Retirement may seem like a distant dream, but it’s never too early to start planning. The sooner you begin saving, the more time your money has to grow and the more comfortable your life will be in retirement. There are many ways to boost your retirement savings, and it’s important to find a strategy that works for you. This guide will explore some of the best ways to boost your retirement savings and help you reach your financial goals.

From maximizing contributions to taking advantage of tax benefits, there are a number of strategies that can help you significantly increase your retirement nest egg. By understanding these options and making informed decisions, you can set yourself up for a secure and comfortable future. Let’s delve into some of the effective methods for boosting your retirement savings and discover how you can make the most of your money.

Understanding Your Current Savings Rate

Knowing your current savings rate is crucial to determining how well you’re on track to reach your retirement goals. It’s simply the percentage of your income that you’re saving for retirement. To calculate it, divide your annual retirement contributions by your gross annual income. For example, if you earn $50,000 per year and contribute $5,000 to your retirement accounts, your savings rate is 10% (5,000/50,000 x 100).

Understanding your savings rate can help you identify areas for improvement. If you’re aiming for a 15% savings rate but are only saving 5%, you know you have room to increase your contributions. It can also help you see how changes in your income or expenses impact your savings. Remember, every little bit counts when it comes to retirement savings.

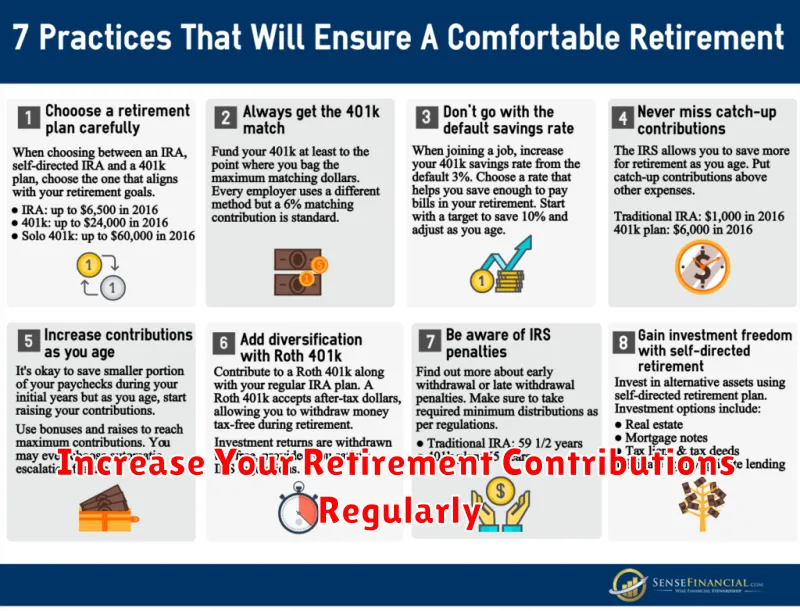

Increase Your Retirement Contributions Regularly

One of the most effective ways to boost your retirement savings is to increase your contributions regularly. Even small increases can make a significant difference over time, thanks to the power of compounding. Aim to increase your contributions by a small percentage each year, such as 1% or 2%. This gradual increase can be easily incorporated into your budget without feeling overwhelming.

Consider tying your contribution increases to pay raises or bonuses. This way, you’re essentially putting your extra income into your retirement savings, making it a natural part of your financial plan.

A simple rule of thumb is to aim for a contribution level of 15% of your gross income. This may seem like a large number, but it’s a common benchmark for achieving financial independence in retirement. However, if 15% seems out of reach, start with a smaller percentage and gradually increase it over time.

Catch-Up Contributions for Those 50+

If you’re 50 or older, you have a powerful tool at your disposal to supercharge your retirement savings: catch-up contributions. These allow you to contribute extra money to your retirement accounts each year, helping you make up for lost time and get closer to your financial goals.

Here’s how catch-up contributions work: The IRS lets you contribute an additional amount on top of the regular annual contribution limits for both traditional and Roth IRAs, as well as 401(k) and 403(b) plans. In 2023, you can contribute an extra $1,000 to your IRA and $7,500 to your 401(k). This can significantly boost your retirement savings, especially if you’ve been saving for a while.

