Are you getting the most out of your employer benefits and compensation packages? Many employees don’t fully understand the value of their benefits and compensation, leaving valuable perks on the table. This can lead to financial strain and missed opportunities for personal growth and well-being. In today’s competitive job market, it’s crucial to know what you’re entitled to and how to maximize your total compensation.

By understanding the various components of your benefits and compensation package, you can make informed decisions about your financial well-being, career advancement, and overall life satisfaction. This article will guide you through a comprehensive approach to leveraging your employer benefits and maximizing your compensation, empowering you to take control of your financial future.

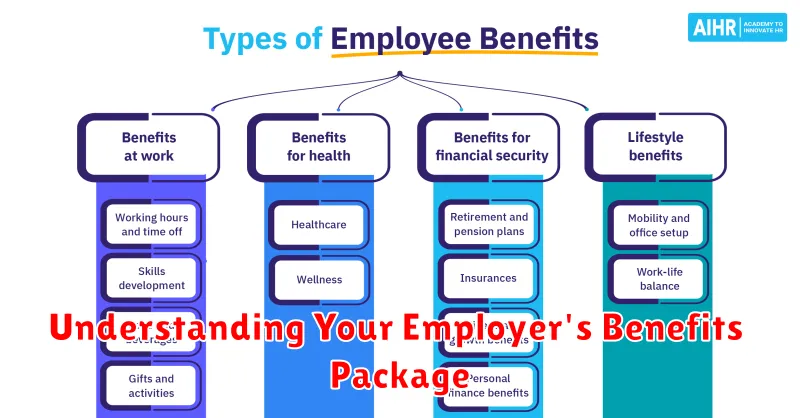

Understanding Your Employer’s Benefits Package

Beyond your salary, your employer offers a benefits package that can significantly impact your overall financial well-being and quality of life. It’s crucial to understand the ins and outs of this package to maximize its benefits. Your benefits package likely includes a variety of offerings, such as health insurance, dental and vision coverage, life insurance, disability insurance, paid time off, and retirement plans.

Take the time to review your employer’s benefits package thoroughly. Pay close attention to the details of each benefit, including:

- Coverage levels: What is the extent of coverage for each benefit?

- Deductibles and co-pays: How much will you be responsible for out-of-pocket?

- Eligibility requirements: What are the conditions for accessing each benefit?

- Open enrollment period: When can you make changes to your benefits selection?

Don’t hesitate to ask questions. Your human resources department or benefits administrator is there to provide clarification. Understanding the details of your benefits package empowers you to make informed decisions and maximize the value it offers.

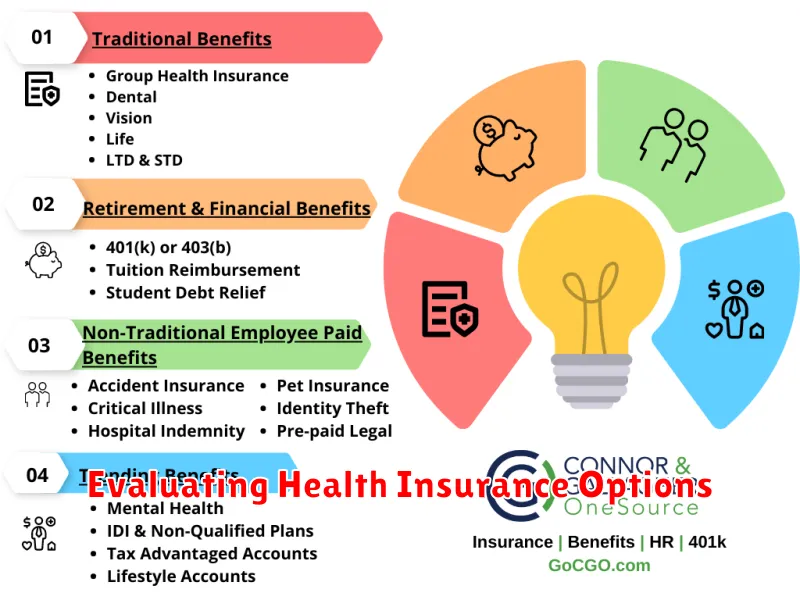

Evaluating Health Insurance Options

Your health insurance is a significant part of your overall compensation package. It can make a big difference in your overall financial well-being. You need to carefully evaluate the options available to you and choose the plan that best suits your needs and budget.

