Feeling overwhelmed by your finances? You’re not alone. Managing money can be a daunting task, especially when you’re juggling a busy life. But it doesn’t have to be a constant source of stress. With a few simple, actionable steps, you can significantly improve your financial well-being without sacrificing your precious time. This article will guide you through a proven strategy to optimize your finances with minimal effort, helping you reach your financial goals and live a more financially secure life.

From automating your savings to maximizing your income, we’ll explore effective strategies that require minimal effort but deliver big results. Discover how to unlock the power of automation, identify hidden savings opportunities, and build a robust financial foundation without spending hours on spreadsheets and calculations. Whether you’re a beginner or looking to take your finances to the next level, this article is packed with practical tips to simplify your money management and achieve your financial goals with ease.

Automating Your Savings and Bill Payments

In today’s fast-paced world, managing finances can feel like a constant juggling act. But what if you could take some of the stress out of it? Automating your savings and bill payments is a powerful tool that can help you optimize your finances with minimal effort.

Setting Up Automatic Savings: One of the biggest benefits of automation is that it forces you to save consistently. You can set up automatic transfers from your checking account to your savings account on a regular basis, such as weekly or monthly.

Automating Bill Payments: This feature ensures that your bills are paid on time, preventing late fees and damage to your credit score. With autopay, you can set up recurring payments for bills like your rent, utilities, credit card payments, and subscriptions.

Streamlined Financial Management: When you automate your savings and bill payments, you are essentially setting yourself up for success. You can free up your time and mental energy, allowing you to focus on other financial goals, like budgeting, investing, or debt reduction.

Choosing the Right Tools: Many banks and financial institutions offer automatic saving and bill payment services. You can also use third-party apps like Mint, YNAB, or Personal Capital to manage these functions.

Automating your finances is an easy and effective way to improve your financial well-being. By taking advantage of automation, you can save more, avoid late fees, and simplify your financial life.

Utilizing Budgeting Apps and Tools

In today’s digital age, there are countless budgeting apps and tools available to help you optimize your finances. These apps can automate many tasks, track your spending, set financial goals, and provide insights into your spending habits. Some popular options include Mint, Personal Capital, YNAB (You Need a Budget), and EveryDollar.

Benefits of using budgeting apps and tools include:

- Automatic tracking of transactions: Connect your bank accounts and credit cards to automatically track your income and expenses.

- Categorization of spending: Understand where your money is going by categorizing your spending into different areas like groceries, entertainment, and rent.

- Budgeting and goal setting: Create personalized budgets, set financial goals, and track your progress towards achieving them.

- Alerts and notifications: Receive alerts about upcoming bills, potential overspending, and low balances.

- Financial insights and reports: Analyze your spending habits, identify areas for improvement, and make informed financial decisions.

Choosing the right budgeting app or tool depends on your individual needs and preferences. Consider factors such as ease of use, features, cost, and compatibility with your financial institutions.

Negotiating Lower Bills and Interest Rates

One of the easiest ways to save money and optimize your finances is by negotiating lower bills and interest rates. Many people assume that these prices are set in stone, but that’s often not the case. Companies are often willing to negotiate, especially if you’re a loyal customer or are willing to switch providers.

Start by gathering your bills and identifying areas where you might be able to save. For example, you could try negotiating a lower rate on your cable, internet, or cell phone bill. You could also try negotiating a lower interest rate on your credit card or loan.

When negotiating, it’s important to be polite and respectful. Explain your situation and why you’re requesting a lower rate. Be prepared to walk away if you don’t get the deal you want. You can always try negotiating again later. Be aware of current market prices and be sure to do your research to ensure you’re getting a fair deal.

Here are a few tips for negotiating lower bills and interest rates:

- Be prepared to switch providers. Companies are more likely to negotiate with you if they know you’re willing to take your business elsewhere.

- Be polite and respectful. Companies are more likely to work with you if you’re courteous.

- Be willing to negotiate. Don’t be afraid to ask for what you want.

- Do your research. Know what other providers are charging for similar services or products.

- Be persistent. If you don’t get the deal you want, try again later.

Negotiating lower bills and interest rates can be a simple and effective way to save money. It may not seem like a lot, but these small savings can add up over time. Just remember to be polite, persistent, and prepared to walk away if you don’t get the deal you want.

Taking Advantage of Cashback Rewards and Discounts

One of the simplest yet often overlooked ways to improve your finances is by leveraging cashback rewards and discounts. These seemingly small perks can add up significantly over time, giving you more money in your pocket without requiring major lifestyle changes. It’s all about being smart with your spending and maximizing the value of every dollar.

Start by identifying the areas where you spend the most. This could be groceries, fuel, dining, or online shopping. Once you know where your money goes, you can research credit cards or programs that offer cashback rewards in those specific categories. You can find cards offering high cashback rates for travel, groceries, or even everyday spending.

