Navigating the world of finance can be daunting, especially in your 20s. This is a time when you’re likely just starting out in your career, building your independence, and exploring your financial goals. While it’s exciting, it can also be a period rife with potential financial pitfalls. Making smart money choices in your 20s sets you up for a secure financial future, but it’s easy to fall into common traps that can hinder your progress.

From overspending to neglecting savings, there are a number of financial mistakes that can have long-term repercussions. Understanding and avoiding these pitfalls is crucial for building a solid financial foundation. This article will delve into some of the most common financial mistakes people make in their 20s and offer actionable strategies to help you navigate your finances with confidence.

Living Beyond Your Means: The Budget Buster

Your 20s are a time of exciting new beginnings. You’re entering the workforce, building your career, and perhaps even starting a family. However, this period is also rife with financial pitfalls that can set you back for years to come. One of the most common mistakes young adults make is living beyond their means. This happens when you spend more money than you earn, often by succumbing to the allure of a lavish lifestyle.

It’s easy to fall into this trap when you see friends and colleagues living a lifestyle you admire. You might feel pressured to keep up, leading you to overspend on things like dining out, expensive vacations, and unnecessary gadgets. This can leave you with a mountain of debt, jeopardizing your financial future and hindering your ability to achieve your long-term goals.

To avoid living beyond your means, start by creating a realistic budget. This involves tracking your income and expenses, identifying areas where you can cut back, and setting financial goals. Make a conscious effort to prioritize your needs over your wants and resist the temptation to buy things you can’t afford. Remember, true wealth is not defined by what you own, but by what you can afford to keep.

Don’t let your 20s be defined by financial mistakes. By learning to manage your money wisely and living within your means, you can set yourself up for a bright and prosperous future.

Racking Up Credit Card Debt: A High-Interest Trap

In your 20s, you’re likely starting to build your credit history. While credit cards can be useful tools for building credit and making purchases, they can also become a major source of financial stress if you’re not careful. Credit card debt can easily spiral out of control due to high-interest rates. This trap can seriously impact your financial health and make it difficult to achieve your financial goals.

To avoid falling into this trap, it’s essential to understand how credit cards work and practice responsible usage. Here are some key tips to keep in mind:

- Pay your balance in full each month. This is the best way to avoid interest charges and maintain a good credit score.

- Use a credit card as a tool, not a crutch. Only charge what you can afford to pay off each month. Avoid using your card for impulse purchases or to cover essential expenses.

- Be aware of the interest rate. Choose a card with a low APR and compare offers before settling on one. Higher interest rates mean you’ll pay more in the long run.

- Set a budget and track your spending. This will help you stay on top of your expenses and avoid overspending on your card.

- Consider using a credit card with a rewards program. These can offer perks like cash back or travel points, but only if you use the card responsibly and pay your balance in full each month.

Remember, managing your credit cards responsibly is crucial for your financial well-being. By following these tips, you can avoid the high-interest trap and build a solid financial foundation for your future.

Neglecting Savings: Start Building Your Future Today

Your 20s are a time of exploration and growth, both personally and financially. While it’s tempting to focus on immediate needs and desires, neglecting savings can have significant long-term consequences. Starting a savings habit early is crucial for achieving financial security and setting yourself up for a brighter future.

The earlier you begin saving, the more time your money has to grow through compounding. Even small contributions can accumulate over time, giving you a substantial head start towards your financial goals. Don’t underestimate the power of compound interest; it’s a potent tool for wealth building.

Building a strong savings foundation in your 20s offers numerous advantages, including:

- Financial stability: A savings buffer provides a safety net for unexpected expenses, such as medical emergencies or job loss. It offers peace of mind knowing you can handle life’s curveballs.

- Investment opportunities: Savings provide the capital needed to invest in assets like stocks, real estate, or businesses, potentially generating greater returns over time.

- Goal achievement: Whether it’s buying a home, starting a family, or traveling the world, having savings makes achieving your financial goals more attainable.

While starting a savings habit may seem daunting, it’s easier than you might think. Start by setting a small, achievable savings goal and gradually increase your contributions as your income grows. Utilize tools like automatic transfers to streamline the process, and consider setting up a separate savings account to keep your funds segregated.

Remember, the key is to start now. Don’t wait until you’re older and wish you had started saving sooner. By building a strong savings foundation in your 20s, you’re investing in your future well-being and setting yourself up for a life of financial freedom.

Ignoring Investment Opportunities: Time is on Your Side

Your 20s are a crucial time to build a strong financial foundation. One of the biggest mistakes young people make is ignoring investment opportunities. You might think you don’t have enough money to invest, or that you need to wait until you’re older and have more financial stability. But the truth is, the earlier you start investing, the more time your money has to grow.

