Are you in your 50s and beyond and starting to feel the pressure of retirement creeping up? Don’t worry, you’re not alone. Many people find themselves wondering how to save enough money for a comfortable retirement, especially when they’ve got a lot of other expenses to contend with. But it’s never too late to start planning for your future, and the good news is that there are a number of strategies you can use to catch up on your savings and ensure a secure retirement.

This article will explore practical and effective strategies for saving for retirement in your 50s and beyond. We’ll delve into the key factors to consider, including catching up on contributions, maximizing your retirement accounts, adjusting your lifestyle, and seeking professional guidance. Whether you’re just starting to think about retirement or looking to boost your existing savings plan, this guide will equip you with the knowledge and tools to confidently navigate your financial future.

The Importance of Catching Up on Retirement Savings

If you’re in your 50s or beyond and haven’t saved as much as you’d like for retirement, you’re not alone. Many people find themselves playing catch-up later in life. But the good news is that it’s never too late to start saving for retirement. Even if you’ve only got a few years left before you plan to retire, it’s still possible to make a significant impact on your future financial well-being.

The importance of catching up on retirement savings cannot be overstated. The longer you wait to save, the more money you’ll need to put away each month to reach your retirement goals. It’s also essential to recognize that the power of compound interest works in your favor. The earlier you start saving, the more time your money has to grow, making it easier to reach your financial goals.

There are several benefits to catching up on retirement savings, even if you’re starting later in life. You’ll have more financial security in retirement, allowing you to enjoy your golden years without worrying about money. It can also provide you with peace of mind, knowing that you’re financially prepared for the future. Moreover, it allows you to maintain your desired lifestyle after you retire. This could include traveling, pursuing hobbies, or helping out family members.

Catching up on retirement savings may seem daunting, but it’s achievable with careful planning and commitment. There are several strategies you can utilize, such as increasing your contributions to your retirement accounts, maximizing tax advantages, and exploring additional savings opportunities. Consulting a financial advisor can also be beneficial in developing a personalized savings plan tailored to your needs and circumstances.

Remember, it’s never too late to start saving for retirement. By prioritizing saving and taking proactive steps, you can secure a financially comfortable future. It’s crucial to understand that catching up on retirement savings requires discipline and commitment but can significantly improve your financial well-being in the long run.

Maximizing Contributions to Retirement Accounts

One of the most important things you can do to prepare for retirement in your 50s and beyond is to maximize your contributions to retirement accounts. This includes both traditional and Roth IRAs, as well as 401(k)s and other employer-sponsored retirement plans. The sooner you start contributing to these accounts, the more time your money has to grow through compounding interest.

The amount you can contribute to a traditional or Roth IRA is $6,500 per year if you’re 50 or older. For 401(k)s, the limit is $22,500 in 2023. You can also make catch-up contributions if you are 50 or older, allowing you to contribute an additional $7,500 to a 401(k) and $1,000 to a Roth IRA.

Exploring Different Retirement Savings Plans (401(k), IRA)

If you’re in your 50s or beyond, retirement may seem like it’s right around the corner. It’s never too late to start saving for retirement, and it’s essential to understand the different retirement savings plans available to you. Two popular options are the 401(k) and IRA.

A 401(k) is a retirement savings plan offered by your employer. You can contribute pre-tax dollars to the plan, which means you won’t have to pay taxes on your earnings until you withdraw them in retirement. Many employers also offer a matching contribution, meaning they’ll contribute a certain percentage of your salary to your 401(k) account. This is essentially free money, so it’s a great benefit to take advantage of.

An IRA, or Individual Retirement Account, is a retirement savings plan that you can set up yourself. There are two main types of IRAs: traditional IRAs and Roth IRAs. With a traditional IRA, you can contribute pre-tax dollars and pay taxes on your earnings in retirement. A Roth IRA allows you to contribute after-tax dollars, and your withdrawals in retirement are tax-free. The main difference between these two types of IRAs is the tax treatment of your contributions and withdrawals.

The best retirement savings plan for you will depend on your individual circumstances. If you’re employed, you should definitely take advantage of a 401(k) if your employer offers one. If you’re self-employed or don’t have a 401(k), an IRA is a great alternative. It’s important to understand the rules and regulations of each plan before making a decision.

