Are you tired of constantly feeling broke, even though you work hard and earn a decent income? Maybe you’re overwhelmed by debt and just don’t know where your money is going. If this sounds familiar, you’re not alone. Many people struggle with their finances, but it doesn’t have to be this way. The key is to create a realistic monthly budget that works for you.

A budget is a plan for how you will spend your money each month. It’s not about restricting yourself or making sacrifices; it’s about taking control of your finances so you can achieve your financial goals. Whether you want to pay off debt, save for a down payment on a house, or just have more money to spend on the things you enjoy, a monthly budget is the first step towards financial freedom.

Track Your Income and Expenses

Before you can create a budget, you need to know where your money is going. This means tracking both your income and expenses.

Start by gathering all of your financial documents, including bank statements, credit card statements, and pay stubs. You can use a spreadsheet, budgeting app, or a simple notebook to record your income and expenses. Be sure to track everything, even small purchases like coffee or snacks.

Once you’ve gathered all your financial documents, you can start tracking your income and expenses. There are a few different ways to track your finances.

The 50/30/20 Rule is a common budgeting method that suggests allocating 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment.

The Zero-Based Budget is a method where you allocate every dollar of your income to a specific category. You’ll need to track your expenses carefully and ensure they all add up to your total income.

The Envelope Method is a physical way of budgeting where you allocate cash to specific categories and put the money in designated envelopes.

No matter which method you choose, the important thing is to be consistent with your tracking. Make sure you track everything so you can understand your spending patterns.

Identify Your Needs vs. Wants

Creating a realistic monthly budget is crucial for managing your finances effectively. The first step in this process is identifying the difference between your needs and wants. This distinction allows you to prioritize spending and make informed decisions about where your money goes.

Needs are essential for survival and well-being. They include items like rent or mortgage payments, groceries, utilities, transportation, and healthcare. These expenses are non-negotiable and must be accounted for in your budget.

Wants, on the other hand, are desires that enhance your lifestyle but aren’t necessary for survival. Examples include dining out, entertainment, shopping for clothes, vacations, and subscriptions. While these things can bring enjoyment, they’re often more flexible and can be adjusted or eliminated if necessary.

By clearly identifying your needs and wants, you gain control over your spending. You can allocate your funds strategically, ensuring that your essential needs are met before indulging in wants. This process fosters financial discipline and helps you achieve your financial goals more effectively.

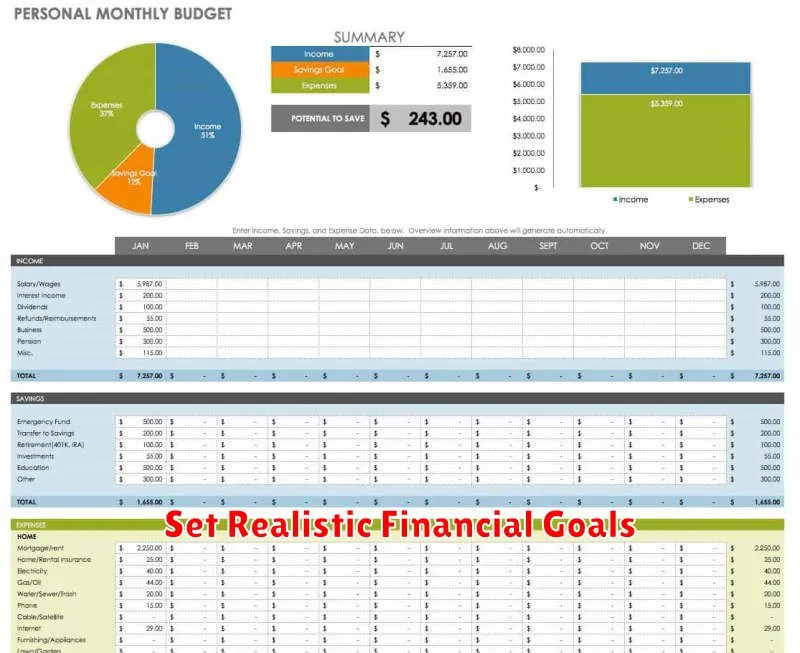

Set Realistic Financial Goals

Before you start budgeting, it’s crucial to set realistic financial goals. This means setting goals that are achievable within your current financial situation. Don’t be discouraged if your goals seem small at first. The key is to start with something manageable and build from there.

Here are some tips for setting realistic financial goals:

- Be specific: Instead of saying “I want to save more money,” set a specific goal, like “I want to save $500 per month.”

- Make them measurable: How will you know if you’ve reached your goal? It’s helpful to track your progress.

- Set a timeline: When do you want to achieve your goal? Having a deadline will help keep you motivated.