The power of compounding works in your favor. Compounding is when your investment earnings generate even more earnings, creating a snowball effect. The longer you invest, the bigger that snowball gets.

Even small investments can make a big difference over time. Think of it as planting a seed that grows into a mighty tree. Start by taking advantage of retirement accounts like 401(k)s and Roth IRAs. Even if you can only contribute a small amount each month, it adds up over time.

Don’t let the fear of the stock market hold you back. The stock market has always recovered from downturns, and historical data shows long-term investments tend to be profitable. Remember, investing is a marathon, not a sprint. Focus on the long-term and don’t be afraid of short-term fluctuations.

Not Having an Emergency Fund: Be Prepared for the Unexpected

Life is full of surprises, and not all of them are pleasant. A sudden job loss, unexpected medical expenses, or even a car breakdown can throw your finances into chaos if you’re not prepared. This is why having an emergency fund is crucial, especially in your 20s when you’re likely still establishing your financial foundation.

An emergency fund acts as a safety net, allowing you to handle unexpected expenses without resorting to credit cards or dipping into your savings. Aim to save at least 3-6 months’ worth of living expenses. While it might seem daunting, even starting with a small amount and consistently adding to it will build a solid foundation for financial security.

Think about it: if you’re caught off guard by an unexpected expense, you won’t have to stress about making ends meet. Having an emergency fund provides peace of mind and the freedom to navigate life’s challenges without financial worry.

Overspending on Lifestyle Inflation: Keep Your Spending in Check

Your 20s are a time of exciting new experiences and personal growth, but it’s also a crucial time to establish healthy financial habits. One common mistake that can derail your progress is lifestyle inflation. This is the tendency to increase your spending as your income rises, often without considering the long-term impact on your financial goals.

Here’s how to avoid falling into the trap of lifestyle inflation:

- Track Your Spending: Use budgeting apps or spreadsheets to track where your money is going. This awareness can help you identify unnecessary expenses.

- Define Your Needs vs. Wants: Before you buy something, ask yourself if it’s a necessity or a want. Prioritize needs like rent, food, and utilities while being mindful of unnecessary wants.

- Set a Budget and Stick to It: Create a realistic budget that outlines your income and expenses. Allocate funds to specific categories and avoid overspending in any area.

- Delay Gratification: Instead of instant gratification, consider delaying purchases for a set period. This allows you to reflect on your needs and avoid impulse buying.

- Challenge Your Spending Habits: Actively question your spending patterns. Are you buying things you don’t use? Can you find cheaper alternatives? By being mindful, you can save money in the long run.

By staying vigilant about your spending habits and resisting the allure of lifestyle inflation, you can build a solid financial foundation in your 20s that will serve you well for years to come.

Failing to Plan for Retirement: Start Early, Retire Comfortably

One of the biggest financial mistakes you can make in your 20s is neglecting to plan for retirement. Many young adults think they have plenty of time to save, but the truth is that starting early gives you a huge advantage. The magic of compounding, where your earnings generate more earnings, works wonders over time. The earlier you start, the more your money will grow.

Even small, consistent contributions can add up to a significant nest egg over the years. Imagine investing just $100 per month starting at age 20. If you earn a modest 7% annual return, you’d have over $700,000 by age 65!

Don’t be fooled by the perceived “long time” until retirement. Starting early allows you to benefit from the power of time. Take advantage of employer-sponsored retirement plans, like 401(k)s, and consider individual retirement accounts (IRAs). Remember, the earlier you start, the more comfortable your retirement will be.

Not Taking Advantage of Employer Benefits: Maximize Your Compensation Package

Your salary isn’t the only part of your compensation. Many employers offer a variety of benefits that can significantly increase your overall financial well-being. These benefits are often overlooked, but they can be incredibly valuable, especially in your 20s. Taking advantage of these perks can save you money, improve your health, and even boost your future retirement savings.

Health Insurance: Health insurance is crucial, particularly in your 20s when you’re likely to be more susceptible to health issues. Employer-sponsored health insurance plans often offer affordable coverage and can help you avoid costly medical bills.

Retirement Savings Plans: Many companies offer 401(k) plans or similar retirement savings vehicles. These plans allow you to contribute pre-tax dollars to your retirement savings, potentially reducing your tax burden. Take advantage of employer matching programs, where they contribute a certain amount for every dollar you contribute, essentially giving you free money towards your future.