Don’t forget about the power of discounts! Utilize apps that provide coupons and deals at your favorite stores. Many retailers also offer loyalty programs that reward you with points or discounts for repeat purchases. Take the time to look for promotional codes before making online purchases, and consider signing up for email newsletters from brands you regularly shop with.

By taking advantage of cashback rewards and discounts, you can effectively “earn” money back on your everyday purchases. These strategies require minimal effort but can make a real difference in your financial well-being. With a little planning and awareness, you can optimize your finances and achieve your financial goals more easily.

Investing in Low-Maintenance Index Funds

Investing can seem daunting, especially if you’re new to it. You might feel overwhelmed by the sheer number of options, the need for constant monitoring, and the risk of making the wrong choices. But there’s a simple and effective way to invest that requires minimal effort: investing in low-maintenance index funds.

Index funds are designed to track a specific market index, such as the S&P 500. They invest in a basket of securities that mirrors the index’s composition, providing broad market exposure with low management fees. This means you don’t have to spend hours researching individual stocks or worrying about market timing.

Here’s why investing in index funds is a great strategy for optimizing your finances with minimal effort:

- Passive Investing: Index funds are a form of passive investing, meaning they don’t require active management. This means you don’t need to spend time monitoring the market or adjusting your portfolio, freeing up your time and energy for other things.

- Low Fees: Index funds typically have lower expense ratios than actively managed funds, meaning you’ll pay less in fees over time. This allows more of your investment to grow and compound.

- Diversification: By investing in an index fund, you automatically diversify your portfolio across a wide range of securities, reducing your overall risk.

- Long-Term Growth: Historically, index funds have consistently delivered strong returns over the long term, making them a reliable way to build wealth.

If you’re looking to optimize your finances with minimal effort, investing in low-maintenance index funds is a simple and effective strategy to consider. It’s a great way to get started with investing, even if you have limited experience or time. Remember to consult a financial advisor if needed, to ensure your investment strategy aligns with your individual financial goals and risk tolerance.

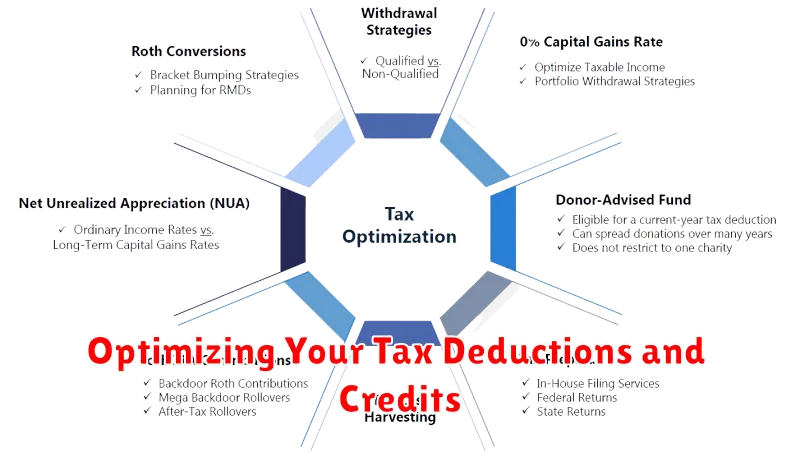

Optimizing Your Tax Deductions and Credits

Saving money and optimizing your finances doesn’t have to be a complicated, time-consuming process. One simple way to boost your financial well-being with minimal effort is by maximizing your tax deductions and credits. By taking advantage of these legal tax breaks, you can significantly reduce your tax liability and keep more of your hard-earned money in your pocket.

Here are some key tips to help you optimize your tax deductions and credits:

- Keep meticulous records: Gather all your relevant documentation, including receipts, invoices, and investment statements. This will help you accurately track your eligible expenses and claim the right deductions.

- Explore all available deductions: There are numerous deductions available based on your individual circumstances, such as medical expenses, charitable contributions, homeownership costs, and student loan interest. Research and understand which deductions you qualify for to maximize your savings.

- Utilize tax credits: Tax credits directly reduce your tax liability, dollar-for-dollar. Explore credits like the Earned Income Tax Credit (EITC), Child Tax Credit, or the American Opportunity Tax Credit. These credits can offer substantial savings, especially for low- and middle-income earners.

- Consider a tax professional: If you’re unsure about navigating the tax system or maximizing your deductions and credits, consult a qualified tax advisor. They can provide personalized guidance and ensure you claim all eligible benefits.

By implementing these strategies, you can significantly reduce your tax burden and improve your financial health. Remember, it’s essential to stay informed about current tax laws and regulations to ensure you’re taking advantage of all available opportunities. With a little effort, you can optimize your tax deductions and credits, leaving more money in your pocket and contributing to your overall financial well-being.