- Break it down: Don’t try to do everything at once. Divide your goals into smaller, more manageable steps.

- Prioritize: Not all goals are created equal. Identify the most important ones and focus your efforts on those first.

Setting realistic financial goals is a crucial step in creating a successful budget. By setting achievable goals, you can stay motivated and make progress towards your financial objectives.

Allocate Your Income to Different Categories

Once you have a clear picture of your income and expenses, it’s time to allocate your income to different categories. This step is crucial for creating a realistic budget that you can stick to. Start by grouping your expenses into essential needs, wants, and savings.

Essential needs include expenses that are absolutely necessary for survival, such as housing, food, transportation, and utilities. Allocate a portion of your income to cover these needs, ensuring you have enough to meet your basic requirements.

Wants are expenses that are not essential but provide you with enjoyment or convenience. This category might include dining out, entertainment, shopping, and subscriptions. While wants are important for overall well-being, try to allocate a reasonable amount to this category, leaving room for savings and other financial priorities.

Savings are crucial for financial security and future goals. Allocate a specific amount of your income to savings each month. This can include emergency funds, retirement savings, or funds for specific goals like a down payment on a house or a vacation.

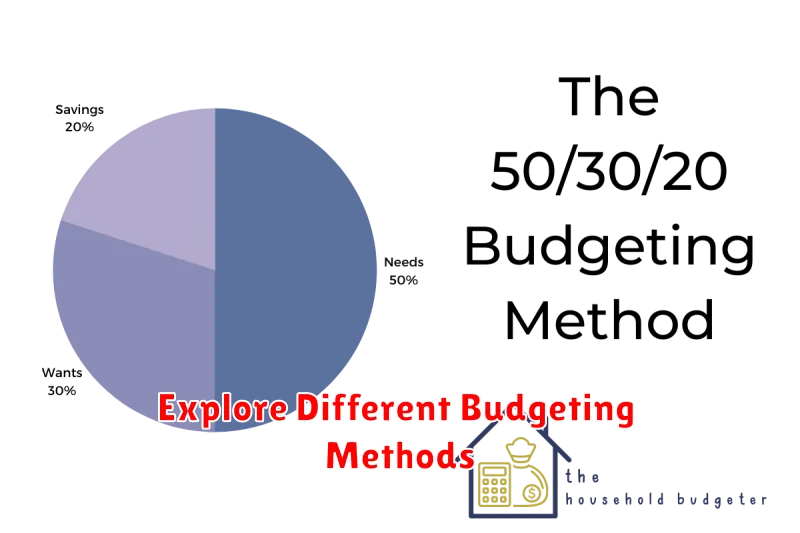

Explore Different Budgeting Methods

There are many different budgeting methods out there, but the most important thing is to find one that works for you. Some popular methods include:

Zero-Based Budgeting

This method involves allocating every dollar of your income to a specific category, leaving zero dollars left over. This can be a good way to ensure you are spending within your means and saving for your goals.

50/30/20 Budget

The 50/30/20 method breaks down your income into three categories: 50% for needs (like housing, groceries, utilities), 30% for wants (like entertainment, dining out, travel), and 20% for savings and debt repayment. This method can help you prioritize your spending and ensure you are putting money aside for your future.

Envelope Budgeting

The envelope method involves allocating cash to different spending categories and placing it in separate envelopes. This method can help you visualize your spending and make it more difficult to overspend in any particular category.

Cash-Flow Forecasting

This method involves tracking your income and expenses over a period of time to create a projection of your future cash flow. It can be a helpful way to identify potential areas for improvement and make informed decisions about your spending.

Ultimately, the best budgeting method for you will depend on your individual circumstances, goals, and spending habits. Experiment with different methods until you find one that works for you and helps you reach your financial goals.

Utilize Budgeting Apps and Tools

In today’s digital age, there are numerous budgeting apps and tools available to make managing your finances a breeze. These resources can help you track your spending, set financial goals, and automate your savings.

Some popular budgeting apps include Mint, Personal Capital, and YNAB (You Need a Budget). These apps allow you to connect your bank accounts, credit cards, and other financial accounts to provide a comprehensive overview of your finances. They can categorize your spending, create budgets, and send you alerts when you’re approaching your spending limits.

Beyond budgeting apps, there are also budgeting spreadsheets and online calculators available. These tools can be helpful for those who prefer a more hands-on approach to budgeting or who want to customize their budgeting system.

By leveraging budgeting apps and tools, you can streamline your budgeting process, gain valuable insights into your spending habits, and ultimately take control of your finances.

Build an Emergency Fund

An emergency fund is a crucial part of any realistic budget. It acts as a safety net to cover unexpected expenses, such as medical bills, car repairs, or job loss. Without an emergency fund, you could find yourself in a difficult financial situation, forced to rely on credit cards or loans to cover unexpected costs.

