Are you looking for a way to invest your money consistently and strategically? Then you need to learn about dollar-cost averaging. This investment strategy involves investing a fixed amount of money at regular intervals, regardless of the market’s fluctuations. This method can help you mitigate risk and potentially maximize your returns over time.

Dollar-cost averaging is a popular strategy for both seasoned investors and newcomers to the market. By spreading out your investments, you can avoid the pitfalls of trying to time the market, a notoriously difficult task. With dollar-cost averaging, you buy more shares when prices are low and fewer shares when prices are high, effectively averaging your cost per share over time.

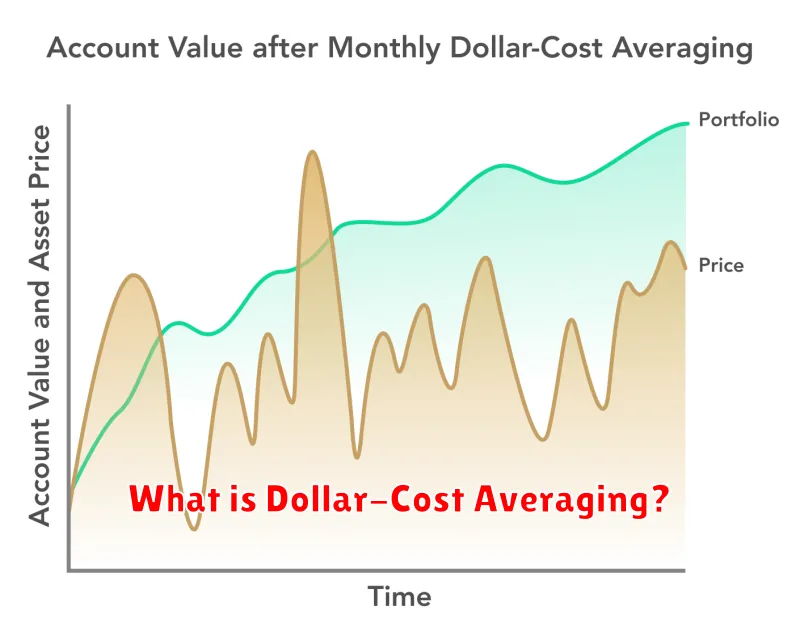

What is Dollar-Cost Averaging?

Dollar-cost averaging (DCA) is an investment strategy where you invest a fixed amount of money in a particular asset at regular intervals, regardless of the asset’s price. Instead of investing a lump sum at one time, you spread out your investments over time, buying more when prices are low and less when prices are high. This strategy helps to reduce the impact of market volatility and can lead to a lower average purchase price for your investments.

For example, let’s say you decide to invest $100 per month in a particular stock. If the stock price is $50 per share in month one, you’ll buy two shares. If the stock price drops to $40 per share in month two, you’ll buy 2.5 shares. In month three, if the stock price goes back up to $60 per share, you’ll buy 1.67 shares. By investing a fixed amount each month, you’re able to buy more shares when the price is low and fewer shares when the price is high. This helps to average out your purchase price and potentially reduce your overall investment risk.

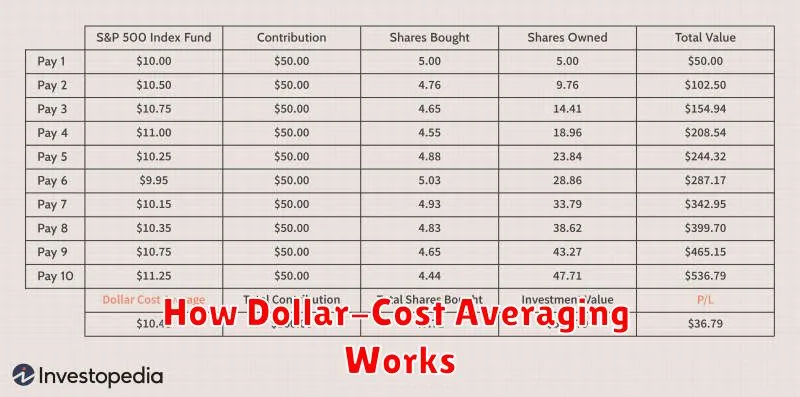

How Dollar-Cost Averaging Works

Dollar-cost averaging (DCA) is a simple investment strategy that involves investing a fixed amount of money at regular intervals, regardless of the market’s current price. This strategy aims to reduce the impact of market volatility on your investment returns by averaging out the cost of your investments over time.

For example, if you invest $100 per month in a particular stock, you’ll buy more shares when the price is low and fewer shares when the price is high. This helps to mitigate the risk of buying at the top of the market and losing money when the price declines.

The key to DCA is consistency. By investing a fixed amount at regular intervals, you’ll automatically buy more shares when the price is low and fewer shares when the price is high, effectively reducing the average cost of your investment.