In addition to traditional 401(k)s and IRAs, there are a variety of other retirement savings plans available, such as solo 401(k)s and SEP IRAs. These are specifically designed for self-employed individuals and small business owners. It’s best to consult with a financial advisor to discuss which plan is right for you based on your unique financial situation.

Investment Strategies for Late-Stage Retirement Savers

Retirement planning in your 50s and beyond demands a strategic approach, especially if you’re playing catch-up. You’re likely closer to retirement and have a shorter time horizon to build your nest egg. Therefore, investment strategies need to be tailored to your specific needs and risk tolerance. Here’s a breakdown of key strategies to consider:

1. Diversification: Diversifying your portfolio across different asset classes, such as stocks, bonds, and real estate, is crucial for managing risk. Consider a mix of growth-oriented and conservative investments to balance potential returns with the need for stability.

2. Risk Tolerance: As you approach retirement, your risk tolerance may shift. You might be less comfortable with high-risk investments, especially if you’re near your retirement date. Shift your portfolio towards more conservative options, like bonds and dividend-paying stocks.

3. Tax Efficiency: Tax-efficient strategies are essential for late-stage savers. Explore options like tax-advantaged retirement accounts (401(k), IRA) and consider the potential tax implications of withdrawing funds from these accounts during retirement.

4. Investment Management: If you’re not comfortable managing investments yourself, consider working with a financial advisor. They can help you build a personalized portfolio, monitor market trends, and adjust your investments as needed.

5. Regular Reviews: Your financial situation and goals may change over time. Regularly review your investment portfolio to ensure it’s aligned with your evolving needs. Make adjustments as necessary to stay on track for a comfortable retirement.

Late-stage retirement saving requires a proactive approach and careful consideration of investment strategies. By focusing on diversification, risk management, tax efficiency, and professional guidance, you can maximize your chances of achieving your retirement goals.

Managing Risk and Preserving Capital

In your 50s and beyond, the time horizon for your investments shrinks, making risk management paramount. Your focus shifts from maximizing growth to preserving capital and generating a steady stream of income. Here’s how to approach it:

Reduce exposure to volatile assets: Gradually shift away from stocks and towards less risky investments like bonds, real estate, and fixed-income securities. This helps buffer against potential market downturns and safeguards your retirement nest egg.

Diversify your portfolio: Don’t put all your eggs in one basket. Diversify your investments across different asset classes, industries, and geographical locations. This spreads the risk and reduces the impact of any single investment performing poorly.

Consider guaranteed income streams: Explore options like annuities, which provide a guaranteed stream of income for life. While annuities may have some drawbacks, they offer peace of mind knowing you’ll have a steady source of income in retirement.

Work with a financial advisor: A financial advisor can provide personalized guidance on managing risk and preserving capital, factoring in your individual circumstances, risk tolerance, and financial goals. They can help you develop a comprehensive retirement plan that minimizes risk while maximizing returns.

Creating a Realistic Retirement Budget

Saving for retirement in your 50s and beyond can be daunting, but it’s never too late to start. A key aspect of your retirement planning is creating a realistic budget that accounts for your expenses, income sources, and lifestyle goals.

Start by listing all your essential expenses, including housing, food, healthcare, transportation, and utilities. Don’t forget about discretionary spending like travel, entertainment, and hobbies. A good way to track your spending is by using a budgeting app or a spreadsheet.

Next, consider your income sources in retirement. This may include Social Security, pensions, savings, and investments. Estimate how much income you’ll need each year to cover your expenses.

You can adjust your spending habits to fit your budget. Consider cutting back on non-essential expenses, finding ways to reduce housing costs, and negotiating lower bills. Also, explore ways to generate additional income, such as part-time work or selling unwanted items.

A realistic retirement budget is essential for a comfortable and financially secure retirement. By taking the time to create a well-thought-out budget, you can set yourself up for success in your golden years.

Downsizing and Reducing Expenses

As you approach retirement, minimizing your expenses can significantly impact your financial security. One of the most impactful ways to do this is through downsizing. This involves moving to a smaller home, which can reduce housing costs, property taxes, and maintenance expenses. Downsizing allows you to free up equity from your current home, which you can use to boost your retirement savings.

