Feeling overwhelmed by the current economic uncertainty? You’re not alone. With rising inflation, fluctuating markets, and geopolitical instability, it’s more crucial than ever to stay financially prepared. But don’t panic! By adopting proactive strategies, you can navigate these turbulent times with confidence and protect your financial well-being. This guide will equip you with actionable steps to weather the storm and build a robust financial foundation for the future.

From building an emergency fund to diversifying your investments, we’ll delve into practical tips and strategies that can help you achieve financial resilience. Whether you’re a seasoned investor or just starting your financial journey, this article is designed to empower you with the knowledge and tools necessary to navigate the ever-changing economic landscape.

Assess Your Current Financial Situation

Before you can make any changes to your financial plan, it’s essential to have a clear understanding of your current financial situation. This means taking a look at your income, expenses, assets, and debts.

Start by gathering all of your financial documents, including bank statements, credit card statements, investment statements, and tax returns. Once you have all of your documents in one place, you can begin to create a budget.

To create a budget, list all of your monthly income sources and your monthly expenses. Be sure to include all of your fixed expenses, such as rent or mortgage payments, car payments, and insurance premiums, as well as your variable expenses, such as groceries, entertainment, and travel.

Once you have a clear understanding of your income and expenses, you can start to assess your assets and debts. Assets are anything that you own, such as your home, car, investments, and savings accounts. Debts are anything that you owe, such as credit card debt, student loans, and car loans.

After you have assessed your current financial situation, you will be in a better position to make informed decisions about your finances. This information will help you determine what changes you need to make to your budget, whether you need to increase your income, reduce your expenses, or pay down debt.

Build an Emergency Fund

One of the most important steps you can take to weather economic uncertainty is to build an emergency fund. This is a stash of cash that you can tap into when unexpected expenses arise, such as job loss, medical bills, or car repairs. A healthy emergency fund should cover 3 to 6 months of your essential living expenses.

To start building your emergency fund, begin by setting a realistic savings goal. If you’re starting from scratch, even small amounts can make a difference. Automate your savings by setting up regular transfers from your checking account to your savings account. Once you’ve established a foundation, consider increasing your contributions to your emergency fund as your financial situation allows.

Reduce Unnecessary Spending

During times of economic uncertainty, one of the most effective ways to safeguard your finances is to actively reduce unnecessary spending. This might seem daunting, but it can be achieved through a combination of mindful budgeting and adopting a more frugal lifestyle. Start by identifying your spending habits. Track your expenses for a month or two to understand where your money is going. Then, categorize these expenses into needs and wants.

Focus on cutting back on wants. These are things you don’t absolutely need for survival or well-being. This could include dining out frequently, entertainment subscriptions you don’t use, or impulse purchases. Consider alternatives: cooking more meals at home, exploring free or low-cost entertainment options, and using a shopping list to avoid buying items you don’t need.

Beyond reducing spending, consider ways to generate additional income. This could involve taking on a side hustle, selling unused items, or exploring opportunities to earn extra money within your existing skillset.

By actively reducing unnecessary spending and exploring alternative income streams, you can effectively navigate through uncertain economic times and build a stronger financial foundation for the future. Remember, every little saving counts and contributes to your overall financial resilience.

Explore Additional Income Streams

In times of economic uncertainty, it’s crucial to diversify your income sources. Exploring additional income streams can provide a safety net and enhance your financial resilience. Consider these options:

- Freelancing: Leverage your skills and expertise to offer services like writing, editing, web design, or consulting.

- Online Teaching: Share your knowledge and passion by teaching online courses through platforms like Udemy or Skillshare.

- Renting out assets: If you own a spare room, car, or equipment, consider renting it out on platforms like Airbnb or Turo.

- Side hustles: Explore gig economy opportunities such as delivery driving, food delivery, or pet sitting.

- Investing: Consider investing in stocks, bonds, or real estate to generate passive income.

By exploring these options, you can create a more secure financial foundation and navigate economic uncertainty with greater confidence.

Review Your Insurance Coverage

In times of economic uncertainty, it’s more crucial than ever to ensure you have adequate insurance coverage. This helps protect you financially in the face of unexpected events. Reviewing your current insurance policies is a key step in staying financially prepared.

Start by evaluating your needs. Have your circumstances changed since you last reviewed your policies? Have you purchased new assets, like a home or vehicle? Has your family grown? These changes may require adjustments to your insurance coverage.

Next, examine your current coverage. Do you have enough liability insurance to protect yourself in case of an accident? Are your deductibles reasonable? Is your health insurance plan still meeting your healthcare needs?

Don’t be afraid to shop around. Compare quotes from different insurers to ensure you’re getting the best value. And consider adding additional coverage, such as identity theft protection or flood insurance, if needed.

