Are you feeling overwhelmed by your finances? Do you dream of reaching your financial goals, but don’t know where to start? A financial plan is the key to unlocking your financial future. It provides a clear roadmap to help you achieve your goals, whether it’s buying a home, paying off debt, or saving for retirement. By taking the time to create a 5-year financial plan, you’ll gain control of your money and set yourself up for long-term success.

This guide will walk you through the steps to create a comprehensive financial plan that will help you navigate the next five years with confidence. We’ll cover everything from setting realistic goals and tracking your spending to investing wisely and managing debt effectively. Whether you’re just starting out or looking to revamp your existing plan, this article provides valuable insights and actionable tips to help you build a solid financial foundation for the future.

Define Your Financial Goals

Before you start making a financial plan, you need to know where you want to go. This is where defining your financial goals comes in. What do you want to achieve with your finances in the next five years? Are you saving for a down payment on a house, paying off debt, investing for retirement, or something else entirely?

When setting goals, it’s important to be specific, measurable, achievable, relevant, and time-bound (SMART). For example, instead of saying “I want to save money,” a better goal would be “I want to save $10,000 for a down payment on a house by the end of 2024.”

Having clear financial goals will give you direction and motivation. It will also help you track your progress and stay accountable to your financial plan.

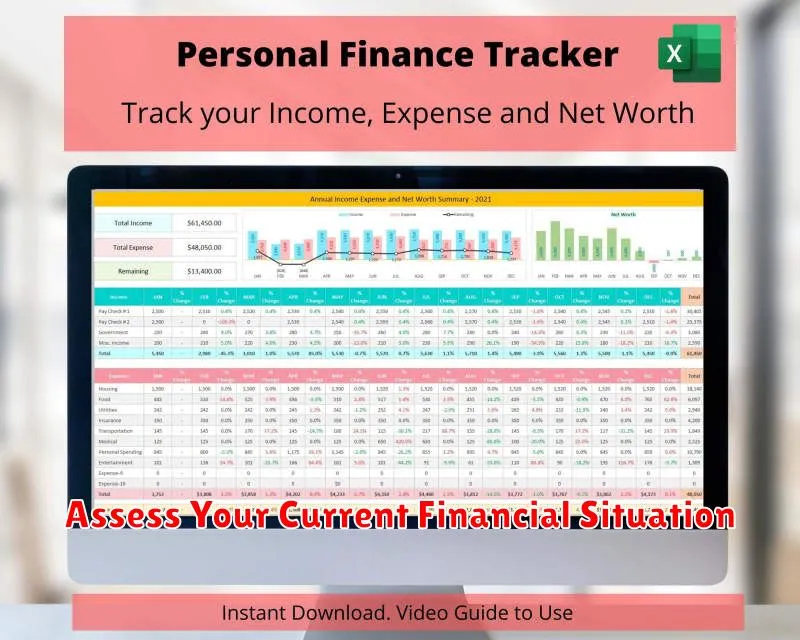

Assess Your Current Financial Situation

Before you can start planning for the future, it’s essential to understand your current financial standing. This involves taking a close look at your income, expenses, assets, and debts.

Income: List all sources of income, including your salary, wages, investments, and any other regular income streams. Be sure to consider any potential income changes in the next five years, such as raises or promotions.

Expenses: Track all your expenses for a month or two to get a clear picture of where your money is going. Categorize expenses, such as housing, transportation, food, utilities, entertainment, and debt payments. This will help you identify areas where you can potentially cut back.

Assets: Include the value of your assets, such as your home, car, savings accounts, investments, and retirement funds. Assess the potential appreciation or depreciation of these assets over the next five years.

Debts: List all your outstanding debts, including credit card balances, student loans, mortgages, and personal loans. Note the interest rates and minimum payments for each debt.

Net Worth: Calculate your net worth by subtracting your liabilities (debts) from your assets. This gives you a snapshot of your overall financial health.

By thoroughly assessing your current financial situation, you’ll gain a better understanding of your financial strengths and weaknesses. This will help you set realistic financial goals for the next five years.

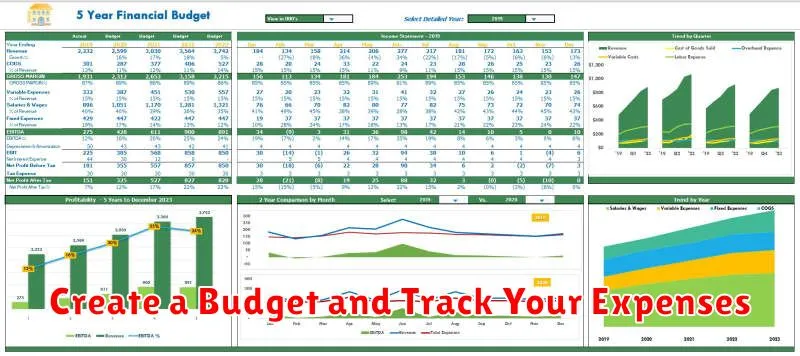

Create a Budget and Track Your Expenses

The foundation of a successful financial plan is a well-structured budget. It allows you to understand your income and spending patterns, identify areas for improvement, and make informed financial decisions.

