Feeling financially insecure? You’re not alone. Many of us struggle with the uncertainty of unexpected expenses. Life throws curveballs, from car repairs to medical emergencies, and it can be overwhelming to handle them without a financial safety net. This is where an emergency fund comes in. An emergency fund is a crucial financial tool that can give you peace of mind and protect you from financial hardship.

But what if you’re living on a limited income? Building an emergency fund may seem impossible. Don’t worry, it’s not! With careful planning and consistent effort, even those with limited income can start an emergency fund. This guide will provide practical tips and strategies to help you get started and achieve financial stability.

Why You Need an Emergency Fund

An emergency fund is a crucial financial safety net that can help you navigate unexpected life events without derailing your financial stability. It serves as a cushion to absorb financial shocks and prevent you from falling into debt or making hasty decisions during challenging times.

Imagine facing a sudden job loss, unexpected medical expenses, or a car breakdown. These situations can be incredibly stressful, especially when you’re already struggling to make ends meet. Without an emergency fund, you may be forced to rely on high-interest loans, deplete your savings, or even go without essential needs. This can lead to a domino effect of financial problems, making it even harder to recover.

An emergency fund provides peace of mind and financial security. It allows you to handle unexpected situations without panic, giving you time to find alternative solutions and regain control of your finances. It’s a powerful tool for building financial resilience and protecting your future.

Determining Your Emergency Fund Goal

The first step in building an emergency fund is to determine your goal amount. This will depend on your individual circumstances, but a good rule of thumb is to aim for 3-6 months’ worth of essential expenses. Essential expenses include things like rent, utilities, groceries, and transportation.

If you have a stable income and a low cost of living, you may be able to get by with a smaller emergency fund. However, if you have a variable income or a high cost of living, you’ll want to aim for a larger amount.

To calculate your emergency fund goal, simply add up your monthly essential expenses and multiply that number by 3, 4, 5, or 6, depending on how much of a cushion you want. For example, if your monthly essential expenses are $2,000, your emergency fund goal could be anywhere from $6,000 to $12,000.

It’s also important to consider any potential risks that could impact your finances, such as job loss, illness, or car repairs. If you’re concerned about these risks, you may want to aim for a larger emergency fund.

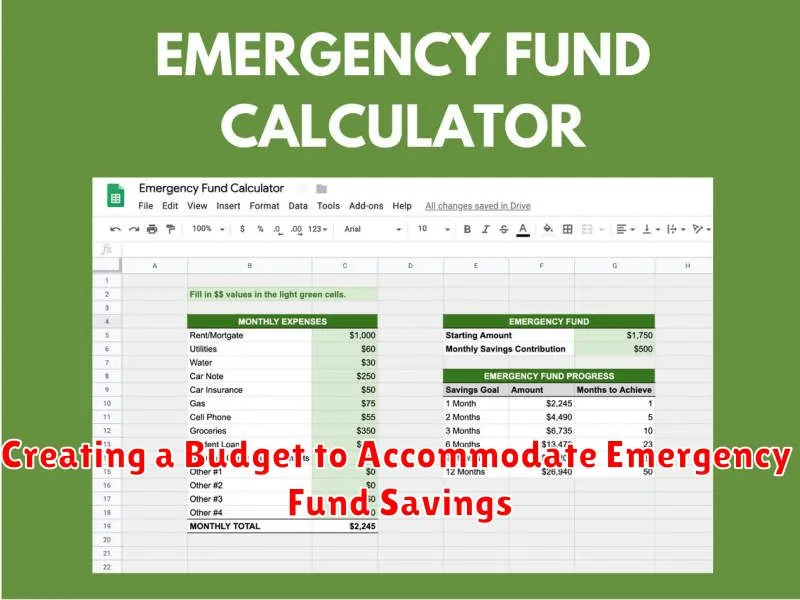

Creating a Budget to Accommodate Emergency Fund Savings

Building an emergency fund with a limited income can be challenging, but it’s essential. The first step is to create a budget that allows you to allocate funds for your emergency fund while still covering your essential expenses.

Start by tracking your expenses for a month to understand where your money is going. Categorize your spending and identify areas where you can cut back. Consider these tips:

- Dining Out: Reduce restaurant meals and cook more at home.

- Subscriptions: Evaluate subscriptions you don’t use regularly and cancel them.

- Entertainment: Limit non-essential entertainment spending like movie tickets or concerts.

Once you have a clear picture of your spending, prioritize essential expenses like rent, utilities, groceries, and transportation. Then, allocate a small amount of money each month to your emergency fund. Even saving $20 a week can add up over time.

Remember, creating a budget is an ongoing process. Review and adjust your budget regularly as your income or expenses change.

Finding Ways to Cut Expenses and Save More

Building an emergency fund on a limited income can feel daunting, but it’s achievable with a conscious effort to cut expenses and save more. It’s about prioritizing your needs and finding ways to trim the fat from your budget. This might mean making small changes to your daily habits, negotiating better rates for your services, or even exploring alternative solutions for your needs.

Start by identifying areas where you can cut back. Consider creating a detailed budget to track your income and expenses. Look for subscriptions or services you’re not fully utilizing. Challenge yourself to cook at home more often instead of eating out. Negotiate your cable or internet bill for a lower rate. Every small saving you make can add up to a substantial amount over time.

