Are you a freelancer or self-employed worker looking to take control of your finances? Navigating the world of income and expenses can be a challenge, especially when you’re responsible for everything from taxes to retirement planning. But don’t worry, we’ve got you covered! This article is packed with essential financial tips designed to help you achieve financial stability and reach your financial goals.

From mastering budgeting and saving strategies to understanding taxes and retirement planning, we’ll break down the key concepts that every freelancer and self-employed worker needs to know. Whether you’re just starting out or looking to take your financial management to the next level, this guide will provide the insights and tools you need to thrive.

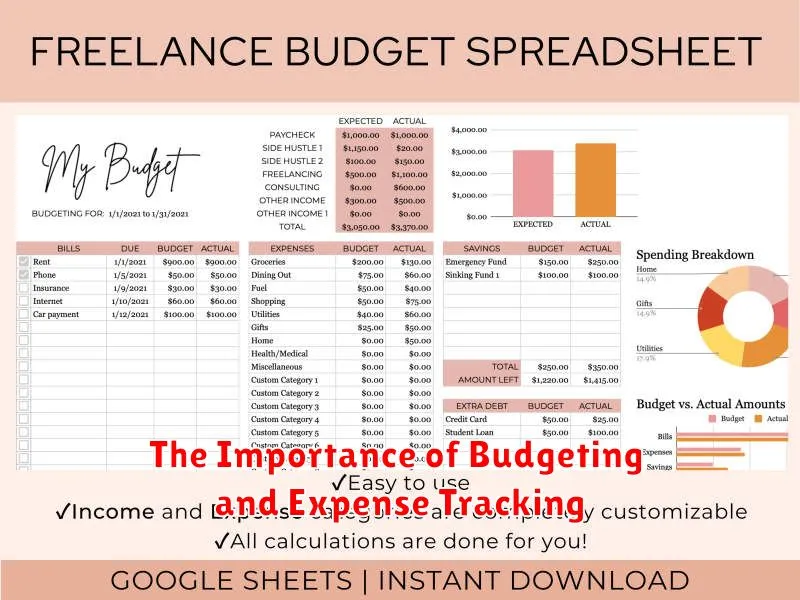

The Importance of Budgeting and Expense Tracking

As a freelancer or self-employed individual, you are responsible for managing your own finances. This means that you need to be on top of your income and expenses to ensure that you are profitable and able to save for the future. One of the most important aspects of financial management is budgeting and expense tracking.

Budgeting is the process of creating a plan for how you will spend your money. This plan should include your income and expenses, and it should be updated regularly. A budget helps you to track your spending, identify areas where you can save money, and make sure that you are not overspending.

Expense tracking is the process of recording all of your expenses. This can be done manually using a spreadsheet or notebook, or you can use a budgeting app. Tracking your expenses helps you to see where your money is going and to identify areas where you can cut back. It can also help you to prepare for tax season by providing a detailed record of your business expenses.

By budgeting and tracking your expenses, you can gain a better understanding of your financial situation and make informed decisions about your spending. This can help you to avoid financial stress, build a solid financial foundation, and achieve your financial goals.

Managing Irregular Income and Cash Flow

One of the biggest challenges freelancers and self-employed workers face is managing irregular income and cash flow. Unlike traditional employees with a steady paycheck, your earnings can fluctuate greatly from month to month. This can make it difficult to budget, save, and plan for the future.

To manage this irregularity, it’s important to implement strategies that ensure you have enough cash on hand to cover your expenses. Here are some tips for managing irregular income and cash flow:

- Track your income and expenses meticulously: Use a budgeting app or spreadsheet to track every dollar that comes in and goes out. This will give you a clear picture of your financial situation and help you identify areas where you can cut back.

- Create a budget and stick to it: Based on your income and expenses, create a realistic budget that allocates funds for essential expenses, savings, and debt repayment. Make sure to factor in any seasonal fluctuations in your income.

- Set up a savings cushion: Aim to have at least 3-6 months’ worth of living expenses saved in an emergency fund. This will provide a safety net during slow months or unexpected expenses.

- Consider setting up a separate business account: Separating your business and personal finances will make it easier to track income and expenses and to file your taxes.

- Invoice promptly and follow up on payments: Send invoices immediately after completing work and follow up regularly to ensure timely payment.