Start by creating a detailed list of all your income sources, including salary, investments, and any other regular income. Next, meticulously track your expenses for at least a month. Use a spreadsheet, budgeting app, or even a simple notebook to record every dollar spent, categorizing it into essential needs like housing, food, transportation, and discretionary spending like entertainment, dining out, and subscriptions.

Once you have a clear picture of your income and expenses, you can start to analyze your spending habits. Identify areas where you can potentially reduce costs. This might involve negotiating bills, finding cheaper alternatives, or simply being more mindful of your spending. It’s crucial to strike a balance between meeting your needs and creating room for financial goals.

Tracking your expenses regularly not only helps you identify spending leaks but also allows you to monitor progress towards your financial goals. As you make adjustments and stick to your budget, you’ll gain a sense of control over your finances and build a solid foundation for your five-year plan.

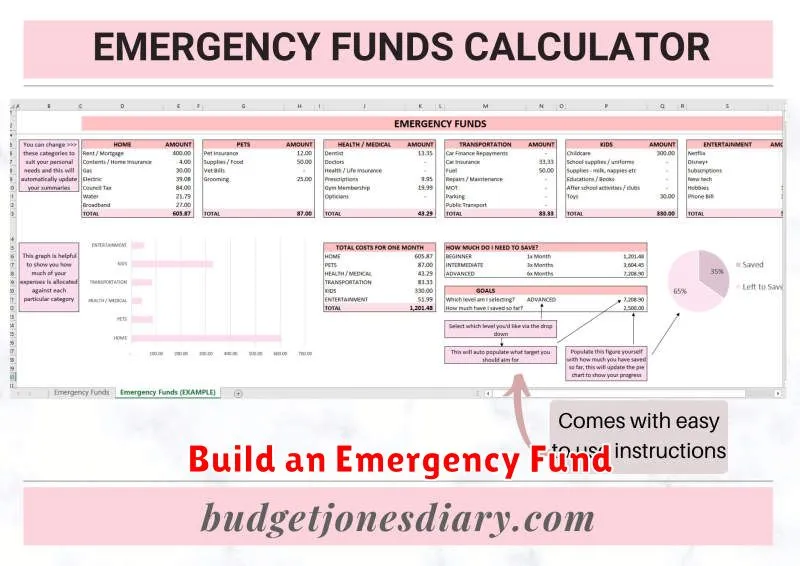

Build an Emergency Fund

An emergency fund is a crucial component of any financial plan, particularly in the next five years. It acts as a safety net to cover unexpected expenses such as medical bills, job loss, car repairs, or home emergencies. A well-funded emergency fund can prevent you from going into debt or depleting your savings during unforeseen circumstances.

Aim to have 3-6 months’ worth of living expenses saved in your emergency fund. This amount provides enough cushion to navigate potential financial challenges without significantly impacting your financial stability.

To build your emergency fund, prioritize regular contributions, even if they’re small. Automate contributions from your checking account to your emergency fund savings account to ensure consistent progress. Consider using the “snowball method” to prioritize paying off high-interest debt while simultaneously building your emergency fund.

It’s crucial to keep your emergency fund accessible. Storing it in a high-yield savings account or money market account ensures both safety and liquidity, allowing you to access the funds quickly when needed.

Building an emergency fund is an essential step in securing your financial future. By prioritizing this critical component, you can navigate unexpected challenges with greater peace of mind and protect your long-term financial goals.