By regularly reviewing and updating your insurance coverage, you can minimize your financial risk and create a stronger safety net for your family during these uncertain times.

Diversify Your Investments

In times of economic uncertainty, it’s crucial to protect your financial well-being. Diversifying your investments is a key strategy that can help mitigate risk and ensure your portfolio remains resilient. By spreading your assets across different asset classes, you reduce your vulnerability to any single market downturn.

Here’s how diversification can benefit you:

- Reduces Risk: By investing in a variety of assets, you lower your exposure to any one particular investment. If one asset class performs poorly, others might compensate, preventing significant losses.

- Improves Returns: Diversification allows you to potentially capture higher returns over the long term. Different asset classes tend to perform differently in various economic conditions, providing opportunities for growth.

- Enhances Stability: A diversified portfolio is more stable during market fluctuations. While individual investments may experience volatility, the overall portfolio is less likely to be severely impacted.

When diversifying your investments, consider allocating your funds across different asset classes, such as:

- Stocks: Represent ownership in companies and can provide potential for growth.

- Bonds: Debt securities that pay regular interest payments and offer a degree of stability.

- Real Estate: Tangible assets that can provide rental income and appreciation potential.

- Commodities: Raw materials like gold, oil, and agricultural products, which can act as a hedge against inflation.

The optimal allocation will depend on your individual circumstances, risk tolerance, and financial goals. Consult with a financial advisor to create a personalized diversification strategy that aligns with your needs.

Stay Informed About Economic Developments

In times of economic uncertainty, staying informed about current events is crucial. By understanding the factors driving economic shifts, you can make more informed financial decisions. This includes keeping abreast of:

- Interest rate changes: Understand how interest rates affect borrowing costs and investment returns.

- Inflation rates: Monitor inflation levels to see how they impact the purchasing power of your money.

- Employment trends: Stay aware of job market conditions, as they can influence consumer spending and overall economic growth.

- Government policies: Be informed about economic policies that could impact your finances, such as tax changes or spending initiatives.

- Global events: Keep up with geopolitical events and their potential economic ramifications.

You can access reliable economic information through reputable sources like:

- Financial news websites: Sites such as Bloomberg, Reuters, and The Wall Street Journal provide in-depth coverage of economic news.

- Government agencies: Websites like the Federal Reserve and the Bureau of Labor Statistics offer data and analysis on economic indicators.

- Economic blogs and podcasts: Numerous blogs and podcasts offer insightful commentary and analysis on current economic trends.

By staying informed about economic developments, you can be better prepared to navigate financial challenges and make informed decisions for your future.

Seek Professional Financial Advice

Navigating uncertain economic times can be daunting, but seeking professional financial advice can provide invaluable support. A financial advisor can offer personalized guidance tailored to your specific circumstances and goals. They can help you develop a robust financial plan, assess your risk tolerance, and make informed decisions regarding investments, savings, and debt management.

Experienced professionals can provide a fresh perspective and identify potential areas for improvement that you might have overlooked. They are well-versed in financial markets, tax laws, and other relevant regulations, ensuring your financial decisions are aligned with your best interests.

Moreover, a financial advisor can serve as a trusted confidant, offering unbiased counsel and emotional support during times of market volatility. They can help you stay focused on your long-term financial goals, even when faced with short-term market fluctuations.

Remember, seeking professional financial advice is an investment in your financial well-being. It empowers you to navigate uncertainty with greater confidence and achieve your financial aspirations.

Create a Realistic Budget and Stick to It

One of the most important things you can do to stay financially prepared during uncertain economic times is to create a realistic budget and stick to it. This means tracking your income and expenses, identifying areas where you can cut back, and creating a plan for how you will spend your money.

Start by listing all of your monthly income, including your salary, any side hustle income, and any other regular payments you receive. Then, list all of your monthly expenses, including your rent or mortgage, utilities, groceries, transportation, and any other recurring costs.

Once you have a clear picture of your income and expenses, you can start to identify areas where you can cut back. This may mean reducing your spending on non-essentials, such as dining out, entertainment, or shopping. You may also want to consider negotiating lower rates for your utilities or finding ways to save money on your grocery bill.

It’s essential to create a budget that you can realistically stick to. If your budget is too restrictive, you are more likely to give up on it. It’s better to start with a budget that feels comfortable and gradually make adjustments as needed.

Using a budget tracker or spreadsheet can be helpful in tracking your spending and ensuring you stay on track.

Negotiate Bills and Expenses

In uncertain economic times, it’s crucial to take control of your finances. One powerful strategy is to negotiate your bills and expenses. You might be surprised at how often companies are willing to work with you, especially if you’re a loyal customer or have been impacted by economic hardship.

Start by contacting your service providers, such as your internet, cable, phone, and utility companies. Explain your situation and see if they offer any discounts or payment plans. Be polite and professional, and keep detailed records of your conversations.