- Explore alternative income streams: Having multiple income sources can help to even out fluctuations in your primary income. Consider offering additional services or products or taking on freelance gigs.

Managing irregular income can be challenging, but by implementing these strategies, you can gain control of your finances and build a strong financial foundation for your freelance or self-employed career.

Setting Up a System for Invoicing and Payment Collection

As a freelancer or self-employed worker, getting paid on time is crucial. A reliable system for invoicing and payment collection helps you manage your finances efficiently and maintain a healthy cash flow.

Choose an invoicing software that suits your needs. There are many options available, both free and paid. Some popular choices include FreshBooks, Xero, and Invoice Ninja. These platforms allow you to create professional-looking invoices, track payments, and send reminders.

Be clear and concise in your invoices. Include all essential information such as your name, business details, client information, invoice number, date, description of services, and payment terms. It’s also beneficial to specify a payment deadline.

Send invoices promptly after completing work. Timely invoicing ensures your clients are aware of their obligations and avoids delays in payment. Consider using a payment gateway to make it easier for clients to pay online. Options like PayPal, Stripe, and Square offer secure and convenient payment processing.

Establish clear payment terms with your clients. Determine the payment schedule, whether it’s upfront, milestones, or upon completion of the project. Communicate these terms clearly in your contracts and invoices to avoid misunderstandings.

Follow up with clients who haven’t paid on time. Send polite reminders and inquire about any issues they may be facing. Being proactive in payment collection helps maintain a healthy relationship with your clients and minimizes late payments.

Implementing a system for invoicing and payment collection empowers you to manage your finances effectively, track income, and receive timely payments. This is essential for financial stability and sustainable growth in your freelance or self-employed career.

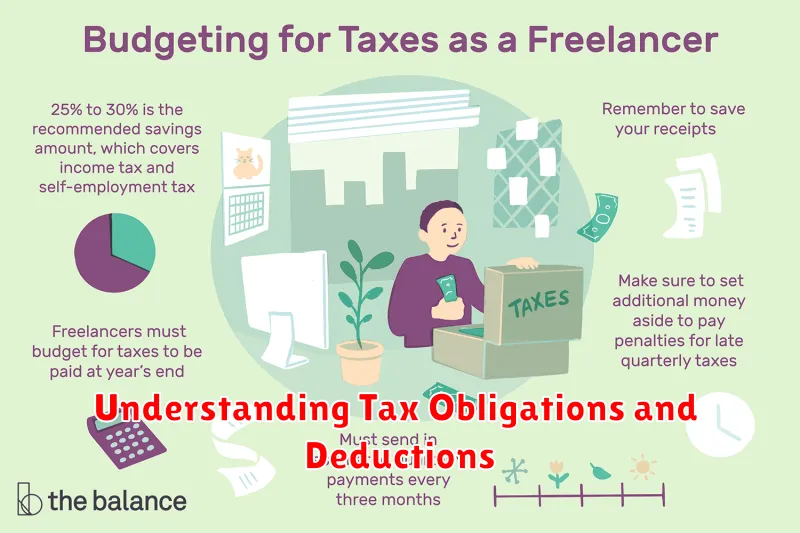

Understanding Tax Obligations and Deductions

As a freelancer or self-employed worker, you’re responsible for handling your own taxes. This means understanding your tax obligations and taking advantage of available deductions to minimize your tax burden.

Your tax obligations will depend on your specific circumstances, including your income, expenses, and location. You’ll generally need to pay self-employment taxes, including Social Security and Medicare, in addition to income tax. You may also be required to pay state and local taxes.

Deductions can significantly reduce your taxable income. Common deductions for freelancers and self-employed individuals include:

- Home office expenses

- Business expenses (e.g., supplies, travel, professional services)

- Health insurance premiums

- Retirement contributions

It’s important to keep accurate records of your income and expenses throughout the year to ensure you can claim all eligible deductions. This can be done with a simple spreadsheet or dedicated accounting software.

Consult with a tax professional to ensure you’re taking advantage of all available deductions and meeting your tax obligations. They can help you navigate the complexities of self-employment taxes and develop a personalized tax plan.

Creating a Safety Net: Emergency Funds and Savings

As a freelancer or self-employed worker, you’re responsible for your own income, which means there’s no safety net of a regular paycheck or benefits. It’s critical to create your own financial cushion by building an emergency fund and establishing consistent saving habits.

