, you can quickly start to see progress. This can make you feel more in control of your finances and give you the motivation to keep working towards your debt-free goals.

While the debt snowball method can be a very effective way to pay off debt, it’s important to keep in mind that it may not be the most financially efficient way to do it. The debt avalanche method, which involves paying off debts from highest interest rate to lowest, will save you more money in the long run. However, for some people, the motivational aspects of the debt snowball method outweigh the potential savings from the avalanche method.

Disadvantages of the Debt Snowball Method

The debt snowball method, while effective for some, has its share of drawbacks. Here are some things to consider:

Higher Interest Costs: The debt snowball method prioritizes paying off the smallest debts first, regardless of interest rates. This can lead to paying more interest overall, as you’ll be paying down lower-interest debts before those with higher interest rates.

Longer Payoff Time: Focusing on paying off smaller debts first can mean it takes longer to eliminate the debts with the highest interest rates. This can result in a longer overall repayment period.

Possible Discouragement: The snowball method can be discouraging if you’re making significant payments but still see a large balance on your highest-interest debt. This can make you feel like you’re not making progress.

Limited Financial Planning: The debt snowball method doesn’t take into account your overall financial goals, such as building an emergency fund or saving for retirement. This can lead to neglecting other important financial priorities.

Debt Snowball vs. Debt Avalanche: Which Is Right for You?

When you have multiple debts, it can feel overwhelming to know where to start paying them off. Two popular strategies for tackling debt are the debt snowball and the debt avalanche. Both methods are effective, but they approach debt repayment differently.

The debt snowball method focuses on paying off your smallest debt first, regardless of interest rate. This strategy gives you a quick win, which can provide motivation and momentum to keep going. Once the smallest debt is paid off, you roll that payment amount onto the next smallest debt, creating a snowball effect that gets bigger with each successful payoff.

The debt avalanche method, on the other hand, prioritizes paying off debts with the highest interest rates first. This approach is more mathematically efficient, as you save more money in the long run by minimizing interest charges. However, it can be demotivating to see your debt balance decrease slowly at first.

Ultimately, the best strategy for you depends on your personal preferences and financial situation. If you value quick wins and staying motivated, the debt snowball method may be a better fit. If you prioritize saving money on interest and minimizing your overall debt cost, the debt avalanche method could be more appealing.

Here’s a table summarizing the key differences between the two methods:

| Method | Focus | Pros | Cons |

|---|---|---|---|

| Debt Snowball | Smallest debt first | Motivating, quick wins | May pay more interest overall |

| Debt Avalanche | Highest interest rate first | Saves money on interest, minimizes debt cost | Can be demotivating, slower progress initially |

No matter which method you choose, it’s important to be consistent with your payments and stay focused on your goal of becoming debt-free. Both the debt snowball and debt avalanche strategies can help you achieve financial freedom!

Tips for Success with the Debt Snowball Method

The debt snowball method is a popular way to pay off multiple debts. It involves focusing on paying off your smallest debt first, while making minimum payments on your other debts. Once you’ve paid off the smallest debt, you roll that payment amount into the next smallest debt, and so on. This method can be very motivating, as you quickly start to see progress and feel like you’re making real headway.

Here are some tips for success with the debt snowball method:

- Create a Budget: Before you can start the debt snowball method, you need to know how much money you have coming in and going out each month. This will help you determine how much you can afford to put towards your debt each month.

- List Your Debts: List all of your debts from smallest to largest balance. This will give you a clear picture of your debt situation and help you prioritize which debts to tackle first.

- Make Minimum Payments on Other Debts: While you are focused on paying down your smallest debt, make sure to make at least the minimum payment on your other debts to avoid late fees and penalties.

- Stay Committed: The key to success with the debt snowball method is to stay committed to your plan. There may be times when you want to give up, but it’s important to remember why you started in the first place.

- Reward Yourself: As you pay off each debt, reward yourself with something small. This will help you stay motivated and on track.