Here are some tips for evaluating your health insurance options:

- Understand your needs. Think about your current health status, your family’s health history, and any pre-existing conditions. Consider your expected healthcare expenses in the coming year.

- Compare plans. Look at the different plans offered by your employer and consider the following factors:

- Premium costs: How much will you have to pay out of pocket each month?

- Deductible: How much will you have to pay before your insurance coverage kicks in?

- Co-pays and coinsurance: How much will you have to pay for doctor visits, prescriptions, and other services?

- Network: Which doctors and hospitals are in the plan’s network?

- Coverage: What services are covered by the plan?

- Ask questions. Don’t hesitate to ask your HR department or your insurance provider any questions you have.

By taking the time to carefully evaluate your health insurance options, you can ensure that you are getting the best possible coverage for your needs.

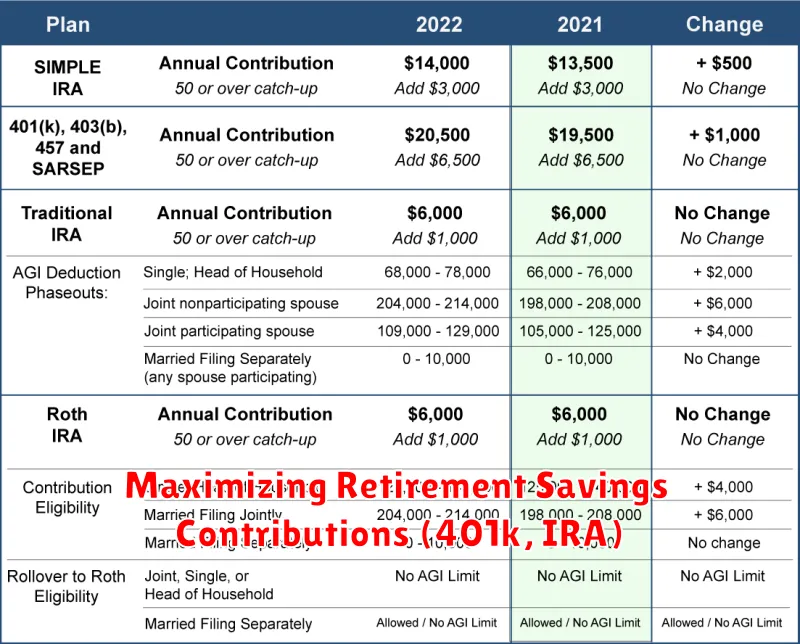

Maximizing Retirement Savings Contributions (401k, IRA)

One of the most valuable parts of an employer’s benefits and compensation package is retirement savings. This is because you can take advantage of tax-advantaged accounts like 401(k) and IRA to save for the future.

If your employer offers a 401(k) plan, consider contributing as much as possible to take full advantage of the matching contributions offered. Employers typically match a certain percentage of employee contributions, effectively giving you free money. This is essentially free money, so make sure you contribute enough to get the full match.

Additionally, consider contributing to an IRA. An IRA offers a tax deduction on contributions, which can significantly lower your current tax liability. It’s important to note that the contributions to both 401(k) and IRA are subject to annual limits.

Maximize your contributions by understanding the limits and considering any applicable catch-up contributions for those 50 and older. Start early and consistently contribute to your retirement savings plans to secure your financial future.

Taking Advantage of Employer-Sponsored Savings Plans (HSA, FSA)

Employer-sponsored savings plans, such as Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs), can be powerful tools for saving money on healthcare costs. These accounts allow you to set aside pre-tax dollars to cover eligible medical expenses, reducing your taxable income and potentially saving you money on taxes.

HSAs are available to those enrolled in a high-deductible health plan (HDHP). They offer tax-advantaged savings for healthcare expenses, with contributions growing tax-free and withdrawals used for qualified medical expenses being tax-free as well.