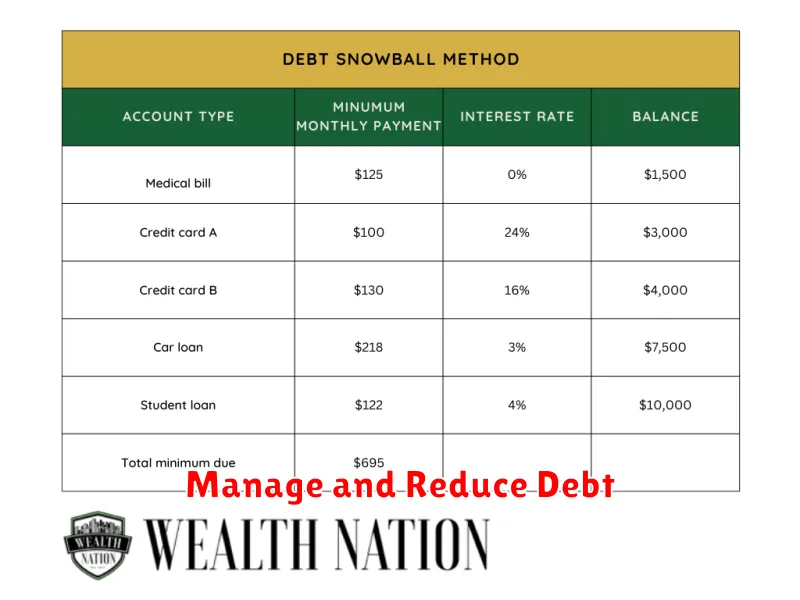

Manage and Reduce Debt

A crucial part of any financial plan is effectively managing and reducing debt. Uncontrolled debt can cripple your financial progress, making it difficult to reach your long-term goals. Here are some key steps to tackle debt within the next five years:

1. Track Your Spending and Debt: The first step is to gain a clear understanding of your current financial situation. Create a detailed budget to track your income and expenses. This will help you identify areas where you can cut back and allocate those funds towards debt repayment.

2. Prioritize Debt Repayment: Once you have a clear view of your debts, prioritize repayment based on interest rates. Focus on paying down high-interest debts first, such as credit cards, as they accumulate the most interest over time. Consider using strategies like the snowball method or the avalanche method to effectively manage your debt repayment plan.

3. Explore Consolidation or Refinancing: If you have multiple high-interest debts, you might consider consolidating them into a single loan with a lower interest rate. This can simplify your debt management and potentially lower your monthly payments. However, make sure to carefully research and compare options before making any decisions.

4. Seek Professional Help: If you feel overwhelmed by debt, don’t hesitate to seek guidance from a financial advisor or credit counselor. These professionals can provide personalized advice, develop a customized debt management plan, and negotiate with creditors on your behalf.

5. Stay Committed and Consistent: Repaying debt requires discipline and consistency. Stick to your budget, prioritize debt payments, and celebrate your progress along the way. By staying committed to your plan, you’ll steadily reduce your debt and create a stronger financial foundation for the future.

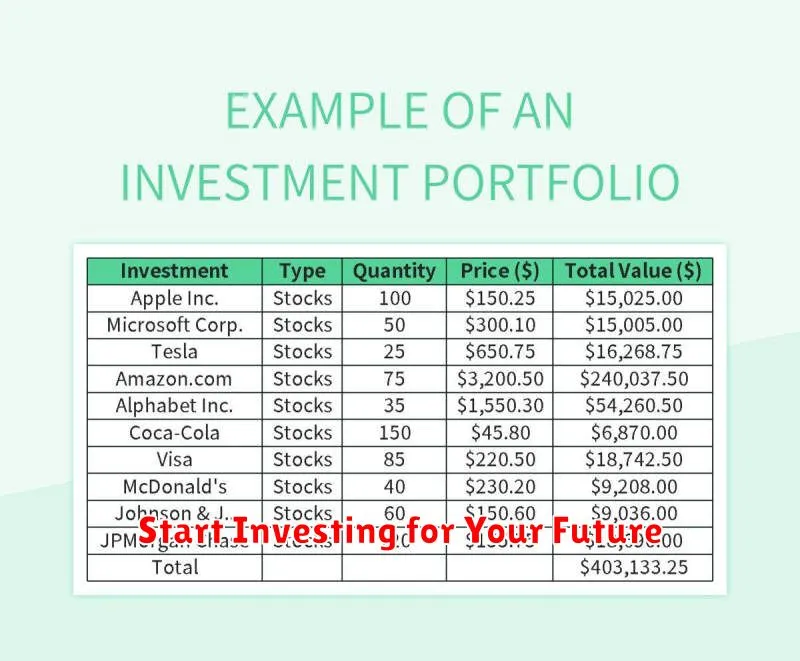

Start Investing for Your Future

A financial plan for the next five years should include a solid investing strategy. Investing is crucial for long-term financial security, allowing your money to grow and outpace inflation. It’s never too early or too late to start investing, and even small contributions can make a significant difference over time.

Before diving into specific investments, understand your risk tolerance, investment goals, and time horizon. Risk tolerance refers to your comfort level with the potential for losses. Investment goals could include saving for retirement, a down payment on a house, or your children’s education. Time horizon refers to how long you plan to keep your investments.

Consider a diversified portfolio that includes a mix of assets like stocks, bonds, and real estate. Stocks offer potential for higher returns but come with higher risk. Bonds are considered less risky and provide steady income. Real estate can be a good long-term investment, offering both appreciation potential and rental income.

Seek advice from a financial advisor if you need help creating an investment strategy. They can assess your individual circumstances and recommend suitable investment options. Remember, consistent investing, even small amounts regularly, can help you reach your financial goals.