Catch-up contributions are a great way to take advantage of the “compound interest effect” – even small increases in contributions can snowball over time, making a significant difference in your retirement nest egg. If you’re looking to make the most of your savings years, catch-up contributions are a must.

Explore Tax-Advantaged Retirement Accounts

One of the most effective ways to boost your retirement savings is to take advantage of tax-advantaged retirement accounts. These accounts offer significant tax benefits that can help you save more money over the long term. There are several different types of tax-advantaged retirement accounts available, each with its own unique set of rules and benefits.

Traditional IRAs allow you to deduct your contributions from your taxable income, reducing your tax liability in the present. However, you’ll be taxed on withdrawals in retirement. Roth IRAs work in reverse, with contributions made after taxes but withdrawals in retirement being tax-free. The best option for you depends on your individual financial situation and tax bracket.

401(k) plans are employer-sponsored retirement accounts. Your contributions may be deducted from your taxable income, and your employer may also offer a matching contribution. 403(b) plans are similar to 401(k) plans but are offered to employees of certain non-profit organizations.

529 plans are designed specifically for saving for education expenses. While not technically retirement accounts, they offer significant tax advantages for saving for your children’s future. The benefits can vary based on your state of residence, so be sure to research the specific plan details in your area.

By understanding the different types of tax-advantaged retirement accounts available, you can make informed decisions about how to save for your future and potentially maximize your tax savings along the way. It’s essential to do your research and choose the plan that best suits your individual needs and financial goals.

Reduce Unnecessary Expenses

Cutting back on unnecessary expenses is a fundamental step in bolstering your retirement savings. By identifying areas where you can trim your spending, you’ll free up more money to invest for your future. This might involve reevaluating your subscriptions, dining out habits, or even reconsidering your transportation needs.

Start by tracking your spending for a few months. This will give you a clear picture of where your money is going. Look for recurring costs that can be eliminated or reduced. For example, can you downgrade your cable package or switch to a cheaper phone plan?

Another way to reduce unnecessary expenses is to cook more meals at home instead of eating out. Not only is this healthier, but it can save you a significant amount of money over time. Similarly, consider taking advantage of free or low-cost entertainment options, such as visiting parks, museums, or attending community events.

By adopting a more mindful approach to your spending habits, you can significantly increase your retirement savings. Every dollar you save today is a dollar that can grow in your retirement portfolio, giving you more financial freedom in your golden years.

Generate Additional Income Streams

Generating additional income streams is a vital strategy for bolstering your retirement savings. It allows you to supplement your regular income and accelerate your retirement planning. There are numerous avenues to explore, each with its unique advantages and considerations.

Part-time work offers flexibility and a consistent income stream. You can leverage your existing skills or explore new opportunities in areas that pique your interest. Freelancing provides the freedom to set your own hours and choose projects aligned with your abilities. Platforms like Upwork and Fiverr connect freelancers with clients seeking various services.

Renting out a spare room can generate passive income and provide a stable source of revenue. If you have a property or space you’re not fully utilizing, consider listing it on platforms like Airbnb or VRBO. Investing in real estate can yield significant returns, but it requires careful research and financial planning. Rental properties, commercial real estate, and even REITs offer potential investment avenues.

Starting a side hustle allows you to pursue a passion or explore entrepreneurial ventures. From selling handmade crafts to offering online courses, the options are abundant. Dividend stocks provide a regular stream of income, while high-yield savings accounts offer competitive interest rates on your deposits.

Remember to assess your time commitment, financial resources, and risk tolerance when exploring additional income streams. Carefully research and evaluate each option before making a decision. By diversifying your income sources, you can enhance your financial security and accelerate your journey towards a comfortable retirement.