FSAs, on the other hand, are offered by employers to cover medical, dependent care, or other qualified expenses. They allow you to set aside pre-tax dollars for these expenses. While contributions are not tax-deductible, withdrawals are used tax-free for eligible expenses. However, unused funds in an FSA are often forfeited at the end of the year.

To maximize the benefits of these plans, consider the following:

- Contribute the maximum amount allowed: Taking full advantage of the contribution limits for HSAs and FSAs can significantly reduce your healthcare expenses.

- Use the funds for qualified expenses: Ensure you understand the eligible expenses for your specific plan to avoid penalties for non-qualified withdrawals.

- Keep track of your expenses: Maintain thorough records of your medical expenses to ensure you can properly claim reimbursements from your HSA or FSA.

- Explore options for rollover or carryover: Some plans allow for a limited rollover of unused HSA funds or a carryover of unused FSA funds into the next year.

By taking advantage of these employer-sponsored savings plans, you can effectively manage your healthcare costs and potentially save a considerable amount of money on taxes.

Utilizing Life Insurance and Disability Insurance Benefits

Life insurance and disability insurance are often overlooked benefits that can provide valuable financial security for you and your family. Life insurance, as the name suggests, provides a death benefit to your beneficiaries if you pass away. This can help cover funeral expenses, outstanding debts, and provide financial support for your loved ones. Disability insurance, on the other hand, provides income replacement if you become unable to work due to an illness or injury. This can help you maintain your lifestyle and cover your expenses while you are unable to work.

To make the most of these benefits, it’s crucial to understand the details of your employer’s plan. Consider the following:

- Coverage Amount: Determine if the life insurance coverage offered is sufficient for your needs. You may need to purchase additional coverage through a personal policy.

- Disability Benefit Period: Understand the duration of disability coverage offered by your employer. Is it short-term or long-term? You may want to consider supplemental disability coverage to ensure your financial stability in case of a long-term disability.

- Waiting Period: This is the time you must wait before benefits kick in after becoming disabled. Understand the waiting period and consider how it might impact your financial situation.

- Exclusions and Limitations: Review the policy’s exclusions and limitations carefully. Certain conditions or situations might not be covered.

By understanding these key details, you can make informed decisions about how to utilize these valuable benefits to safeguard your financial well-being and protect your family in case of an unexpected event.

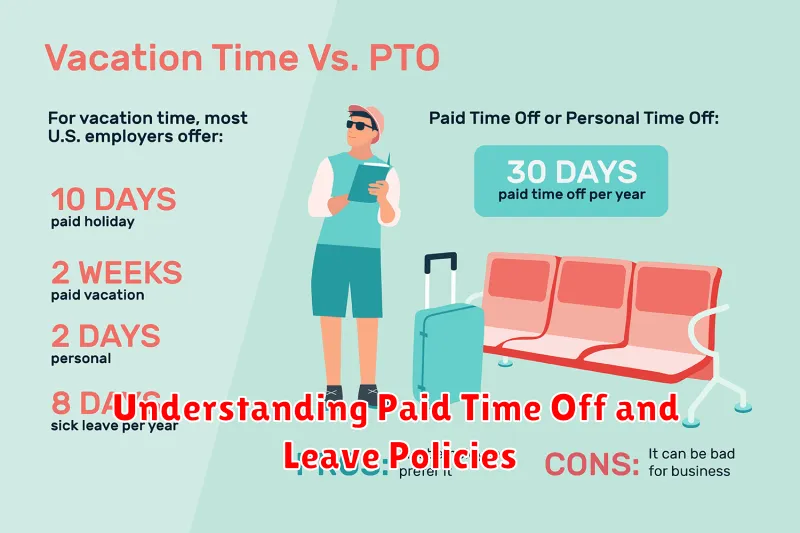

Understanding Paid Time Off and Leave Policies

Understanding your employer’s paid time off (PTO) and leave policies is crucial for maximizing your compensation package. These policies outline the types of leave you’re eligible for, the amount of time you can take, and the process for requesting and using this time. Knowing these details will help you plan for vacations, personal appointments, and other important events, ensuring that you’re using your benefits to their fullest potential.