Remember, saving doesn’t always mean depriving yourself. It’s about finding a balance. You can still enjoy your hobbies and social outings, but perhaps find budget-friendly alternatives. Explore free activities like going for hikes, visiting local museums, or attending free community events. Even small changes in your spending habits can have a significant impact on your ability to build an emergency fund.

Exploring Additional Income Opportunities

Building an emergency fund on a limited income can feel daunting, but it’s achievable with a bit of creativity and resourcefulness. One of the most effective ways to boost your savings is to explore additional income opportunities. These side hustles or part-time jobs can provide a consistent stream of income, helping you reach your financial goals faster.

Consider these options:

- Freelancing: Leverage your skills in writing, graphic design, web development, or other fields to offer services on platforms like Upwork or Fiverr.

- Driving for a rideshare service: Set your own hours and earn money by transporting passengers. Platforms like Uber and Lyft are popular options.

- Online tutoring or teaching: If you have expertise in a particular subject, you can tutor students online through websites like TutorMe or Chegg.

- Selling crafts or handmade items: Utilize your artistic skills to create and sell products on platforms like Etsy or Shopify.

- Renting out a spare room: If you have extra space in your home, consider renting it out through Airbnb or other short-term rental platforms.

Remember to factor in the time commitment and expenses associated with each option. Choose a side hustle that aligns with your interests, skills, and available time.

Setting Up a Dedicated Savings Account for Your Emergency Fund

Once you’ve committed to building an emergency fund, the next step is to find the right place to store your savings. While you could simply put money in your checking account, it’s best to open a dedicated savings account for your emergency fund. This will help you keep track of your savings and prevent you from accidentally spending it on something else. Look for a high-yield savings account that offers a competitive interest rate and minimal fees. You want to make sure your emergency fund is growing as much as possible without being eaten away by bank charges. You might be able to find a bank that offers an account specifically for emergencies, or you can set up a regular savings account and label it as your emergency fund.

When choosing a savings account, consider these factors:

- Interest Rate: The higher the interest rate, the faster your emergency fund will grow.

- Fees: Some banks charge monthly maintenance fees or fees for withdrawing money early. Make sure to choose an account with minimal fees.

- Accessibility: You should be able to access your emergency fund quickly and easily in case of an unexpected expense.

It’s also a good idea to choose a savings account that is FDIC-insured. This means your money is protected by the federal government up to $250,000 per depositor, per insured bank. This will give you peace of mind knowing your savings are safe.

When you’ve opened your savings account, the next step is to start making regular contributions. You can choose a set amount to save each month, or you can make larger contributions when you can afford it. The key is to be consistent with your savings.

Automating Your Emergency Fund Contributions

One of the most effective ways to build an emergency fund with limited income is to automate your contributions. This involves setting up a system where a fixed amount of money is automatically transferred from your checking account to your savings account on a regular basis. This could be weekly, bi-weekly, or monthly, depending on your budget and income flow.

Here are some benefits of automating your emergency fund contributions:

- Consistency: You are less likely to miss contributions when they are automated. This ensures steady progress towards your savings goal.

- Time-Saving: Automating eliminates the need for manual transfers, freeing up your time and energy for other things.

- Discipline: It encourages financial discipline by making it easier to save consistently. Even small contributions can add up over time.

- Reduced Temptation: You are less likely to spend the money if it’s automatically transferred to a separate account.

Most banks and financial institutions offer online tools for setting up automatic transfers. You can also consider using a personal finance app to manage your savings goals. To set up automation, you’ll need to create a high-yield savings account dedicated to your emergency fund and then link it to your checking account. Once connected, schedule regular automatic transfers based on your budget.

Automating your emergency fund contributions takes the guesswork out of saving and ensures you consistently build a safety net. It’s a simple yet powerful strategy for those with limited income, and it can be a crucial step toward financial security.

Building Your Emergency Fund Gradually

It’s a common misconception that you need a huge chunk of money to start an emergency fund. You don’t! The key is to start small and build it up gradually. Even if you can only afford to save $5 or $10 a week, it’s a start. The goal is to develop a consistent saving habit.

Consider setting up an automatic transfer from your checking account to your savings account. This will help you save without even thinking about it. Many banks also offer apps and online tools that help you track your spending and savings. Use these resources to your advantage.

Remember, building an emergency fund is a marathon, not a sprint. Don’t get discouraged if you don’t see results immediately. Stay consistent and focus on making small, achievable goals. Over time, your emergency fund will grow, and you’ll be prepared for any unexpected expenses life throws your way.

Replenishing Your Emergency Fund After Use

After you’ve used your emergency fund, it’s crucial to replenish it as soon as possible to ensure you’re prepared for future unexpected events. Here’s how to do it:

1. Prioritize Saving: Make replenishing your emergency fund a top priority. Create a budget and allocate a specific amount each month to rebuild your savings. Even small contributions can make a big difference over time.

2. Review Your Expenses: Look for areas where you can cut back on spending. This could include reducing subscriptions, dining out less, or finding more affordable alternatives.

3. Consider Side Hustles: Take on a part-time job or freelance work to earn extra income. This can accelerate your savings and help you rebuild your emergency fund faster.

4. Automate Savings: Set up automatic transfers from your checking account to your savings account. This will ensure you consistently contribute to your emergency fund without having to manually transfer funds.

5. Track Your Progress: Monitor your savings regularly and celebrate your milestones. Seeing your emergency fund grow can motivate you to stay committed to your saving goals.

Replenishing your emergency fund may take time, but with a consistent plan and disciplined saving habits, you’ll be well-prepared for the unexpected.

{kind=link}