Review and Adjust Your Plan Regularly

A financial plan isn’t a set-it-and-forget-it document. Your life circumstances, financial goals, and the overall economy are constantly changing. That’s why it’s crucial to review and adjust your plan regularly, ideally at least once a year. This allows you to stay on track and adapt your strategy to any new challenges or opportunities.

During your review, consider factors like:

- Changes in your income or expenses: Did you get a raise or take on new financial obligations?

- Progress towards your goals: Are you on track to meet your savings goals, pay off debt, or reach other financial milestones?

- Market fluctuations: Have interest rates changed, or are your investments performing well or poorly?

- Life events: Did you get married, have a child, or experience another significant life event that impacts your finances?

Based on your review, make necessary adjustments to your plan. This might involve:

- Adjusting your budget: Re-evaluate your spending habits and allocate funds accordingly.

- Re-evaluating your investment strategy: Perhaps it’s time to shift your portfolio allocation, take on more risk, or become more conservative.

- Re-prioritizing your goals: Your priorities might change over time, so it’s important to ensure your financial plan still aligns with them.

By consistently reviewing and adjusting your financial plan, you’ll be better equipped to reach your goals, weather financial storms, and navigate the ever-changing economic landscape.

Plan for Unexpected Events

Life is unpredictable, and unexpected events can happen at any time. These events can have a significant financial impact, so it’s essential to plan for them. A contingency fund is a vital part of your financial plan. This fund should have enough money to cover three to six months of essential expenses, such as rent, utilities, and groceries.

Here are some tips for creating a contingency fund:

- Set a specific goal: Determine the amount you want to save for your contingency fund. This goal should be realistic and achievable.

- Automate your savings: Set up automatic transfers from your checking account to your savings account. This will help you stay on track and avoid forgetting to save.

- Track your progress: Regularly check your savings balance to monitor your progress towards your goal.

In addition to a contingency fund, consider these strategies:

- Review your insurance coverage: Ensure you have adequate health, disability, and life insurance coverage to protect yourself and your family from financial hardship.

- Have a plan for emergencies: Identify potential emergencies and create a plan for how you will handle them. This might include knowing how to access emergency funds, contacting family members, and getting essential supplies.

By planning for unexpected events, you can reduce the financial stress that can accompany these situations and ensure your financial stability. This will help you stay on track with your long-term financial goals.

Seek Professional Financial Advice

While you can create a basic financial plan on your own, seeking professional financial advice can be immensely beneficial. A financial advisor can provide personalized guidance based on your specific circumstances, risk tolerance, and financial goals. They can help you:

- Develop a comprehensive financial plan that addresses all aspects of your financial life, including investments, retirement planning, debt management, and insurance.

- Identify potential financial risks and create strategies to mitigate them.

- Optimize your investment portfolio for growth and risk management.

- Provide ongoing support and adjustments as your financial needs evolve.

A financial advisor can also help you stay accountable to your financial goals and make informed decisions. They can provide objective advice, free from emotional biases that can cloud your judgment. Consulting a financial advisor is an investment in your financial well-being and can help you achieve your long-term financial aspirations.

Stay Informed about Financial Trends

Staying informed about financial trends is crucial when crafting a financial plan. The economic landscape is constantly evolving, with interest rates, inflation, and market performance fluctuating. By understanding these trends, you can make more informed decisions about your investments, spending, and debt management.

Here are some key areas to stay informed about:

- Interest rates: Interest rates can impact the cost of borrowing money for mortgages, loans, and credit cards, as well as the returns on savings accounts and bonds. Understanding interest rate movements can help you make better decisions about borrowing and saving.

- Inflation: Inflation erodes the purchasing power of your money. Monitoring inflation rates can help you adjust your spending and investment strategies to stay ahead of rising prices.

- Market performance: Stock markets, bond markets, and other investment vehicles fluctuate in value. Staying informed about market trends can help you make more informed investment decisions and manage your portfolio effectively.

You can stay up-to-date on financial trends through various sources, such as:

- Financial news websites: Websites like Bloomberg, CNBC, and The Wall Street Journal provide up-to-the-minute coverage of financial markets and economic indicators.

- Financial magazines: Publications like Forbes, Fortune, and Money offer in-depth analysis of financial trends and investment strategies.

- Economic reports: Government agencies, such as the Federal Reserve and the Bureau of Labor Statistics, release regular economic reports that provide data on inflation, unemployment, and other key economic indicators.

- Financial podcasts: Podcasts like Planet Money and The Indicator provide accessible and engaging discussions about financial topics.

By staying informed about financial trends, you can make more informed decisions about your financial planning, investments, and overall financial well-being. Remember, a successful financial plan is a flexible one that adapts to the ever-changing economic environment.

{kind=link}