Are you looking to invest your money but unsure where to start? It can be overwhelming to navigate the world of stocks, bonds, and mutual funds. These three investment options offer different levels of risk, return potential, and liquidity. Understanding the key differences between them is crucial for building a well-rounded investment portfolio tailored to your individual financial goals. This guide will explore the fundamental characteristics of each asset class, helping you make informed decisions for your investment journey.

Whether you’re a seasoned investor or just starting, grasping the nuances of stocks, bonds, and mutual funds is vital. This article will break down the pros and cons, risk profiles, and potential returns associated with each investment type. By understanding the differences, you can create an investment strategy that aligns with your risk tolerance, time horizon, and financial objectives. So, buckle up and join us as we delve into the exciting world of investment options!

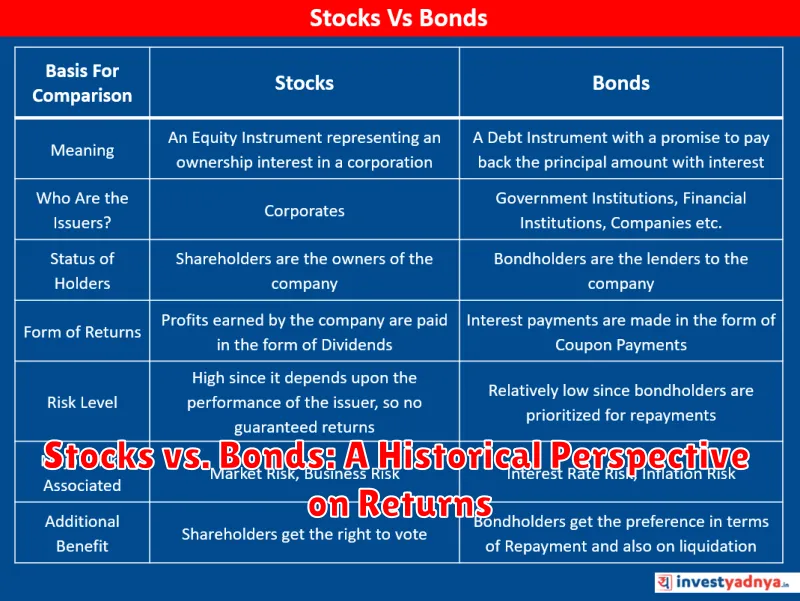

Stocks: Ownership, Growth Potential, and Volatility

Stocks represent ownership in a company. When you buy stock, you’re purchasing a small piece of that company’s equity. This ownership entitles you to a share of the company’s profits and any potential future growth.

Stocks have the potential for significant growth. If a company performs well, the value of its stock can rise substantially, generating high returns for investors. However, stocks also carry volatility, meaning their prices can fluctuate widely in the short term. This volatility can lead to potential losses, especially during periods of economic uncertainty or industry downturns.

There are two main types of stocks:

- Common stock gives investors voting rights and the right to receive dividends, which are payments distributed from the company’s profits.

- Preferred stock offers investors a fixed dividend payment, but they typically don’t have voting rights.

Investing in stocks can be a rewarding strategy for long-term investors seeking to grow their wealth, but it’s crucial to understand the associated risks and be prepared for potential market fluctuations.

Bonds: Fixed Income, Stability, and Lower Risk

Bonds represent a debt investment, where you lend money to a company or government entity. In return, they promise to pay back the principal amount (your initial investment) along with interest payments at predetermined intervals. This structure makes bonds a more stable and predictable investment compared to stocks.

The primary appeal of bonds lies in their fixed income. You know precisely how much interest you’ll earn on your investment. This predictability makes them a suitable option for investors seeking income generation, particularly those who prioritize stability over potentially higher returns.

Bonds typically offer a lower risk profile than stocks. While they can still fluctuate in value, their stability is rooted in the guaranteed principal repayment. However, it’s crucial to understand that bonds are not risk-free. Factors like inflation, interest rate hikes, and the issuer’s creditworthiness can influence bond values.

There are various types of bonds, each with its own characteristics. Government bonds (issued by national governments) are generally considered less risky than corporate bonds (issued by companies). The interest rate and maturity date of a bond also impact its risk and return potential.

Bonds can be a valuable component of a diversified investment portfolio. They offer stability, income, and a lower risk profile compared to stocks. However, like any investment, it’s crucial to conduct thorough research and understand the intricacies of bond investing before making any decisions.