Paid Time Off: Don’t underestimate the value of vacation time. Not only can it reduce stress and boost your mental well-being, but it also gives you time to recharge and focus on your personal goals. Use it wisely.

Tuition Reimbursement: Some employers offer tuition reimbursement programs that can help you further your education and enhance your career prospects. This can lead to increased earning potential in the long run.

Flexible Spending Accounts (FSAs): FSAs allow you to set aside pre-tax dollars to cover eligible medical expenses and dependent care expenses. This can significantly reduce your tax liability and help you save money on these essential costs.

Employee Discounts: Many companies offer discounts on goods and services, including things like gym memberships, travel, and even entertainment. Don’t forget to take advantage of these perks to save money on things you already use.

By fully utilizing your employer benefits, you’re essentially maximizing your compensation package beyond just your salary. It’s a smart financial move that can have a significant impact on your financial well-being, both now and in the future.

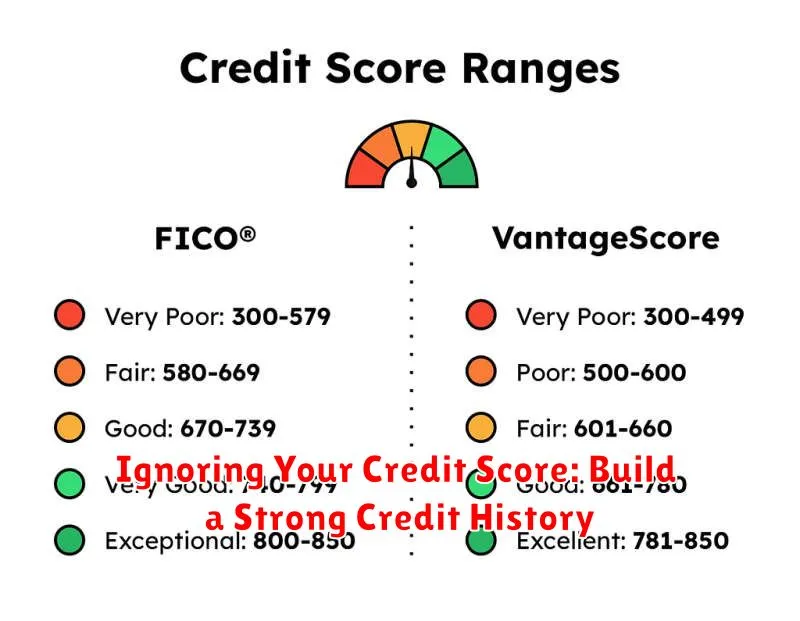

Ignoring Your Credit Score: Build a Strong Credit History

Your credit score is a crucial factor in your financial life. It plays a significant role in getting approved for loans, mortgages, credit cards, and even jobs. In your 20s, it’s essential to start building a strong credit history by understanding how your credit score works and taking steps to improve it.

Here are some tips to get you started:

- Get a credit card: A secured credit card is a great starting point. Secured cards require a security deposit, which limits the amount you can borrow. However, responsible use builds your credit history.

- Pay your bills on time: Payment history makes up a large percentage of your credit score. Set reminders or use automatic payments to avoid late payments.

- Keep your credit utilization low: Credit utilization ratio is the amount of credit you use compared to your available credit. Aim for less than 30% to maintain a healthy score.

- Monitor your credit report: Check your credit report regularly for errors and identify any fraudulent activity. You’re entitled to a free credit report from each of the three major credit bureaus annually.

- Avoid taking on too much debt: While building credit is important, avoid accumulating too much debt. Focus on paying down existing debt before taking on new loans or credit cards.

Building a strong credit history in your 20s sets you up for financial success later on. By taking these steps, you’ll ensure that you have access to affordable financing options for your future needs.

Not Seeking Financial Education: Empower Yourself with Knowledge

Your 20s are a crucial time for building a strong financial foundation. While it might seem overwhelming, taking control of your finances is not just about saving money – it’s about empowering yourself with knowledge. Understanding basic financial principles can set you up for success in the long run, helping you avoid costly mistakes that can derail your future goals.

Imagine starting your career with a solid financial plan. You’ll be able to confidently navigate challenges like student loan repayment, investing for retirement, or even making smart decisions about buying a home. Don’t underestimate the power of financial literacy. It’s an investment in yourself that pays off in countless ways.

Think of it this way: Would you drive a car without knowing how to operate it? Of course not! Your finances deserve the same level of attention. Instead of feeling intimidated, embrace the opportunity to learn. There are countless resources available, from online courses to personal finance books and websites. Take the time to educate yourself, and you’ll be amazed at how much easier managing your money becomes.

{kind=link}