You can also consider renegotiating your loan terms. If you’re struggling to make payments, contact your lender and explore options like a temporary interest rate reduction, payment deferral, or loan modification. Don’t hesitate to ask for help, as lenders are often willing to work with borrowers who are facing financial difficulties.

Finally, don’t be afraid to shop around for better deals on insurance, subscriptions, and other services. Comparing prices and negotiating with different providers can save you a significant amount of money in the long run.

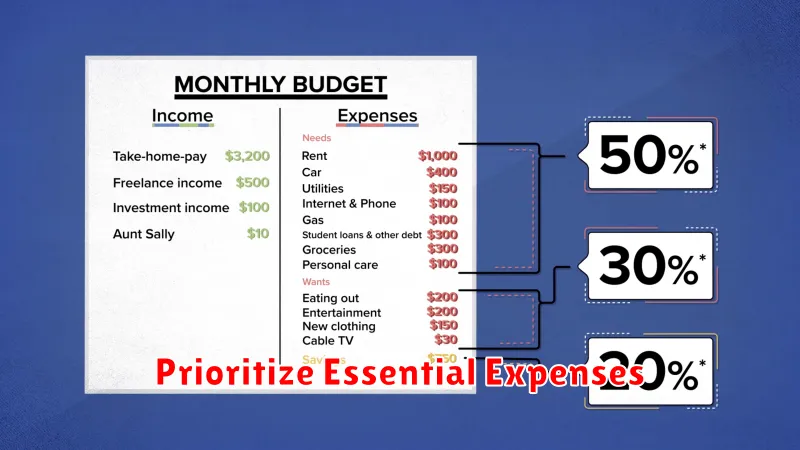

Prioritize Essential Expenses

During uncertain economic times, it’s crucial to prioritize your spending and ensure that essential expenses are covered. These are the expenses that are vital for your survival and well-being, such as housing, utilities, groceries, transportation, and healthcare.

Start by creating a detailed budget, carefully tracking your income and expenses. This will give you a clear picture of where your money is going and identify areas where you can potentially cut back. Prioritize essential expenses over non-essentials like entertainment, dining out, or unnecessary subscriptions.

Consider negotiating with service providers, such as your internet or cable company, to see if you can lower your monthly bills. Also, explore alternative transportation options, like carpooling or public transit, to reduce your fuel costs. Remember, every little bit helps, and by taking proactive steps to manage your expenses, you can maintain your financial stability even during turbulent economic periods.

Consider Downsizing or Relocating

Economic uncertainty can make it difficult to plan for the future. If you are looking to reduce your expenses, consider downsizing your home or relocating to a more affordable area. Downsizing can involve moving to a smaller home, a less expensive neighborhood, or a more rural area. Relocating may mean moving to a new city or state altogether. Both options can significantly reduce your housing costs, which is one of the largest expenses for most people.

When making a decision to downsize or relocate, it is important to consider your personal needs and preferences. Think about the factors that are most important to you, such as your job, family, friends, and lifestyle. Weigh the pros and cons of each option carefully, and make a decision that is best for you and your family.

Downsizing or relocating can be a big decision, but it can also be a great way to improve your financial situation. It can help you save money, reduce stress, and create a more sustainable lifestyle. If you are considering making a move, do your research and get expert advice to make sure you are making the right choice for your circumstances.

Explore Government Assistance Programs

Navigating uncertain economic times can be challenging, but knowing about available resources can provide much-needed relief. The government offers various assistance programs designed to help individuals and families during difficult periods. Exploring these options can provide a safety net and peace of mind.

Unemployment benefits provide financial support to individuals who have lost their jobs through no fault of their own. Eligibility criteria and benefit amounts vary depending on the state, so it’s crucial to research your state’s specific program.

Food assistance programs, such as SNAP (Supplemental Nutrition Assistance Program), provide food benefits to low-income individuals and families. These programs ensure access to nutritious food and can significantly alleviate financial burdens related to groceries.

Housing assistance programs, like Section 8, help low-income families afford safe and decent housing. These programs provide rental subsidies or vouchers to help cover a portion of rent costs.

Healthcare assistance programs, like Medicaid, provide health insurance coverage to low-income individuals and families. Medicaid helps ensure access to essential healthcare services, including preventive care, treatment, and hospitalization.

Energy assistance programs, such as the Low Income Home Energy Assistance Program (LIHEAP), provide financial assistance to low-income households to help pay for heating and cooling costs during the colder months. This can be crucial for maintaining a comfortable and safe living environment.

Researching and understanding these government assistance programs is essential for navigating uncertain economic times. By exploring these options, you can access resources that provide financial support, food security, healthcare, and other critical necessities.

{kind=link}