Mutual Funds: Diversification, Professional Management, and Flexibility

Mutual funds offer a compelling investment option due to their unique combination of diversification, professional management, and flexibility. By pooling funds from numerous investors, mutual funds enable diversification across various asset classes, reducing overall risk. This diversification is crucial for investors seeking to mitigate the volatility inherent in individual stocks or bonds.

Furthermore, mutual funds benefit from the expertise of professional portfolio managers. These managers, armed with specialized knowledge and market insights, meticulously select and manage the assets within the fund. This professional oversight minimizes the burden on individual investors, allowing them to leverage the experience of experts without the need for extensive research and trading.

The flexibility offered by mutual funds is another key advantage. Investors can choose from a wide range of funds targeting different asset classes, investment styles, and risk tolerances. This array of options empowers investors to align their investments with their financial goals and risk appetites. Moreover, mutual funds allow for easy entry and exit, offering investors the freedom to adjust their portfolio as needed.

Understanding Risk and Return in Each Asset Class

When it comes to investing, understanding the relationship between risk and return is crucial. Risk refers to the potential for losing money on an investment, while return refers to the potential for making money. Generally, the higher the risk, the higher the potential return. This relationship applies across all asset classes, including stocks, bonds, and mutual funds.

Stocks are considered a higher-risk investment than bonds. This is because stocks represent ownership in a company, and the value of a stock can fluctuate significantly based on the company’s performance. However, stocks also have the potential for higher returns than bonds. Historically, stocks have outperformed bonds over the long term.

Bonds, on the other hand, are considered a lower-risk investment than stocks. This is because bonds represent loans to a company or government, and the interest payments are fixed. While bonds offer less potential for growth than stocks, they are generally considered a safer investment.

Mutual funds are baskets of stocks, bonds, or other assets that are managed by a professional fund manager. Mutual funds offer diversification, which means that your investment is spread across multiple assets. This diversification helps to reduce risk. The risk and return of a mutual fund will depend on the underlying assets it invests in. A fund that invests in stocks will generally be considered riskier than a fund that invests in bonds.

It’s important to remember that there is no one-size-fits-all approach to investing. The best asset class for you will depend on your individual risk tolerance, investment goals, and time horizon. It’s essential to carefully consider your financial situation and seek advice from a qualified financial advisor before making any investment decisions.

Stocks vs. Bonds: A Historical Perspective on Returns

When it comes to investing, two prominent asset classes stand out: stocks and bonds. While both offer the potential for growth, they differ significantly in their risk profiles, returns, and suitability for different investment goals. Understanding the historical performance of these asset classes can provide valuable insights into their potential for future returns.

Historically, stocks have outperformed bonds over the long term. This is because stocks represent ownership in companies, allowing investors to participate in their growth and profitability. As companies grow and generate profits, their stock prices tend to rise, resulting in higher returns for investors. However, stocks are considered a riskier investment than bonds, as their values can fluctuate significantly in the short term due to factors like economic conditions, company performance, and market sentiment.

Bonds, on the other hand, are debt instruments that represent loans made to governments or corporations. Investors who buy bonds are essentially lending money to the issuer in exchange for periodic interest payments and the repayment of the principal amount at maturity. Bonds are generally considered less risky than stocks, as they offer a fixed rate of return and are less susceptible to market volatility. However, bonds typically provide lower returns compared to stocks over the long term.

The historical performance of stocks and bonds can be summarized as follows:

- Stocks have historically yielded higher returns than bonds, but they also come with higher risk.

- Bonds offer a more stable and predictable return, but their growth potential is limited compared to stocks.

It’s important to note that past performance is not necessarily indicative of future results. However, historical data provides a valuable benchmark for understanding the potential returns and risks associated with stocks and bonds. When making investment decisions, it’s crucial to consider your individual risk tolerance, investment goals, and time horizon.

Mutual Funds: Active vs. Passive Management Approaches

Mutual funds are a popular investment vehicle that allows investors to pool their money together to purchase a diversified portfolio of securities, such as stocks or bonds. When choosing a mutual fund, one important decision is whether to opt for an actively managed or a passively managed fund.

Active management involves a fund manager who actively buys and sells securities within the fund’s portfolio with the goal of outperforming the market. These managers try to identify undervalued investments and capitalize on market trends. Active management typically involves higher fees due to the expertise and time required to manage the fund.

Passive management, on the other hand, aims to track a specific market index, such as the S&P 500. Passive funds, also known as index funds, typically have low management fees and a low turnover rate. These funds buy and hold securities in the same proportion as the index they are tracking, mimicking its performance.