An emergency fund acts as a financial buffer to handle unexpected events, like illness, equipment failure, or a sudden drop in work. Aim for a fund that covers 3-6 months of living expenses. This can be a challenging goal for freelancers, so start small and gradually build up your savings.

Here are some tips for building your emergency fund:

- Set a savings goal and track your progress.

- Automate your savings by setting up regular transfers from your checking account.

- Find ways to cut back on expenses.

- Consider using a high-yield savings account to maximize your returns.

Building an emergency fund is essential for financial security and peace of mind. It gives you the freedom to handle unexpected situations without jeopardizing your finances.

Investing for Retirement as a Freelancer

Retirement planning for freelancers and self-employed workers can be a bit more challenging than for those with traditional jobs. Since you don’t have an employer contributing to a 401(k) or providing a pension plan, you’re solely responsible for your retirement savings. Fortunately, there are a number of options available to freelancers for building a nest egg.

One of the most popular choices is a Solo 401(k). This is a retirement savings plan designed for self-employed individuals and small business owners. With a Solo 401(k), you can contribute as both an employee and employer, allowing you to maximize your contributions. The money grows tax-deferred, and you don’t pay taxes until you withdraw it in retirement.

Another option is a SEP IRA. This is a simpler and less expensive retirement plan that’s easier to set up than a Solo 401(k). However, SEP IRAs have lower contribution limits than Solo 401(k)s.

No matter which retirement plan you choose, make sure to invest wisely. Consider a diversified portfolio that includes a mix of stocks, bonds, and other assets. You should also take into account your risk tolerance and time horizon.

Investing for retirement as a freelancer may require more effort and planning than for someone with a traditional job. However, by taking advantage of the available resources and making smart decisions, you can build a secure financial future for yourself.

Finding Affordable Health Insurance Options

As a freelancer or self-employed individual, securing affordable health insurance can be a significant challenge. Unlike traditional employees, you don’t receive employer-sponsored coverage, leaving you to navigate the complexities of the individual market. However, there are several strategies you can employ to find affordable options that meet your needs:

1. Explore the Marketplace: The Affordable Care Act (ACA) established health insurance marketplaces, where you can compare plans from different insurers. These marketplaces offer subsidies and tax credits to eligible individuals and families, potentially reducing your monthly premiums.

2. Consider a Health Savings Account (HSA): HSAs allow you to contribute pre-tax dollars to an account that can be used for healthcare expenses. This can be particularly advantageous for freelancers who may have higher deductibles on their plans, as you can use the HSA funds to offset out-of-pocket costs.

3. Explore Short-Term Health Insurance: For temporary gaps in coverage, short-term health insurance can provide an alternative. It’s often less expensive than traditional plans but may not cover all essential health services.

4. Consider Association Health Plans: Some professional organizations or trade associations offer group health insurance plans to their members, potentially providing more affordable rates.

5. Negotiate With Providers: Don’t be afraid to negotiate with healthcare providers, such as hospitals and clinics, for discounts or payment plans. You may also find lower-cost options at community health centers or free clinics for basic healthcare needs.

Finding affordable health insurance as a freelancer requires research and proactive planning. By exploring different options and utilizing available resources, you can secure coverage that protects your health and your financial well-being.

Protecting Your Business with Liability Insurance

As a freelancer or self-employed worker, you wear many hats. You’re the CEO, marketing team, and customer service representative all rolled into one. But one crucial role you shouldn’t neglect is safeguarding your business from potential risks. This is where liability insurance comes in, providing a crucial safety net in case of unforeseen circumstances.

Liability insurance acts as a shield, protecting you from financial repercussions if you’re sued for causing harm to someone or damaging their property. This could include things like:

- A client tripping over a piece of equipment at your workspace.

- A mistake in your work causing financial losses to a client.

- An online comment about a client causing reputational damage.

Without liability insurance, you could be personally responsible for covering legal fees, settlements, and other costs associated with these incidents, potentially jeopardizing your hard-earned savings and business stability.

Don’t underestimate the value of liability insurance. It’s an essential investment that provides peace of mind, allowing you to focus on growing your business knowing you’re protected from unforeseen events.

{kind=link}