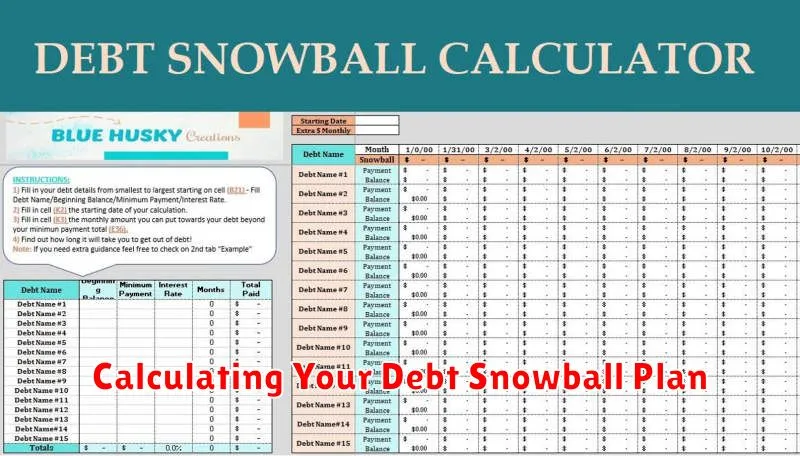

Calculating Your Debt Snowball Plan

The debt snowball method involves listing your debts from smallest to largest balance, then paying the minimum payment on all debts except for the smallest. You then throw all your extra money at the smallest debt until it’s paid off. Once that debt is gone, you roll the amount you were paying on it onto the next smallest debt, and so on.

To start calculating your debt snowball plan, you’ll need to gather a few pieces of information:

- A list of all your debts

- The balance of each debt

- The interest rate of each debt

- Your monthly income

- Your monthly expenses

Once you have this information, you can create a spreadsheet or use a debt snowball calculator to help you visualize your plan. Here’s a basic example:

| Debt | Balance | Interest Rate | Minimum Payment |

|---|---|---|---|

| Credit Card A | $1,000 | 18% | $30 |

| Credit Card B | $5,000 | 15% | $150 |

| Student Loan | $20,000 | 6% | $200 |

In this example, you would first focus on paying off Credit Card A. You would make the minimum payment on the other debts, and then throw any extra money you have at Credit Card A. Once Credit Card A is paid off, you would roll the $30 you were paying on it onto Credit Card B, and so on.

It’s important to note that the debt snowball method doesn’t always result in the fastest debt payoff. Since you’re not paying down the debts with the highest interest rates first, you could end up paying more in interest over time. However, the snowball method can be a great motivator, as it allows you to see progress quickly and feel a sense of accomplishment as you pay off each debt.

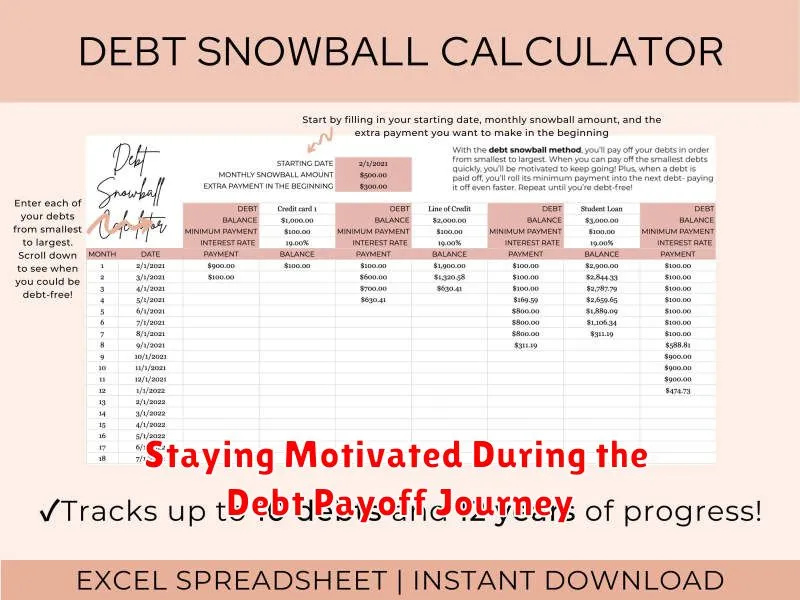

Staying Motivated During the Debt Payoff Journey

Paying off debt can be a long and arduous process, and it’s easy to lose motivation along the way. But staying motivated is crucial to success. Here are a few tips to help you stay on track:

1. Set Realistic Goals: Don’t try to tackle too much at once. Break down your debt payoff plan into smaller, achievable goals. For example, instead of aiming to pay off $10,000 in a year, focus on paying off $500 per month. This will make your progress feel more manageable and keep you motivated.

2. Celebrate Your Wins: Every time you reach a milestone, celebrate your success! This could be anything from paying off a small loan to making a large payment on a credit card. Rewarding yourself for your hard work will help you stay focused and motivated.

3. Visualize Your Future: Imagine the freedom and peace of mind you will have once your debt is paid off. This can be a powerful motivator, reminding you of why you’re working so hard.

4. Find a Support System: Surround yourself with people who will encourage and support you on your debt payoff journey. Talk to friends, family, or a financial advisor about your goals and challenges. Having a support system can make a big difference in your motivation.

5. Stay Positive: There will be times when you feel overwhelmed or discouraged. It’s important to remember that you’re not alone and that you can do this! Focus on your progress and stay positive. You are getting closer to your financial freedom every day.

{kind=link}