The choice between active and passive management depends on various factors, including investment goals, risk tolerance, and time horizon. Active management may be suitable for investors who are seeking to outperform the market and are willing to pay higher fees for a fund manager’s expertise. Passive management may be a more cost-effective option for investors who prefer a low-cost, hands-off approach to investing.

The Role of Each Asset Class in a Diversified Portfolio

A diversified portfolio is a collection of different asset classes that are designed to reduce risk and potentially enhance returns. The most common asset classes include stocks, bonds, and real estate. Each asset class has its own unique characteristics and risks, and understanding these differences is essential for building a well-diversified portfolio.

Stocks represent ownership in publicly traded companies. They are considered a growth asset, meaning they have the potential to generate higher returns over time. However, stocks also carry higher risk than bonds, as their value can fluctuate significantly based on factors such as company performance, economic conditions, and investor sentiment.

Bonds, on the other hand, represent loans made to companies or governments. They are considered a conservative asset, as they generally offer lower returns but are also less volatile than stocks. Bonds can provide stability and income to a portfolio, especially during times of economic uncertainty.

Real estate can be a good source of diversification, providing potential for both income and appreciation. However, it can be illiquid and require significant capital outlay.

The specific allocation of assets within a portfolio will depend on individual circumstances, risk tolerance, and investment goals. It’s important to consult with a financial advisor to create a portfolio that is tailored to your needs.

Factors to Consider When Choosing Between Stocks, Bonds, and Mutual Funds

When it comes to investing, understanding the differences between stocks, bonds, and mutual funds is crucial. Each investment vehicle carries its own set of characteristics and risks, and making the right choice depends on your individual financial goals, risk tolerance, and time horizon. Here are some key factors to consider:

Risk Tolerance: Stocks generally offer higher potential returns but also carry greater risk. Bonds are considered less risky, with lower returns. Mutual funds diversify your portfolio across various assets, mitigating risk but offering varying levels of potential return based on the underlying investments.

Time Horizon: Stocks are better suited for long-term investments, as they can ride out market fluctuations and potentially generate significant returns over time. Bonds are a good choice for short to medium-term investments, providing a steady income stream and relative stability. Mutual funds offer flexibility, allowing you to invest for different time horizons depending on the specific fund.

Investment Goals: Your financial goals will influence your investment choices. Stocks are often used for growth and wealth accumulation, while bonds are suitable for generating income and preserving capital. Mutual funds can serve various goals, from retirement planning to specific thematic investments.

Investment Expertise and Time Commitment: Stocks and bonds often require more individual research and active management. Mutual funds provide professional management, simplifying the investment process and freeing up your time. However, it’s important to choose a fund that aligns with your investment goals and risk tolerance.

Fees and Expenses: Stocks and bonds typically involve lower fees compared to mutual funds, which charge management fees and expenses. However, mutual funds can offer access to expertise and diversification that might not be readily available to individual investors.

Investment Time Horizon and Its Influence on Asset Allocation

Your investment time horizon, or the length of time you plan to stay invested, is a crucial factor in determining your asset allocation. This is the mix of different asset classes, like stocks, bonds, and real estate, that make up your portfolio. The longer your investment horizon, the more risk you can typically take on.

For example, if you’re saving for retirement decades from now, you have more time to recover from market downturns. You can afford to allocate a larger portion of your portfolio to stocks, which historically have generated higher returns over the long term but also carry more volatility.

On the other hand, if you’re saving for a short-term goal, like a down payment on a house in a few years, you’ll want to take on less risk. This means allocating a larger portion of your portfolio to bonds, which are generally considered safer than stocks but offer lower returns.

Here’s a simple breakdown:

- Short-term horizon (less than 5 years): Higher allocation to bonds and cash.

- Mid-term horizon (5-10 years): Balanced portfolio with a mix of stocks and bonds.

- Long-term horizon (10+ years): Higher allocation to stocks.

It’s important to note that these are just general guidelines. The best asset allocation for you will depend on your individual circumstances, risk tolerance, and financial goals. If you’re unsure how to determine your investment time horizon and asset allocation, it’s always a good idea to consult with a financial advisor.

Liquidity and Accessibility of Stocks, Bonds, and Mutual Funds

When it comes to investing, liquidity and accessibility are crucial factors to consider. They determine how easily you can convert your investments into cash when you need it. Let’s explore the liquidity and accessibility of stocks, bonds, and mutual funds:

Stocks are generally considered more liquid than bonds or mutual funds. You can typically buy and sell stocks on major stock exchanges like the New York Stock Exchange (NYSE) or NASDAQ, which are open for trading during business hours. However, the liquidity of individual stocks can vary depending on factors such as the company’s size, trading volume, and overall market conditions.

