In today’s economy, it’s more crucial than ever to make your money work for you. With inflation soaring, interest rates fluctuating, and the stock market feeling unsteady, it’s easy to feel overwhelmed and unsure about how to manage your finances. But don’t fret! There’s a powerful tool at your disposal that can help you secure your future: high-interest accounts.

These accounts can offer a significant advantage over traditional savings accounts, allowing your money to grow at a faster pace and potentially outpacing inflation. By learning how to leverage these accounts effectively, you can unlock the potential to maximize your savings and achieve your financial goals. So, let’s dive into the world of high-interest accounts and discover how you can make your money work harder for you.

Understanding High-Interest Accounts and Their Benefits

High-interest accounts, also known as high-yield savings accounts, are savings accounts that offer a higher interest rate than traditional savings accounts. This means your money grows faster, allowing you to earn more interest over time.

The primary benefit of high-interest accounts is the potential for higher returns. Since they offer higher interest rates, your savings will grow more quickly than in a standard savings account. This can make a significant difference, especially over the long term.

Another advantage is their FDIC insurance. Like traditional savings accounts, high-interest accounts are typically insured by the FDIC up to $250,000 per depositor, per insured bank. This means your money is protected from loss in case of a bank failure.

Lastly, high-interest accounts are generally accessible. You can often access your money quickly and easily through online banking, mobile apps, or ATM withdrawals. This makes them a convenient option for saving money while also having access to your funds when you need them.

Types of High-Interest Accounts: Savings, Checking, and Money Market

When it comes to maximizing your savings, choosing the right type of account is crucial. High-interest accounts offer better returns compared to traditional savings accounts. Let’s explore three popular options: savings accounts, checking accounts, and money market accounts.

Savings Accounts are designed for storing your money for the long term. They typically offer higher interest rates than traditional savings accounts and allow for limited withdrawals. They are ideal for building an emergency fund, saving for retirement, or achieving a specific financial goal.

Checking Accounts are designed for everyday transactions, such as paying bills and making purchases. While some checking accounts offer high interest rates, they often come with limitations on withdrawals or minimum balance requirements. These accounts are best for those who value convenience and frequent access to their funds.

Money Market Accounts (MMAs) combine the features of savings and checking accounts. They offer higher interest rates than traditional savings accounts and provide limited check-writing privileges. MMAs require a higher minimum balance than savings accounts, but they can provide a better return on your savings while still allowing for some flexibility.

Ultimately, the best high-interest account for you depends on your individual financial needs and goals. Consider factors such as interest rates, fees, minimum balance requirements, and withdrawal limitations before making a decision.

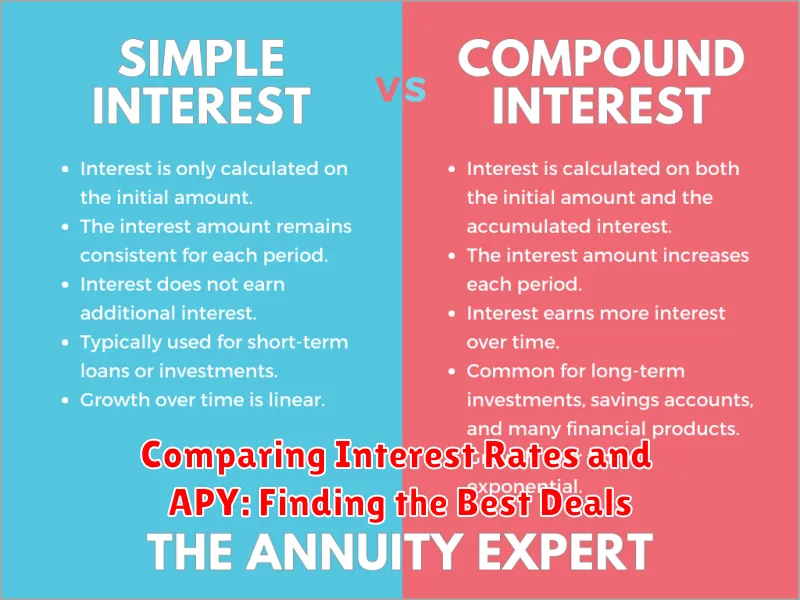

Comparing Interest Rates and APY: Finding the Best Deals

When choosing a high-interest savings account, understanding the difference between interest rates and Annual Percentage Yield (APY) is crucial. While both relate to the earnings on your savings, they represent different aspects of your potential return.

The interest rate is the base percentage that a financial institution offers on your deposits. It’s the fundamental rate that determines how much interest you’ll earn. However, this rate is usually presented as a simple annual rate, without considering compounding.

APY, on the other hand, reflects the actual amount of interest you earn over a year, taking into account compounding. Compounding means that the interest earned is added to your principal, and then the next interest calculation is made on the new, larger balance. This results in a snowball effect, leading to higher overall returns.

