Are you a conservative investor seeking a safe and steady way to grow your wealth? Investing in bonds could be the perfect solution for you. Bonds are considered a less risky investment than stocks, making them an ideal choice for investors who prioritize capital preservation and income generation. With a diverse range of bond options available, you can tailor your portfolio to your individual risk tolerance and financial goals.

This comprehensive guide will walk you through the fundamentals of bond investing, covering essential concepts like bond types, risk factors, and strategies for building a diversified bond portfolio. Whether you’re a seasoned investor or just starting your financial journey, this article will equip you with the knowledge and insights needed to navigate the world of bonds confidently and achieve your investment objectives.

Understanding Bonds and Their Role in Conservative Investing

Bonds are debt securities that represent a loan made by an investor to a borrower, typically a corporation or government. When you invest in a bond, you are essentially lending money to the issuer in exchange for a promise to repay the principal amount (the original investment) plus interest payments over a specified period. Bonds are considered a more conservative investment than stocks because they generally offer lower returns but also less risk.

Bonds are often seen as a key component of a conservative investment portfolio because they provide stability and income. They are less volatile than stocks, meaning their value tends to fluctuate less over time. This makes them a suitable choice for investors who prioritize capital preservation over high growth.

Here are some key benefits of investing in bonds for conservative investors:

- Income generation: Bonds offer predictable interest payments, providing a consistent income stream.

- Capital preservation: Bonds are generally considered a safer investment than stocks, making them suitable for investors seeking to protect their principal.

- Diversification: Adding bonds to a portfolio can help reduce overall risk by diversifying assets.

When considering bond investments, it’s crucial to understand the risk-return trade-off. While bonds offer lower risk than stocks, they also come with their own set of risks, such as:

- Interest rate risk: If interest rates rise, the value of existing bonds can fall.

- Credit risk: The risk that the issuer may default on its obligation to pay interest and principal.

- Inflation risk: Inflation can erode the purchasing power of bond interest payments.

By carefully considering these risks and understanding the role of bonds in a conservative investment strategy, investors can make informed decisions about how to allocate their funds.

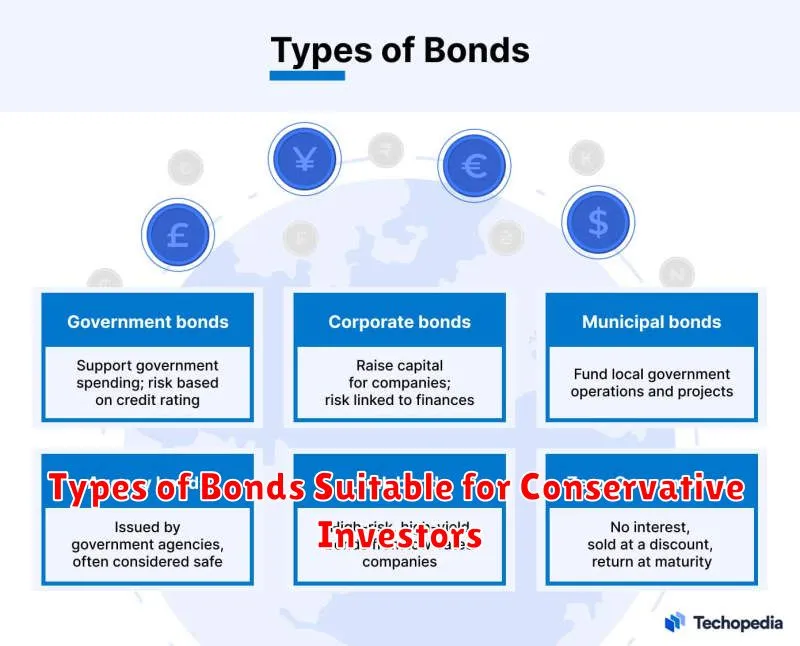

Types of Bonds Suitable for Conservative Investors

Conservative investors prioritize preservation of capital and low risk. When it comes to bonds, certain types are particularly well-suited for this approach. These include:

Treasury Bonds: Issued by the U.S. government, these bonds are considered the safest investment option due to the government’s strong creditworthiness. They offer a low but steady return and are generally less volatile than other bond types.

Investment-Grade Corporate Bonds: These bonds are issued by corporations with strong credit ratings. While slightly riskier than Treasury bonds, they offer potentially higher returns. Look for bonds rated BBB or higher by reputable credit rating agencies like Moody’s and Standard & Poor’s.

Municipal Bonds: Issued by state and local governments, these bonds offer tax-free interest income, which can be attractive to investors in higher tax brackets. They typically carry lower yields compared to other bond types.

Short-Term Bonds: These bonds have shorter maturities, typically less than five years. They are less susceptible to interest rate fluctuations and offer greater stability. A diversified portfolio of short-term bonds can provide a more conservative approach to bond investing.