Benefits of Dollar-Cost Averaging

Dollar-cost averaging (DCA) is an investment strategy that involves investing a fixed amount of money at regular intervals, regardless of the market’s current price. This strategy can be particularly beneficial for long-term investors, as it helps to mitigate the risks associated with market volatility. Here are some of the key benefits of using DCA:

Reduces the risk of market timing: Trying to time the market can be a difficult and risky endeavor, and attempting to buy low and sell high often backfires. DCA helps to avoid this problem by averaging the purchase price over time. Since you’re buying consistently, regardless of the price, you’re less likely to get caught in a downward trend, or miss out on a positive run.

Helps to avoid emotional decision-making: Market fluctuations can trigger emotional reactions, leading to impulsive investment decisions that may not be in your best interest. DCA helps to remove this emotional component by taking the pressure off of making perfect market timing calls. You’re simply committing to your investment strategy, regardless of what the market is doing.

Reduces overall investment risk: Because you are buying consistently, you are less likely to invest all of your capital at a market peak. This helps to reduce the potential for losses, as you will have purchased shares at both higher and lower prices, averaging out your overall investment cost.

Promotes a disciplined approach to investing: By investing a fixed amount at regular intervals, DCA encourages a disciplined approach to investing. This can help you stay on track with your financial goals, even when the market is volatile.

Risks of Dollar-Cost Averaging

While dollar-cost averaging is generally considered a sound investment strategy, it’s not without its risks. Here are a few key considerations:

1. Potential for Missing Out on Market Gains: Dollar-cost averaging involves investing a fixed amount of money at regular intervals. This means you’re buying more shares when prices are low and fewer shares when prices are high. While this helps mitigate losses in a declining market, it can also prevent you from fully capturing gains during a bull market. If the market experiences a significant upward surge, your average purchase price might be lower than the market price, resulting in missing out on potential profits.

2. Time Horizon and Market Volatility: Dollar-cost averaging works best over a long-term investment horizon. Short-term market fluctuations can impact the strategy’s effectiveness. If you need to access your funds quickly, you might end up selling investments at a loss due to market volatility, especially if you’re investing in volatile assets like stocks.

3. Individual Stock Performance: While dollar-cost averaging helps mitigate overall market risk, it doesn’t protect you from the specific risks associated with individual stocks. If you choose to invest in a particular company whose performance deteriorates significantly, even with dollar-cost averaging, you could still experience substantial losses.

4. Lack of Flexibility: Dollar-cost averaging involves a predetermined investment schedule. It may limit your ability to adjust your investment strategy based on changing market conditions. For example, if you anticipate a sharp market downturn, you might want to temporarily pause your investments. However, with dollar-cost averaging, you’re committed to investing at regular intervals.

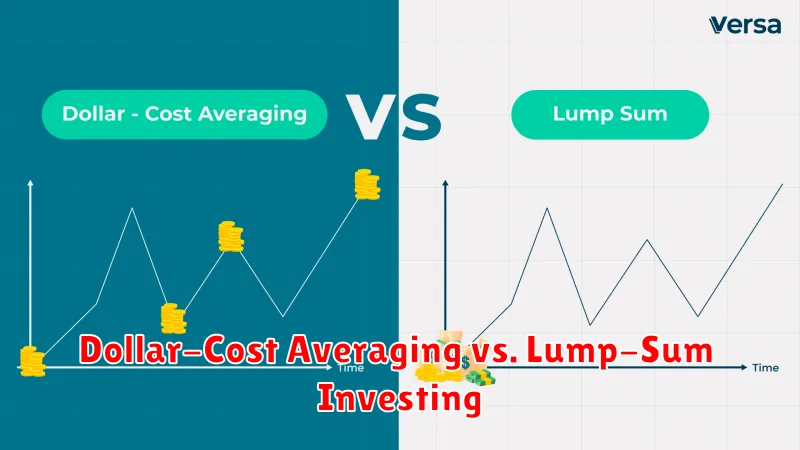

Dollar-Cost Averaging vs. Lump-Sum Investing

When it comes to investing, one of the most common questions investors ask is whether they should invest a lump sum or use dollar-cost averaging. Both strategies have their own advantages and disadvantages, and the best approach will depend on your individual circumstances and risk tolerance.

Lump-sum investing involves investing a large sum of money all at once. This can be a good strategy if you have a significant amount of money to invest and believe that the market is likely to go up in the long term. However, it can also be risky, as you could lose money if the market declines immediately after you invest.

Dollar-cost averaging, on the other hand, involves investing a fixed amount of money at regular intervals, regardless of the market price. This can help to reduce the risk of investing at the wrong time, as you will be buying more shares when the price is low and fewer shares when the price is high. However, it can also mean that you may miss out on potential gains if the market rises significantly during the period in which you are investing.

So, which strategy is right for you? There is no easy answer, and the best approach will depend on your individual circumstances and risk tolerance. If you are a risk-averse investor and are worried about market volatility, dollar-cost averaging may be a good option for you. However, if you are willing to take on more risk and believe that the market is likely to go up in the long term, lump-sum investing may be a better choice.