Bonds are typically less liquid than stocks. While some bonds are traded on exchanges, many are traded over-the-counter (OTC). This means they’re bought and sold directly between investors, which can take longer and involve more negotiation. The liquidity of a specific bond can also depend on its maturity date, credit rating, and market interest rates.

Mutual funds offer a level of liquidity that falls somewhere between stocks and bonds. You can typically buy and sell mutual fund shares through your brokerage account, which is generally a more straightforward process than trading bonds. However, mutual funds often have minimum investment requirements and may impose redemption fees, which can impact your ability to access your funds quickly.

Ultimately, the liquidity and accessibility of any investment depend on several factors, including the specific investment, the market conditions, and your brokerage account. It’s important to understand these factors before making investment decisions.

Fees and Expenses Associated with Each Investment Option

Investing in stocks, bonds, and mutual funds comes with associated fees and expenses, which can vary greatly depending on the specific investment and the broker or investment platform you choose. Understanding these costs is crucial for making informed investment decisions and maximizing returns.

Stocks typically involve brokerage fees when buying and selling shares. These fees can vary based on the brokerage you choose and the type of trade (e.g., online vs. phone). Some brokers may offer commission-free trades, while others may charge flat fees or a percentage of the trade value.

Bonds, like stocks, involve brokerage fees when buying and selling. However, bonds may also carry other fees such as those related to the issuance of the bond, which are reflected in the bond’s yield.

Mutual funds typically have expense ratios, which are annual fees that cover the costs of managing the fund. These expense ratios are expressed as a percentage of the fund’s assets. Mutual funds may also have additional fees, such as redemption fees, which are charged when you sell shares.

It’s important to consider all fees and expenses when choosing an investment option. Be sure to read the prospectus or fund documents carefully before making any investment decisions.

Tax Implications of Stocks, Bonds, and Mutual Funds

Understanding the tax implications of different investment types is crucial for maximizing your returns. Stocks, bonds, and mutual funds each have their own unique tax characteristics that investors should be aware of. Let’s explore the tax aspects of these common investment vehicles.

Stocks: When you sell stocks, you will be subject to capital gains tax. This tax is calculated based on the difference between the selling price and the purchase price, known as your capital gain. Capital gains are typically taxed at preferential rates compared to ordinary income.

Bonds: Interest earned from bonds is considered taxable income. The interest payments you receive are typically subject to federal, state, and local taxes. However, some municipal bonds are exempt from federal income tax, making them attractive to investors seeking to reduce their tax liability.

Mutual Funds: Mutual funds can have a more complex tax structure. Depending on the type of mutual fund, you may receive distributions of capital gains or dividends, which are taxable. Additionally, if you sell shares of a mutual fund, you will be subject to capital gains tax based on the difference between the purchase price and the selling price. You may also need to pay capital gains tax on any distributions you received while holding the fund.

Seeking Professional Advice for Investment Decisions

While understanding the basics of stocks, bonds, and mutual funds is crucial for informed investment decisions, seeking professional advice from a qualified financial advisor can provide significant benefits. These advisors can offer valuable insights, tailored strategies, and a comprehensive perspective based on their expertise and experience. Here’s why professional advice can make a difference:

Personalized Investment Plan: A financial advisor will work with you to understand your financial goals, risk tolerance, and time horizon. They can then create a customized investment plan that aligns with your specific needs and circumstances. This personalized approach ensures that your investments are strategically allocated to maximize returns while minimizing risk.

Objective Guidance: When making investment decisions, it’s easy to get caught up in emotions or be influenced by market trends. A financial advisor provides objective guidance, helping you stay focused on your long-term goals and avoid impulsive decisions. They can offer a balanced perspective and help you make rational choices based on sound financial principles.

Market Expertise: Financial advisors have extensive knowledge of the market, including current trends, economic conditions, and industry analysis. They can leverage this expertise to identify investment opportunities and potential risks, helping you make informed decisions. This specialized knowledge can be particularly valuable during market fluctuations or periods of uncertainty.

Ongoing Support: Investing is not a one-time event but an ongoing process. A financial advisor provides ongoing support and guidance throughout your investment journey. They can monitor your portfolio, adjust strategies as needed, and provide regular updates on market performance. Their continued involvement helps ensure that your investments remain aligned with your evolving goals and financial situation.

Seeking professional advice from a qualified financial advisor is a wise decision for investors of all levels. Their expertise, objectivity, and ongoing support can help you make informed investment choices, maximize your returns, and achieve your financial goals.

{kind=link}