Laddered Bonds: This strategy involves investing in bonds with staggered maturity dates. This helps to diversify your portfolio and reduce interest rate risk by spreading out maturities. You can create a ladder by purchasing bonds with maturities ranging from one to ten years.

It’s important to remember that even conservative investments carry some risk. However, by carefully selecting the right types of bonds, you can build a portfolio that aligns with your risk tolerance and financial goals.

Assessing Your Risk Tolerance and Investment Goals

Before you even consider investing in bonds, it’s essential to understand your risk tolerance and investment goals. These are crucial factors in determining the right approach for you. Risk tolerance refers to your comfort level with potential losses. A conservative investor generally has a low risk tolerance and prefers investments that are considered safer, even if it means lower potential returns.

Your investment goals are the financial objectives you hope to achieve. Are you saving for retirement, a down payment on a house, or your children’s education? Your goals will influence the type of bonds you choose and the timeframe for your investments. For example, a short-term goal, like a down payment, might require a more conservative bond strategy than a long-term goal like retirement.

Bond Yields, Interest Rates, and Their Impact on Returns

As a conservative investor, you’re likely drawn to bonds for their potential stability and predictable income. Understanding the relationship between bond yields, interest rates, and their impact on your returns is crucial for making informed investment decisions.

Bond yields represent the annual return you receive as a percentage of the bond’s face value. They move inversely to interest rates set by the Federal Reserve. When interest rates rise, bond yields generally fall, and vice versa.

Here’s why: As interest rates rise, new bonds are issued with higher yields to attract investors. This makes existing bonds with lower yields less attractive, leading to their prices falling. Conversely, when interest rates decline, the attractiveness of existing bonds with higher yields increases, pushing their prices up.

This inverse relationship is important for understanding how bond investments can be affected by changes in the economic landscape. For instance, if you hold a bond with a fixed interest rate and the Federal Reserve raises rates, your bond’s value may decline. However, you will continue to receive the fixed interest payments until the bond matures.

Therefore, it’s crucial to monitor interest rate trends and consider their impact on the value of your bond holdings. While bond yields may fluctuate in the short term, they generally offer a stable and predictable income stream over the long term, making them a valuable part of a diversified portfolio.

Bond Maturity Dates and Their Significance

Understanding bond maturity dates is crucial for any conservative investor. A bond’s maturity date signifies the date when the issuer will repay the principal amount borrowed from the bondholder. This date is fixed at the time of issuance and is an essential factor to consider when making investment decisions.

The maturity date directly impacts the bond’s lifespan and its associated risks and returns.

Short-term bonds, maturing within a year, are typically considered less risky but offer lower yields. Long-term bonds, maturing in ten years or more, provide the potential for higher returns but come with greater interest rate risk.

As an investor, understanding the maturity date allows you to choose bonds aligned with your investment goals and risk tolerance. If you require predictable income and capital preservation, short-term bonds might be a better fit. On the other hand, if you’re willing to accept greater risk for the potential of higher returns, long-term bonds could be more suitable.

Furthermore, the maturity date plays a role in bond price fluctuations. As interest rates rise, bond prices generally fall, particularly for long-term bonds. Conversely, when interest rates decline, bond prices tend to increase, especially for long-term bonds. Therefore, the maturity date can significantly impact your investment returns, particularly in a fluctuating interest rate environment.

In conclusion, understanding bond maturity dates is crucial for conservative investors seeking to minimize risk and maximize returns. By carefully considering the maturity date of a bond, you can make informed investment decisions aligned with your financial goals and risk tolerance.

Diversifying Your Portfolio with Bonds

As a conservative investor, you likely prioritize preserving capital and achieving steady returns. While stocks offer the potential for higher growth, they also carry greater risk. Bonds, on the other hand, can provide a valuable addition to your portfolio by offering diversification and reducing overall volatility.

Bonds represent loans that you make to a borrower, typically a government or corporation. In return for lending your money, you receive regular interest payments (coupon payments) and the principal amount (face value) back at maturity. Bonds generally offer lower returns than stocks but are also considered less risky.

Here’s how bonds can diversify your portfolio:

- Reduced Volatility: Bonds tend to move in the opposite direction of stocks, providing a counterbalance to market fluctuations. When stock prices decline, bond prices often rise, helping to cushion your overall portfolio.

- Income Generation: Bonds provide regular interest payments, contributing to your portfolio’s overall income stream.

- Preservation of Capital: Bonds are generally considered less risky than stocks, making them an excellent option for preserving capital and protecting your investments from significant losses.

By including bonds in your portfolio, you can achieve a more balanced and diversified investment strategy, mitigating risk and improving your chances of achieving long-term financial goals.