Types of leave include:

- Vacation time: Allows employees to take time off for personal reasons, such as travel or leisure.

- Sick leave: Provides time off for illness or injury.

- Personal leave: Can be used for various reasons, including attending a family event, dealing with a personal emergency, or taking care of a sick family member.

- Family leave: Offers unpaid time off for parental leave, adoption, or to care for a sick family member.

- Bereavement leave: Provides time off for the death of a close family member.

It’s important to carefully review your employer’s policies to understand how each type of leave works, including:

- Accrual rates: How much PTO you earn per pay period.

- Carryover policies: Whether you can roll over unused PTO to the next year.

- Request procedures: How to submit leave requests and required documentation.

- Notification requirements: The amount of notice you need to provide for different types of leave.

By understanding your employer’s PTO and leave policies, you can make informed decisions about your time off, ensure you’re taking advantage of all the benefits you’re entitled to, and avoid any unexpected issues or complications.

Exploring Professional Development Opportunities

One of the most valuable aspects of a comprehensive benefits package is the inclusion of professional development opportunities. These opportunities can range from tuition reimbursement programs and certification sponsorships to access to online learning platforms and mentorship programs. Take advantage of these resources to enhance your skills, expand your knowledge, and advance your career within your company or in your field.

Tuition reimbursement programs can help you pursue higher education, which can lead to promotions, higher salaries, and greater job security. Certification sponsorships can demonstrate your commitment to professional development and can make you more competitive in the job market. Access to online learning platforms can provide you with flexible and convenient ways to learn new skills or deepen your expertise in specific areas. Mentorship programs can connect you with experienced professionals who can provide guidance and support as you navigate your career.

Proactively explore the professional development opportunities available to you and make the most of them. Don’t hesitate to reach out to your HR department or your manager to learn more about the programs and resources available to you.

Negotiating Your Compensation and Benefits Package

Negotiating your compensation and benefits package is a crucial aspect of securing a job that meets your financial and personal needs. It’s not just about getting the highest salary; it’s about crafting a package that addresses your individual priorities. Remember, you’re not just selling your skills, you’re selling yourself as a valuable asset to the company.

Research and Preparation: Before entering any negotiation, arm yourself with knowledge. Research industry benchmarks for your role and location. Understand the company’s financial health and compensation philosophy. Determine your minimum acceptable salary and non-negotiable benefits.

Communicate Your Value: During the interview process, highlight your skills, experience, and achievements that make you stand out. Quantify your accomplishments whenever possible to demonstrate the value you’ll bring to the company.

Be Proactive: Don’t wait for the employer to offer a package; take the initiative. During the final stages of the interview process, express your interest in the role and gently inquire about their compensation and benefits structure.

Be Prepared to Walk Away: If the employer isn’t willing to negotiate on your terms, be prepared to walk away. Your worth is not defined by the first offer; it’s about finding a company that values you and your contributions.

Negotiation Tactics:

- Focus on benefits that align with your priorities. This might include health insurance, retirement plans, paid time off, or professional development opportunities.

- Be open to creative solutions. Consider alternative forms of compensation like bonuses, equity, or flexible work arrangements.

- Remain calm and professional throughout the negotiation process. Focus on finding a mutually beneficial agreement.

Reviewing and Updating Your Benefits Regularly

Once you’ve enrolled in your benefits, don’t just forget about them. Your life situation is constantly changing, and your benefits should evolve with it. Make a habit of reviewing your benefits at least annually, or even more frequently if you experience significant life events like marriage, the birth of a child, or a change in your health status.

You may also need to make adjustments to your benefits if you experience a change in your income, dependents, or health needs. For example, if you receive a raise, you may want to consider increasing your 401(k) contributions. If you get married or have a child, you’ll likely need to add your spouse and child to your health insurance plan. And if you develop a chronic health condition, you may need to switch to a plan that offers more coverage for the specific treatments you need.

Don’t be afraid to ask your HR department for help in understanding your benefits and making necessary adjustments. They are there to assist you and ensure you are getting the most out of your benefits package.

{kind=link}