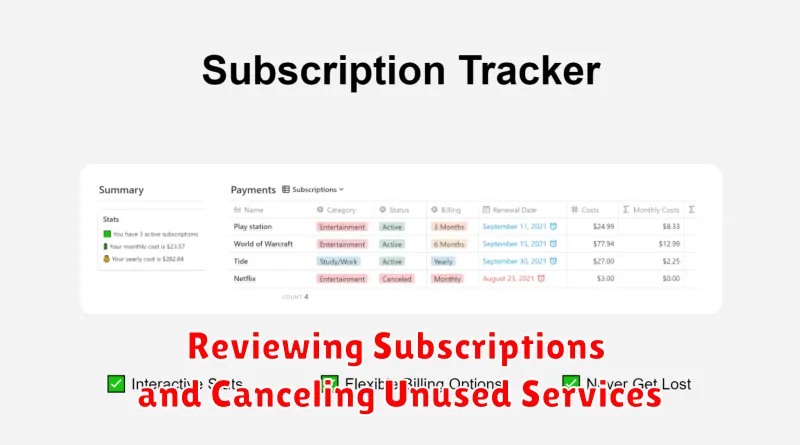

Reviewing Subscriptions and Canceling Unused Services

One of the easiest ways to optimize your finances is to take a look at your recurring subscriptions and cancel any you don’t actively use. Many of us sign up for services on a whim, forgetting about them as they silently drain our bank accounts. This is a common issue, and by taking the time to identify and eliminate these hidden expenses, you can free up significant funds.

Start by making a list of all your subscriptions, including streaming services, software programs, gym memberships, and anything else you pay for on a recurring basis. You can find this information by checking your bank statements, credit card bills, or by simply browsing through your email inbox. Once you have a comprehensive list, take a critical look at each item and ask yourself: Do I actively use this service? Is it worth the monthly cost?

If the answer to either of these questions is “no,” then it’s time to cancel. Many services offer a simple online process for canceling your subscription. If you’re struggling to find the cancellation instructions, contact the customer support team for assistance. By eliminating unnecessary subscriptions, you can free up money that can be used for other financial goals, like saving for retirement, paying off debt, or simply enjoying more financial freedom.

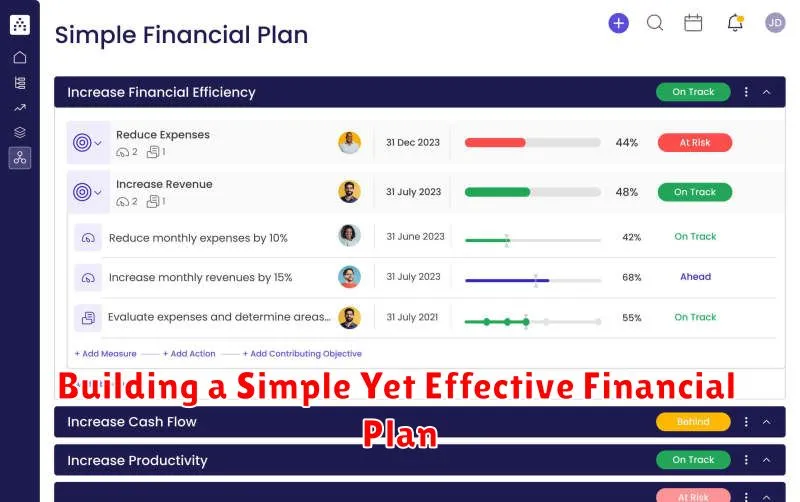

Building a Simple Yet Effective Financial Plan

A financial plan doesn’t have to be complicated to be effective. In fact, a simple yet well-structured plan can help you achieve your financial goals without overwhelming you. Here are the key components of a basic financial plan that you can start implementing right away:

1. Track Your Income and Expenses: The first step is to know where your money is going. Use a budgeting app, spreadsheet, or even a notebook to track your income and expenses for a month. This will give you a clear picture of your financial situation and identify areas where you can save.

2. Set Financial Goals: What do you want to achieve financially? Do you want to buy a house, pay off debt, or save for retirement? Setting specific, measurable, achievable, relevant, and time-bound (SMART) goals will provide you with direction and motivation.

3. Create a Budget: Based on your income and expenses, create a realistic budget that allocates funds to your different financial goals. Prioritize your needs and allocate discretionary spending responsibly.

4. Automate Your Savings: Set up automatic transfers to your savings accounts on a regular basis. This ensures that you are consistently saving towards your goals without having to remember to do it manually.

5. Review Regularly: Your financial situation and goals may change over time. It’s essential to review your budget and financial plan at least once a year to make adjustments as needed.

Building a simple yet effective financial plan is a powerful first step towards achieving your financial goals. It provides structure and clarity, enabling you to take control of your finances and make informed decisions about your money.

{kind=link}