Strategies for Investing in Bonds: Ladders, Barbell, and More

As a conservative investor, bonds offer a valuable way to diversify your portfolio and potentially generate income. There are various strategies you can employ when investing in bonds to manage risk and potentially maximize returns. Here are a few popular strategies:

Laddered Portfolio

A laddered portfolio involves purchasing bonds with different maturities, creating a “ladder” of maturity dates. For example, you might invest in bonds maturing in one, two, three, and four years. This strategy helps to mitigate interest rate risk because as one bond matures, you reinvest the proceeds into a new bond with a longer maturity, allowing you to ladder your portfolio over time. This can provide a steady stream of income while gradually extending the average maturity of your bond holdings.

Barbell Strategy

The barbell strategy emphasizes diversification by allocating funds to both short-term and long-term bonds. For instance, you might invest in bonds with a one-year maturity and bonds with a 10-year maturity. This approach aims to balance the potential for capital appreciation of long-term bonds with the stability of short-term bonds. It can also help to reduce interest rate risk by mitigating the impact of fluctuating interest rates.

Bullet Strategy

In a bullet strategy, you focus your investment on bonds with a single maturity date. This approach is less diversified than laddering or barbell strategies, but it can be simpler to manage and potentially offer higher returns if you accurately predict interest rate movements. However, it also carries a higher risk of capital loss if interest rates rise significantly.

Bond Mutual Funds and ETFs

Investing in bond mutual funds or exchange-traded funds (ETFs) can provide a convenient and diversified way to gain exposure to the bond market. These funds typically hold a basket of bonds, offering diversification and professional management. When choosing a bond fund, it’s important to consider its expense ratio, credit quality, and investment objectives.

Ultimately, the best bond investment strategy for you will depend on your individual risk tolerance, financial goals, and investment time horizon. Consider consulting with a financial advisor to determine the most appropriate strategy for your specific circumstances.

Bond Funds vs. Individual Bonds: Pros and Cons

Conservative investors often turn to bonds for their portfolio’s stability and lower risk compared to stocks. But choosing between investing in bond funds and individual bonds can be a tricky decision. Here’s a breakdown of the pros and cons of each:

Bond Funds

Pros:

- Diversification: Bond funds provide instant diversification across various sectors, maturities, and credit ratings. This spreads risk, reducing the impact of individual bond defaults.

- Professional Management: Fund managers handle the selection, buying, and selling of bonds, taking the burden off the investor.

- Liquidity: Shares of bond funds are easily bought and sold on the stock market, offering greater liquidity than individual bonds.

- Low Minimum Investment: Many bond funds have low minimum investment requirements, making them accessible to a wider range of investors.

Cons:

- Fees: Bond funds typically charge management fees and expense ratios, which can eat into returns.

- Less Control: Investors have limited control over the specific bonds held within a fund, potentially limiting their ability to tailor their portfolio to specific needs.

- Tax Inefficiencies: Bond fund distributions are subject to taxes, potentially creating tax inefficiencies compared to holding individual bonds.

Individual Bonds

Pros:

- Higher Potential Returns: Individual bonds can offer higher returns than bond funds, especially if the investor carefully chooses bonds with favorable interest rates and credit ratings.

- Greater Control: Investors have complete control over the specific bonds they purchase, allowing them to tailor their portfolio to specific goals and risk tolerance.

- Tax Advantages: Holding individual bonds can offer tax advantages in certain scenarios, such as when bonds are held to maturity.

Cons:

- Lack of Diversification: Investing in a limited number of individual bonds exposes investors to greater risk from defaults or market fluctuations.

- Higher Minimum Investment: Individual bonds often have higher minimum investment requirements than bond funds, limiting accessibility for smaller investors.

- Limited Liquidity: Trading individual bonds can be difficult and time-consuming, especially for bonds that are not actively traded.

The choice between bond funds and individual bonds ultimately depends on your investment goals, risk tolerance, and available resources. For conservative investors seeking diversification, professional management, and liquidity, bond funds can be a good option. However, if you’re looking for higher potential returns, greater control, and tax advantages, individual bonds may be a better fit.

Managing Interest Rate Risk as a Bond Investor

Bonds are considered a conservative investment, but they are not without risk. One of the biggest risks for bond investors is interest rate risk. This is the risk that interest rates will rise, causing the value of your bonds to fall. When interest rates rise, new bonds are issued with higher interest rates, making your existing bonds with lower interest rates less attractive to investors. This can lead to a decrease in the market value of your bonds.

There are a few things you can do to manage interest rate risk as a bond investor:

- Invest in bonds with shorter maturities. The shorter the maturity of a bond, the less sensitive it is to interest rate changes. This is because shorter-term bonds have less time for interest rates to rise and affect their value.