Beyond housing, there are numerous other areas where you can reduce expenses. Consider renegotiating your debt, such as loans or credit cards, for lower interest rates. Analyze your monthly bills, like utilities, cable, and streaming services, to identify areas where you can cut back or switch to more affordable options. Finally, review your insurance policies to see if you can adjust coverage or find more competitive rates.

Remember, even small changes can have a substantial impact over time. By diligently analyzing your expenses and implementing strategies to reduce them, you’ll be well on your way to achieving a more comfortable and financially secure retirement.

Working Part-Time in Retirement

If you’re thinking about working part-time in retirement, you’re not alone. Many people find that they need to work part-time to supplement their retirement income. And for some, working part-time can be a great way to stay active and engaged.

There are a few things to consider if you’re thinking about working part-time in retirement. First, it’s important to think about your health and whether you’re physically and mentally able to work. Second, you’ll need to consider your financial needs. How much money do you need to make to cover your expenses? Third, you’ll need to think about your time commitments. How much time are you willing to devote to working?

Once you’ve considered these factors, you can start looking for part-time jobs. There are many different types of part-time jobs available, so you should be able to find something that’s a good fit for you. You can look for jobs online, in newspapers, or at local businesses.

Working part-time in retirement can be a great way to supplement your income, stay active, and make new friends. It’s important to plan ahead and make sure that you’re prepared for the challenges that can come with working in retirement.

Delaying Social Security Benefits

If you’re in your 50s or beyond, it’s likely you’re starting to think about retirement. One of the biggest questions you might have is when to start receiving Social Security benefits. While you can begin receiving benefits as early as age 62, delaying them until age 70 can significantly increase your monthly payments.

The Benefits of Delaying

Delaying your benefits allows them to grow by 8% per year until you reach age 70. This means that if you claim benefits at 70, you’ll receive a 24% higher monthly payment than if you started at 62. That extra income can make a big difference in your retirement years.

Considerations

Of course, there are some things to consider before delaying your benefits. If you’re in poor health or have a shorter life expectancy, it might not make sense to delay. You might also want to consider your financial situation. If you need the income now, delaying your benefits might not be the best option.

The Bottom Line

Delaying Social Security benefits can be a smart move for those who are in good health and can afford to wait. It can significantly increase your monthly payments and provide you with more financial security in retirement.

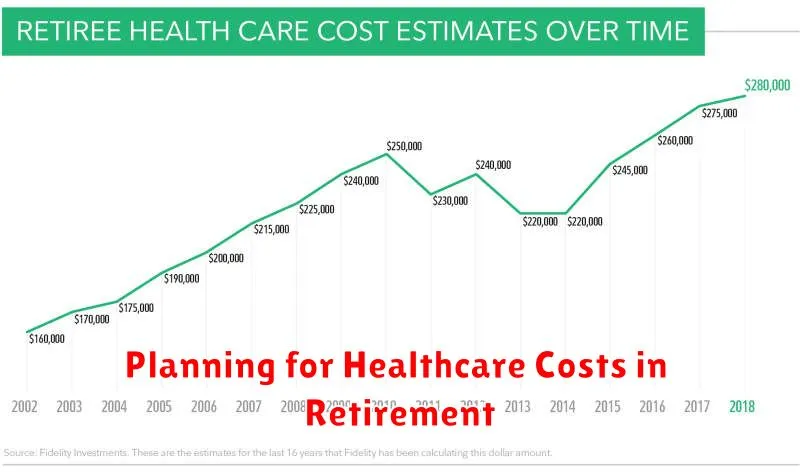

Planning for Healthcare Costs in Retirement

One of the biggest financial concerns for people in their 50s and beyond is how to pay for healthcare costs in retirement. Medical expenses tend to rise as we age, and traditional health insurance often doesn’t cover everything. It’s important to start planning for these costs early, so you can ensure your retirement years are financially secure.

Here are some tips for planning for healthcare costs in retirement:

- Estimate your healthcare expenses. The average retiree spends over $2,000 a year on healthcare, and this number is expected to rise in the future. Using online calculators or working with a financial advisor can help you get a better idea of what your healthcare costs might be.

- Maximize your savings. It’s crucial to have enough money saved to cover these expenses. Consider contributing the maximum amount possible to your 401(k) or IRA. If you have a HSA (Health Savings Account), utilize it for healthcare expenses.