How to Implement Dollar-Cost Averaging

Dollar-cost averaging is a strategy that involves investing a fixed amount of money at regular intervals, regardless of the market’s current price. This helps to average out your purchase price over time, reducing the impact of market volatility.

Here’s how to implement dollar-cost averaging:

- Determine your investment amount: Start by deciding how much you want to invest each month or quarter. This amount should be comfortable for you and fit within your overall financial goals.

- Choose your investment: Select a specific investment, such as a mutual fund, exchange-traded fund (ETF), or individual stocks.

- Set up an automatic investment plan: Many investment platforms allow you to automate your investments. This can help ensure that you invest regularly, regardless of how busy you are.

- Be patient and consistent: Dollar-cost averaging is a long-term strategy. It’s important to stick with your plan and avoid getting caught up in short-term market fluctuations.

By implementing dollar-cost averaging, you can help reduce the impact of market volatility and potentially increase your returns over time.

Choosing Investments for Dollar-Cost Averaging

Dollar-cost averaging (DCA) is a strategy that involves investing a fixed amount of money at regular intervals, regardless of market conditions. This strategy can be a great way to reduce the risk of investing in a volatile market. However, choosing the right investments for DCA is important.

Here are some factors to consider when choosing investments for DCA:

- Your investment goals: What are you hoping to achieve with your investments? Are you saving for retirement, a down payment on a house, or something else?

- Your risk tolerance: How comfortable are you with the possibility of losing money?

- Your time horizon: How long do you plan to invest your money?

- Investment type: There are various types of investments you can use for DCA such as mutual funds, ETFs, and stocks. Consider the type of investment that is best aligned with your financial goals, risk tolerance, and investment timeline.

Once you have considered these factors, you can start to narrow down your investment choices. You can also do research and learn more about different investment options before making any decisions.

Dollar-Cost Averaging in Different Market Conditions

Dollar-cost averaging (DCA) is a strategy that involves investing a fixed amount of money at regular intervals, regardless of the market conditions. This approach can help to reduce the impact of market volatility and potentially improve returns over time. However, the effectiveness of DCA can vary depending on the market conditions.

In a bull market, where prices are steadily rising, DCA may not be as effective as investing a lump sum at the beginning. This is because you are buying assets at higher prices over time. However, DCA can help to mitigate the risk of buying at the peak of the market and experiencing a sudden downturn.

In a bear market, where prices are falling, DCA can be a more effective strategy. By buying assets at regular intervals, you are able to average down the purchase price and benefit from potential future price increases. This is because you are buying more assets when they are cheaper.

In a volatile market, where prices fluctuate significantly, DCA can help to reduce the impact of these fluctuations. By investing a fixed amount at regular intervals, you are effectively smoothing out your average purchase price. This can help to protect your portfolio from sudden market drops.

It is important to note that DCA is not a guaranteed way to make money. It is a strategy that aims to reduce risk and improve returns over time. However, it does not eliminate the risk of losing money, and it is essential to do your research and understand the risks involved before investing.

Common Dollar-Cost Averaging Mistakes to Avoid

Dollar-cost averaging (DCA) is a popular investment strategy that involves investing a fixed amount of money at regular intervals, regardless of market fluctuations. While DCA can be a helpful tool for long-term investors, it’s essential to avoid common mistakes that can undermine its effectiveness.

One common mistake is failing to diversify your investments. DCA can be a great strategy for buying into a specific asset class, such as stocks or bonds, but it’s important to spread your money across different asset classes to mitigate risk. If you only invest in one asset class and that class performs poorly, your entire portfolio could suffer.

Another mistake is stopping DCA too soon. If you’re using DCA to buy into a market that’s been declining, it might be tempting to stop investing when you see the market bottoming out. However, this could mean missing out on the potential upside as the market recovers. It’s important to stick to your DCA plan and continue investing regularly, even when the market isn’t moving in your favor.

Finally, DCA isn’t a magic bullet. It can help to smooth out your returns and reduce the impact of market volatility, but it won’t guarantee profits. There are still risks involved with investing, and it’s important to understand that DCA is a long-term strategy that requires patience and discipline.

Dollar-Cost Averaging and Long-Term Financial Goals

Dollar-cost averaging (DCA) is a strategy where you invest a fixed amount of money at regular intervals, regardless of market fluctuations. This approach can help you achieve your long-term financial goals by smoothing out the effects of market volatility and reducing the risk of buying high and selling low.

DCA is particularly beneficial when you have a long investment horizon. It allows you to buy more shares when prices are low and fewer shares when prices are high, resulting in an average cost per share that is lower than if you had invested a lump sum at a single point in time. This strategy is particularly relevant for those looking to achieve goals like:

- Retirement savings: DCA can help you accumulate wealth over time, even if you start investing late in life.

- Down payment for a house: Investing regularly with DCA can build a sizable nest egg for a down payment on a property.

- Education expenses: DCA can help you save for your child’s college education.

By adopting a disciplined DCA approach, you can build a solid financial foundation that can weather market ups and downs, enabling you to reach your long-term financial goals.

{kind=link}