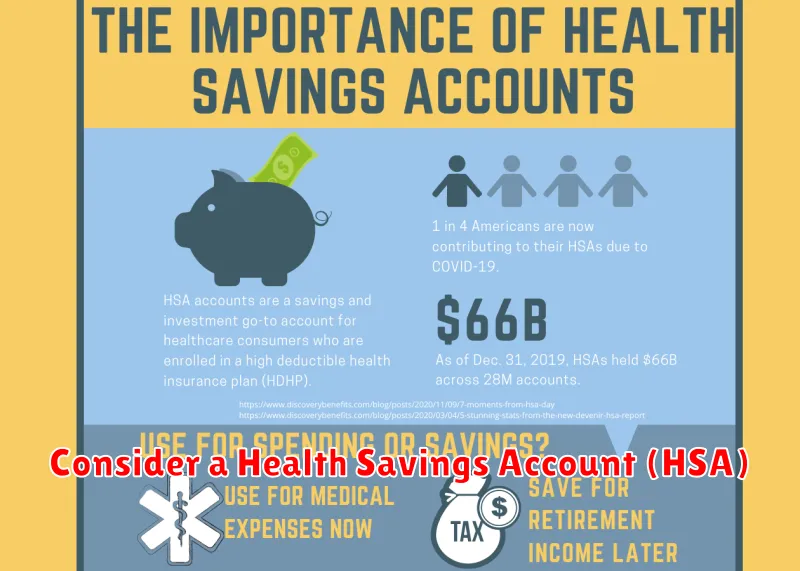

Consider a Health Savings Account (HSA)

A Health Savings Account (HSA) is a tax-advantaged savings account that can be used for healthcare expenses. It can be a powerful tool for boosting your retirement savings, as it offers a triple tax advantage: contributions are tax-deductible, earnings grow tax-deferred, and withdrawals for qualified medical expenses are tax-free.

Here’s how it works: You can contribute pre-tax dollars to an HSA, reducing your taxable income. This money can then be used to pay for medical expenses, such as doctor’s visits, prescriptions, and deductibles. If you have leftover money in your HSA at the end of the year, it can be invested and grow tax-deferred. In retirement, you can use the funds for any purpose, though withdrawals for non-medical expenses will be taxed.

To be eligible for an HSA, you must be enrolled in a high-deductible health plan (HDHP). HSAs are a great option for those who are healthy and expect to use minimal healthcare services, as you are responsible for paying for your medical expenses until you reach your deductible.

Here are some benefits of using an HSA for retirement savings:

- Tax Savings: HSAs offer significant tax advantages, allowing you to save more for retirement.

- Investment Growth: HSA funds can be invested, allowing them to grow tax-deferred.

- Flexibility: You can use the funds for any purpose in retirement, though withdrawals for non-medical expenses will be taxed.

If you are eligible for an HSA, consider it a powerful tool for boosting your retirement savings. The tax advantages and flexibility make it a smart choice for individuals looking to build a secure financial future.

Make Smart Investment Choices

Saving for retirement is a marathon, not a sprint. You need a long-term plan that takes into account market fluctuations and your own risk tolerance. This means making smart investment choices that will help your money grow over time.

A good rule of thumb is to diversify your portfolio, meaning you don’t put all your eggs in one basket. Instead, you spread your investments across different asset classes, such as stocks, bonds, and real estate. This helps to reduce risk and potentially increase your returns.

It’s also important to consider your investment timeframe. If you’re planning to retire in 20 years, you can afford to take on more risk than someone who is retiring in five years. Younger investors can typically afford to hold more stocks, which have the potential for higher growth over the long term. As you get closer to retirement, you may want to shift more of your portfolio to bonds, which are generally considered safer.

Finally, don’t forget to rebalance your portfolio regularly. Over time, some investments will perform better than others. Rebalancing helps to ensure that your portfolio stays aligned with your original investment strategy and risk tolerance.

By following these tips, you can make smart investment choices that will help you reach your retirement goals.

Reassess Your Risk Tolerance

Your risk tolerance, or how comfortable you are with the potential for losses in your investments, is a crucial factor in determining the best way to boost your retirement savings. As you approach retirement, it’s essential to reassess your risk tolerance and make adjustments to your investment portfolio accordingly.