The general recommendation is to have three to six months’ worth of living expenses saved in an emergency fund. This amount should cover your essential needs, including rent or mortgage, utilities, groceries, transportation, and any recurring debt payments.

Here are some tips for building an emergency fund:

- Set a realistic savings goal: Start with a smaller goal, such as saving $500 or $1,000, and gradually increase it as you become more comfortable.

- Automate your savings: Set up automatic transfers from your checking account to your savings account each month. This will make saving a habit and prevent you from having to manually transfer funds.

- Find ways to cut expenses: Look for areas where you can reduce your spending, such as eating out less, cutting back on entertainment, or negotiating lower bills.

- Consider side hustles: If you need to boost your savings faster, consider taking on a part-time job or starting a side hustle to generate extra income.

Building an emergency fund may seem daunting at first, but even saving a small amount each month can make a significant difference in the long run. Remember, it’s about creating a safety net for your financial well-being, providing peace of mind and reducing stress in the face of unexpected life events.

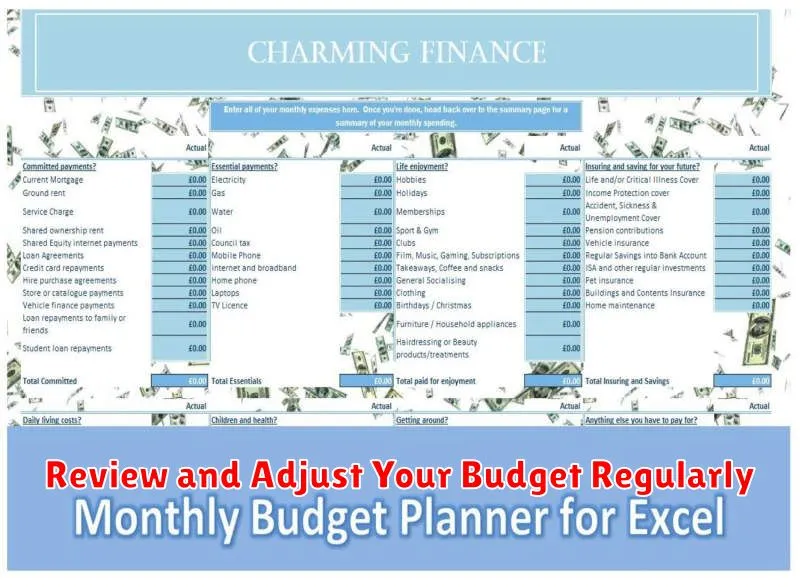

Review and Adjust Your Budget Regularly

Creating a budget is a great first step, but it’s not a set-it-and-forget-it process. Life is constantly changing, and your budget should adapt with it. Review your budget at least once a month, or even more frequently if there are significant changes in your income or expenses. This could include a raise, a job change, a new car payment, or even a change in your spending habits.

As you review your budget, ask yourself these questions:

- Are you sticking to your spending limits?

- Are there areas where you can cut back?

- Are there any unexpected expenses that you need to account for?

- Have your financial goals changed?

Don’t be afraid to make adjustments to your budget as needed. The goal is to create a budget that works for you and your financial situation. You may need to adjust your budget frequently in the beginning as you learn your spending habits. But once you have a solid understanding of your finances, you can likely maintain a budget for longer periods.

By regularly reviewing and adjusting your budget, you can ensure that you are on track to reach your financial goals.

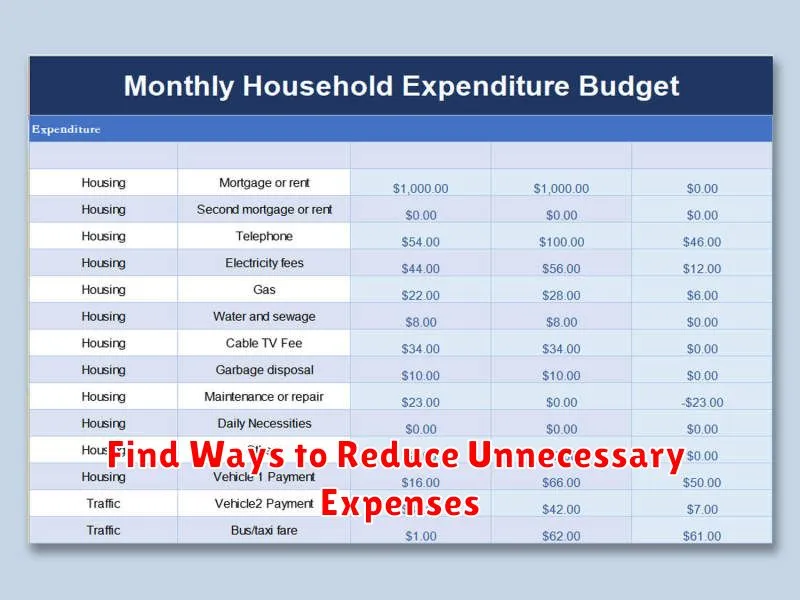

Find Ways to Reduce Unnecessary Expenses

Creating a realistic monthly budget is crucial for financial stability, and a big part of that is identifying and reducing unnecessary expenses. These are the things you spend money on that you could easily live without, or that you could find cheaper alternatives for.