- Invest in bonds with higher coupon rates. A higher coupon rate means the bond pays a higher interest rate, which can help offset the negative impact of rising interest rates.

- Diversify your bond portfolio. Don’t put all your eggs in one basket. Diversifying your portfolio by investing in bonds with different maturities, credit ratings, and issuers can help to reduce the overall risk of your portfolio.

It’s also important to remember that interest rates can fluctuate, and there is no guarantee that they will always rise. If interest rates fall, the value of your bonds could increase. However, it’s important to be aware of the risks associated with interest rate changes and take steps to manage them.

Tax Implications of Bond Investments

Bonds are considered a conservative investment option, but it’s essential to understand the tax implications of bond investments. The tax treatment of bond income can vary depending on the type of bond and your individual circumstances.

Interest Income from bonds is generally taxed as ordinary income, meaning it’s subject to your regular income tax rate. This can range from 10% to 37%, depending on your tax bracket. However, municipal bonds are often exempt from federal income tax, and sometimes state and local taxes as well, making them attractive to investors in higher tax brackets.

Capital Gains are realized when you sell a bond for more than you paid for it. Capital gains are taxed at either 0%, 15%, or 20% depending on your income and holding period. Bonds held for more than a year are eligible for long-term capital gains rates, which are generally lower than ordinary income rates.

It’s important to consult with a financial advisor or tax professional to understand the specific tax implications of your bond investments and how they might affect your overall tax liability. They can help you navigate the complexities of bond taxation and make informed decisions based on your individual financial goals.

Monitoring and Rebalancing Your Bond Portfolio

Once you’ve established your bond portfolio, it’s crucial to monitor and rebalance it regularly. This ensures that your portfolio remains aligned with your investment goals and risk tolerance.

Monitoring involves keeping track of your portfolio’s performance and making sure it’s performing as expected. This includes tracking your bond yields, maturity dates, and credit ratings. Rebalancing involves adjusting your portfolio’s asset allocation as needed. This can be necessary if your portfolio has drifted too far from your initial target allocation, or if your investment goals or risk tolerance have changed.

A good rule of thumb is to rebalance your portfolio at least once a year. You may need to rebalance more frequently if the market is volatile or if your investment goals change significantly.

Here are some specific tips for monitoring and rebalancing your bond portfolio:

- Review your portfolio’s performance regularly. Compare your actual returns to your expected returns and make adjustments as needed.

- Monitor your bond yields. As interest rates rise, bond yields typically fall and vice versa. If interest rates are rising, you may want to consider selling some of your bonds and reinvesting the proceeds in higher-yielding bonds.

- Check your bond maturity dates. As bonds approach maturity, their prices typically become more volatile. If you’re concerned about market volatility, you may want to consider selling bonds that are approaching maturity and reinvesting the proceeds in bonds with longer maturities.

- Review your credit ratings. If the credit rating of one of your bonds is downgraded, it could signal that the bond is becoming riskier. You may want to consider selling the bond or reducing your exposure to the bond.

By monitoring and rebalancing your bond portfolio regularly, you can help ensure that it remains aligned with your investment goals and risk tolerance. This will help you to achieve your investment goals over the long term.

Common Mistakes to Avoid When Investing in Bonds

Bonds are a crucial part of a diversified portfolio, especially for conservative investors seeking steady income and lower risk. However, even experienced investors can fall prey to common mistakes that can negatively impact their bond investments. Here are some pitfalls to avoid:

Not Diversifying: Investing in just a few bonds can expose you to significant risk if those specific bonds perform poorly. Diversifying your portfolio across different bond types, maturities, and issuers helps to mitigate this risk and ensure a smoother ride.

Ignoring Interest Rate Risk: Interest rates and bond prices move in opposite directions. When interest rates rise, the value of your existing bonds may decline. It’s essential to consider the potential impact of rising rates and to choose bonds with appropriate maturities and coupon rates. You can also consider investing in bonds with floating interest rates that adjust to market conditions.

Neglecting Credit Risk: The creditworthiness of the issuer plays a crucial role in determining a bond’s safety and potential return. Avoid investing in bonds issued by companies with poor credit ratings or those facing financial distress. Stick to bonds with high credit ratings from reputable entities.

Chasing High Yields: While high yields can be tempting, they often come with higher risk. Avoid falling into the trap of chasing high yields at the expense of safety. Focus on bonds with reasonable yields and strong credit ratings.

Failing to Monitor Your Portfolio: After purchasing bonds, don’t simply forget about them. Regularly monitor your portfolio’s performance, keeping track of interest rate movements, credit rating changes, and other factors that could affect your investments. Consider rebalancing your portfolio periodically to maintain your desired asset allocation and risk profile.

{kind=link}