If you’re younger and have a longer time horizon, you can generally afford to take on more risk. However, as you get closer to retirement, you’ll likely want to reduce your exposure to risk. This is because you have less time to recover from potential losses.

There are a few ways to adjust your risk tolerance for retirement:

- Shift your investment mix: Consider moving some of your money from stocks, which are considered riskier, to bonds, which are generally considered safer.

- Diversify your portfolio: By investing in a variety of assets, you can reduce the overall risk of your portfolio.

- Consider a guaranteed income stream: Annuities can provide a guaranteed income stream in retirement, which can help to reduce your risk.

It’s important to note that there’s no one-size-fits-all approach to risk tolerance. What’s right for one person may not be right for another. It’s best to consult with a financial advisor to determine the best approach for your individual circumstances.

Diversify Your Investment Portfolio

One of the best ways to boost your retirement savings is to diversify your investment portfolio. This means investing in a variety of different asset classes, such as stocks, bonds, real estate, and commodities. By spreading your money across different asset classes, you can reduce your risk and potentially increase your returns.

Here are some of the benefits of diversifying your investment portfolio:

- Reduced risk: When you invest in a variety of asset classes, you are less likely to be heavily impacted by a downturn in any one market. For example, if the stock market takes a dip, your bond investments may still be doing well.

- Increased potential returns: By investing in a variety of assets, you can take advantage of different market opportunities. For example, if the real estate market is strong, you could see good returns on your real estate investments.

- Improved long-term performance: Over time, a diversified portfolio is more likely to outperform a portfolio that is heavily concentrated in one or two asset classes.

Here are some tips for diversifying your investment portfolio:

- Start with a mix of stocks and bonds. Stocks offer the potential for higher returns, but they are also riskier than bonds. Bonds are generally considered a safer investment, but they offer lower returns.

- Consider adding real estate to your portfolio. Real estate can be a good hedge against inflation and can provide a stream of rental income.

- Don’t be afraid to invest in commodities. Commodities, such as gold and oil, can provide diversification and protection against inflation.

- Rebalance your portfolio regularly. As your investments grow, you’ll need to rebalance your portfolio to maintain your desired asset allocation.

Diversifying your investment portfolio is an important step in securing your financial future. By spreading your risk across different asset classes, you can increase your potential for returns and build a stronger foundation for retirement.

Rebalance Your Portfolio Periodically

Rebalancing your portfolio regularly is crucial for maximizing your retirement savings. It helps you maintain a desired asset allocation and avoid excessive risk or underperformance.

As your investments grow, certain asset classes may become overweighted, leading to a potential imbalance. By rebalancing, you sell some of the overperforming assets and reinvest in the underperforming ones, bringing your portfolio back to your target allocation.

Rebalancing helps you stay disciplined and avoids emotional investing. It prevents you from holding onto underperforming investments for too long or chasing after hot investments. Regular rebalancing ensures you are always aligned with your long-term financial goals and risk tolerance.

There is no one-size-fits-all approach to rebalancing. The frequency depends on your individual needs and market volatility. However, a good rule of thumb is to rebalance your portfolio at least once a year, or more often if your asset allocation deviates significantly from your target.

By rebalancing your portfolio periodically, you can keep your investments on track, reduce risk, and maximize your potential returns.

Seek Professional Financial Advice

While you can learn a lot about retirement planning online or through books, it’s highly recommended to seek the advice of a professional financial advisor. They can provide personalized guidance based on your individual circumstances, such as your income, expenses, risk tolerance, and retirement goals.

A financial advisor can help you:

- Develop a comprehensive retirement plan

- Determine the right asset allocation for your portfolio

- Choose the best investment options for your needs

- Identify potential tax savings strategies

- Monitor your progress and make adjustments as needed

They can also help you navigate complex financial matters like Social Security benefits, Medicare, and long-term care planning.

Remember, seeking professional advice is an investment in your future. By working with a trusted advisor, you can increase your chances of achieving a comfortable and secure retirement.

{kind=link}