Therefore, when comparing different high-interest accounts, focus on the APY rather than just the interest rate. A higher APY generally indicates a better deal as it accounts for the full potential of your earnings through compounding.

For instance, two accounts might offer the same interest rate of 1%. However, one account might compound interest monthly, resulting in a higher APY, while another might compound quarterly, resulting in a lower APY.

By comparing APYs, you can ensure you’re getting the most out of your savings. Look for accounts with higher APYs to maximize your returns and accelerate your savings journey.

Factors Affecting Interest Rates: Federal Reserve Policy and Market Conditions

Understanding the factors that influence interest rates is crucial for maximizing your savings. Two key players in this game are the Federal Reserve (also known as the Fed) and the market conditions.

The Fed, as the central bank of the US, has a significant role in shaping interest rates. They use tools like setting the federal funds rate, which influences the interest rates banks charge each other for overnight lending. This rate, in turn, affects other interest rates, including those offered on savings accounts.

Market conditions also play a crucial role. When the economy is strong, with low unemployment and high consumer spending, the Fed tends to raise interest rates to control inflation. Conversely, during periods of economic weakness, the Fed may lower rates to stimulate borrowing and economic activity.

Inflation is another key factor. When inflation is high, lenders demand higher interest rates to compensate for the declining purchasing power of money. In contrast, low inflation allows for lower interest rates.

It’s essential to keep an eye on these factors to understand how they may affect your savings account interest rates. By understanding the forces shaping interest rates, you can better position yourself to maximize your savings.

Online Banks vs. Traditional Banks: Pros and Cons of Each

Choosing the right bank for your savings can be a big decision. When considering high-interest accounts, it’s crucial to weigh the pros and cons of both online banks and traditional banks.

Online banks, also known as digital banks, operate solely online, eliminating the need for physical branches. They often offer higher interest rates on savings accounts because they have lower overhead costs than traditional banks. Their convenience is another major advantage, allowing you to manage your finances from anywhere with internet access. However, online banks may lack the personal touch and in-person services that traditional banks provide.

Traditional banks, on the other hand, have a long history and a physical presence in the community. They often offer more comprehensive financial products and services, such as loans, mortgages, and investment accounts, in addition to savings accounts. The personal interaction with bank representatives can be a valuable asset, especially for complex financial needs. However, traditional banks may charge higher fees and offer lower interest rates than online banks due to their higher operational costs.

Ultimately, the best choice depends on your individual needs and preferences. If you prioritize convenience and high interest rates, an online bank might be the better option. If you prefer personalized service and a wider range of financial products, a traditional bank might be more suitable.

Features to Look for in a High-Interest Account: Fees, Minimum Balances, and ATM Access

High-interest accounts are a great way to maximize your savings. When choosing a high-interest account, it’s important to consider all the features and compare them to other options to make sure you’re getting the best deal. Here are some key features to look for:

Fees: Many high-interest accounts come with fees. Make sure you understand what fees are associated with the account and how they are charged. This includes monthly maintenance fees, ATM fees, and fees for making transfers.

Minimum Balances: Some high-interest accounts have a minimum balance requirement. This means you need to keep a certain amount of money in the account to earn the highest interest rate. It’s important to consider if you can maintain the minimum balance required.

ATM Access: You want to make sure the bank you choose offers a convenient way to access your money. Consider whether you have access to ATMs in your local area or whether you can make withdrawals at other banks without incurring fees.

By considering these key features, you can choose a high-interest account that meets your needs and helps you maximize your savings.

Strategies for Maximizing Interest Earnings: Automation and Compound Growth

High-interest savings accounts are a great way to grow your savings, but it’s essential to make sure you’re maximizing your interest earnings. Two powerful strategies to consider are automation and compound growth.

Automation involves setting up automatic transfers from your checking account to your high-interest savings account. This ensures you’re consistently adding to your savings and taking advantage of the higher interest rate. Consider setting up a recurring transfer on a regular schedule, like weekly or monthly, to make this process effortless.

Compound growth is the magic of earning interest on your interest. The longer your money stays in your high-interest savings account, the more interest you’ll earn, and the more interest you’ll earn on that interest. This snowball effect can significantly boost your savings over time. Aim to leave your savings untouched as much as possible to allow compound growth to work its magic.

By combining automation and compound growth, you can create a powerful system for maximizing your interest earnings. By consistently adding to your savings and allowing your money to compound, you’ll be well on your way to reaching your financial goals.

Protecting Your Savings: FDIC Insurance and Account Security

When you’re looking for the best way to maximize your savings, a high-interest account is often a top choice. However, it’s equally important to ensure that your money is safe and secure. This is where the Federal Deposit Insurance Corporation (FDIC) comes in.

The FDIC is an independent agency of the United States government that insures deposits in banks and savings associations. This means that if a bank fails, the FDIC will protect your deposits up to $250,000 per depositor, per insured bank, for each account ownership category. This protection includes checking accounts, savings accounts, money market accounts, and certificates of deposit (CDs).