Start by tracking your spending for a month or two to see where your money is going. Look for things like subscriptions you’re not using, expensive coffee shop trips, or takeout meals you could make at home. You may be surprised by how much money you’re spending on small, unnecessary things.

Once you’ve identified your unnecessary expenses, you can start cutting back. This doesn’t have to be a drastic overhaul, but even small changes can add up over time. For example, you could switch to a cheaper cell phone plan, try cooking at home more often, or look for deals and discounts on things you need.

Finding ways to reduce unnecessary expenses is a great way to free up more money in your budget to save for your goals, pay down debt, or simply enjoy more financial freedom. Start small, and you’ll be surprised at how much you can save!

Automate Your Savings and Bill Payments

Automating your savings and bill payments is a crucial step towards a stress-free financial life. It eliminates the risk of late fees, reduces mental strain, and helps you reach your financial goals faster. Here’s how to leverage automation:

Set Up Automatic Transfers: Most banks offer automated transfer services. You can schedule regular transfers from your checking account to your savings account. This ensures consistent saving without needing to manually transfer funds.

Utilize Bill Pay Features: Online banking platforms and budgeting apps offer bill pay features. You can schedule payments for recurring bills like rent, utilities, and subscriptions. This guarantees timely payments and prevents late fees.

Explore Automated Savings Apps: Several apps are designed to automate saving. They round up your purchases to the nearest dollar and deposit the difference into your savings account. These apps can help you accumulate savings effortlessly.

By automating your savings and bill payments, you gain peace of mind knowing that your finances are managed efficiently. It frees up your time and allows you to focus on other aspects of your life, while confidently working towards your financial goals.

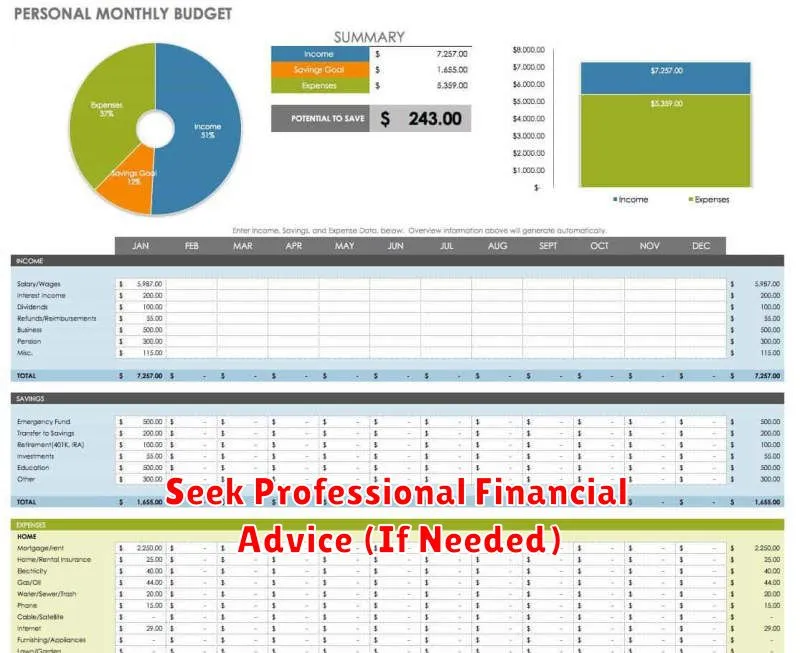

Seek Professional Financial Advice (If Needed)

While creating a budget can be a DIY project for many, there are situations where seeking professional financial advice is highly recommended. If you find yourself facing complex financial situations like significant debt, substantial income fluctuations, or planning for major life events like retirement or buying a home, a financial advisor can provide invaluable guidance.

Financial advisors offer a comprehensive understanding of financial markets, investment strategies, and tax implications, which can be crucial in navigating intricate financial landscapes. Their expertise can help you develop a personalized plan that aligns with your specific goals and risk tolerance.

Remember, seeking professional advice isn’t a sign of weakness, but rather a proactive step towards achieving your financial aspirations with confidence. A financial advisor can act as a trusted partner, providing objective guidance and support to ensure you make informed decisions about your money.

{kind=link}