- Explore Medicare options. Once you turn 65, you’ll be eligible for Medicare. There are different plans available, and it’s important to carefully compare them to find the best coverage for your needs. You can also explore supplemental plans like Medigap or Medicare Advantage, which offer additional coverage.

- Consider long-term care insurance. If you’re concerned about needing long-term care in the future, long-term care insurance can help cover these expenses. Be sure to shop around and compare policies before you buy.

- Maintain a healthy lifestyle. This can help you stay healthy and avoid expensive medical bills. Eat a balanced diet, exercise regularly, and get regular checkups with your doctor.

Planning for healthcare costs in retirement may seem daunting, but it’s essential to have a plan in place. By taking these steps, you can help ensure that you have the financial resources you need to enjoy a healthy and comfortable retirement.

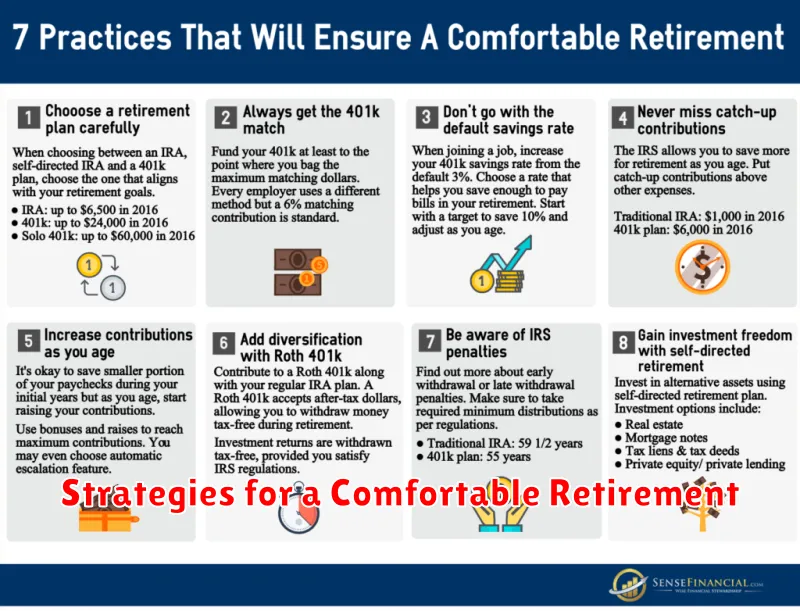

Strategies for a Comfortable Retirement

Retirement may seem like a distant dream when you’re in your 50s, but it’s never too late to start planning for a comfortable and fulfilling retirement. Here are some strategies to help you secure your financial future:

Maximize Your Retirement Contributions: If you haven’t already, contribute the maximum amount allowed to your 401(k) or IRA. If you have the opportunity, consider making catch-up contributions, which allow you to contribute more than the standard limit due to your age. These contributions will grow tax-deferred, potentially leading to substantial savings.

Reduce Debt: High debt payments can significantly impact your retirement savings. Prioritize paying off high-interest debts like credit cards or personal loans. By reducing your debt burden, you’ll have more money available to invest for retirement.

Invest Wisely: Choose a diversified investment portfolio that aligns with your risk tolerance and time horizon. Consult with a financial advisor to create a strategy that balances growth potential with risk management. Don’t be afraid to adjust your investments as you approach retirement to favor more conservative options.

Plan for Healthcare Costs: Healthcare expenses can be a significant factor in retirement. Explore options like a health savings account (HSA) or consider purchasing supplemental insurance to help cover out-of-pocket medical costs.

Consider Part-Time Work: Many people choose to continue working part-time during retirement, either for supplemental income or to stay active. This can help you maintain financial stability and a sense of purpose.

Plan for Your Lifestyle: Think about the lifestyle you want to have in retirement and estimate your expenses. Factor in travel, hobbies, and potential home modifications. By planning ahead, you can ensure your retirement savings are adequate for your desired lifestyle.

Saving for retirement in your 50s and beyond may require some adjustments, but with careful planning and a dedicated approach, you can achieve a comfortable and fulfilling retirement. Remember, it’s never too late to take control of your financial future.

{kind=link}