To ensure your savings are covered, you should choose a bank that is FDIC-insured. You can easily check if a bank is insured by looking for the FDIC logo on their website or at their physical location. It’s also important to understand the different account ownership categories that the FDIC uses for insurance coverage, as this can impact the total amount of insured deposits you have. For example, if you have joint accounts or trust accounts, you may have different coverage limits.

In addition to FDIC insurance, you can further protect your savings by taking some extra steps:

- Choose a reputable bank or credit union with a strong track record of financial stability.

- Set strong passwords and enable two-factor authentication for online banking.

- Monitor your account activity regularly for any suspicious transactions.

- Keep your personal information safe and avoid sharing it with strangers.

By taking these steps, you can rest assured that your hard-earned savings are well-protected. It’s also a good idea to diversify your savings by holding some assets outside of traditional bank accounts, such as in investments or real estate. This can help to further reduce your risk and provide you with peace of mind.

The Role of High-Interest Accounts in an Emergency Fund

An emergency fund is crucial for financial stability, offering a safety net for unexpected expenses. A high-interest savings account plays a vital role in maximizing your emergency fund’s potential. These accounts offer a higher interest rate compared to traditional savings accounts, allowing your savings to grow faster.

Imagine facing an unexpected car repair or medical bill. With a robust emergency fund in a high-interest account, you’ll have the financial cushion to handle these situations without incurring debt. This peace of mind is invaluable, allowing you to focus on resolving the issue rather than worrying about finances.

Moreover, high-interest accounts provide a secure and accessible way to store your emergency fund. Funds are readily available when needed, providing quick access to your savings in case of unforeseen circumstances.

While high-interest accounts may offer a slightly higher interest rate than traditional savings accounts, it’s important to note that the difference may not be substantial. However, every little bit counts, especially when it comes to growing your emergency fund over time. The added interest earned can make a significant difference in the long run.

When choosing a high-interest account, it’s crucial to consider factors like interest rates, minimum deposit requirements, and any fees associated with the account. Comparing different options from various banks and credit unions can help you find the best fit for your needs.

Using High-Interest Accounts for Short-Term Savings Goals

High-interest savings accounts (HISAs) are a great option for short-term savings goals because they offer a higher interest rate than traditional savings accounts. This means that your money will grow faster, allowing you to reach your goal sooner. Some common short-term savings goals that can be achieved through HISAs include:

- Emergency fund: This is a crucial savings goal that can help you cover unexpected expenses, such as medical bills or car repairs.

- Down payment: If you are planning to buy a house or a car, you can use a HISA to save for your down payment.

- Vacation: A HISA can help you save for a dream vacation, whether it’s a weekend getaway or a longer trip.

- Large purchase: If you are planning to make a large purchase, such as a new appliance or a piece of furniture, a HISA can help you save up the money quickly.

When choosing a HISA, it is important to consider the following factors:

- Interest rate: Look for a HISA with a high interest rate, as this will maximize your returns.

- Fees: Some HISAs may charge monthly fees, so be sure to factor these into your decision.

- Minimum deposit: Some HISAs have a minimum deposit requirement, so make sure you are comfortable with this before opening an account.

By taking advantage of the high interest rates offered by HISAs, you can accelerate your savings and achieve your short-term financial goals faster. Remember to do your research and compare different options before choosing a HISA that best suits your needs.

Making the Most of Your High-Interest Savings: Tips and Tricks

High-interest savings accounts offer a fantastic way to grow your money faster than traditional savings accounts. However, simply opening an account isn’t enough to fully reap the benefits. To truly maximize your savings, consider these key tips and tricks.

1. Choose the Right Account: Start by comparing different high-interest savings accounts offered by various banks and credit unions. Look for accounts with competitive interest rates, minimal fees, and convenient online banking features. Research the bank’s reputation and ensure it’s FDIC-insured for peace of mind.

2. Maximize Your Deposits: The more you deposit, the more interest you earn. Make regular contributions to your high-interest savings account, even if they’re small amounts. Consider automating transfers from your checking account to your high-interest savings account on a regular schedule.

3. Take Advantage of Bonuses: Many banks offer sign-up bonuses for new account holders. These bonuses can be a significant boost to your initial savings. Make sure you meet the bonus requirements and understand any limitations.

4. Avoid Early Withdrawals: While you can access your savings whenever needed, remember that withdrawing funds early can negate the benefits of interest accrual. Try to resist dipping into your high-interest savings for everyday expenses and only access them for planned, long-term goals.

5. Consider a High-Yield CD: If you have funds you don’t need immediate access to, consider a high-yield certificate of deposit (CD). CDs offer fixed interest rates for a set period, typically with higher rates than savings accounts. Be aware of the penalties associated with early withdrawals.

By diligently following these tips, you can harness the power of high-interest savings accounts to effectively grow your money and achieve your financial goals faster.

{kind=link}