Are you tired of the rollercoaster ride of the stock market? Do you find the thought of losing your hard-earned savings terrifying? If you answered yes to either of those questions, then you’re not alone. Many people are risk-averse when it comes to investing, and they are looking for safe investment options that can help them grow their wealth without exposing them to unnecessary risk. This article will explore some of the best investment options for risk-averse individuals, providing you with the knowledge and confidence to make informed decisions about your financial future.

From the safety of high-yield savings accounts to the steady returns of real estate, we’ll delve into a variety of investment avenues that cater to those who prioritize stability and security. Our guide will equip you with the understanding to confidently navigate the world of investing, ensuring that your money is working for you in a way that aligns with your personal risk tolerance.

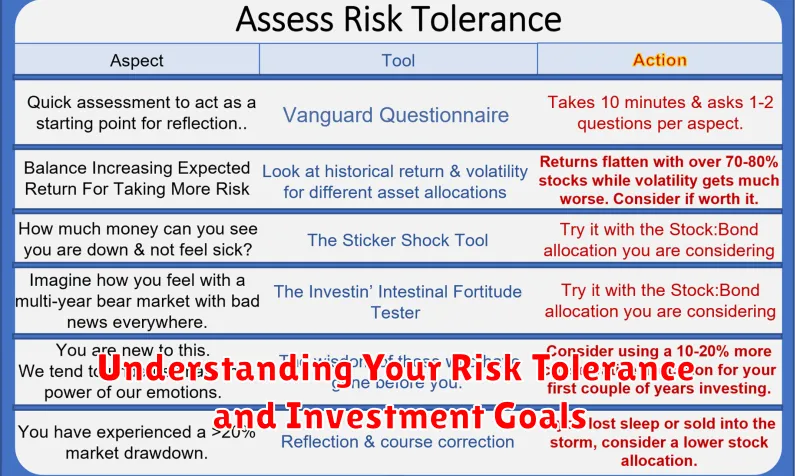

Understanding Your Risk Tolerance and Investment Goals

Before diving into specific investment options, it’s crucial to understand your risk tolerance and investment goals. These two factors are interconnected and play a vital role in shaping your investment strategy.

Risk tolerance refers to your ability and willingness to handle potential losses in your investments. It’s essential to assess how comfortable you are with the possibility of your investments fluctuating in value. If you’re risk-averse, you might prefer investments with lower potential returns but also lower potential losses.

Investment goals, on the other hand, define what you hope to achieve with your investments. These goals could include short-term objectives like saving for a vacation or long-term goals like retirement planning. Understanding your goals helps you determine the appropriate investment horizon and risk level.

For instance, if you’re saving for a vacation in a year, you might choose a low-risk investment like a high-yield savings account. However, if you’re saving for retirement decades from now, you might consider a more diversified portfolio with a mix of stocks and bonds.

By understanding your risk tolerance and investment goals, you can make informed decisions about your investments and choose options that align with your individual needs and priorities.

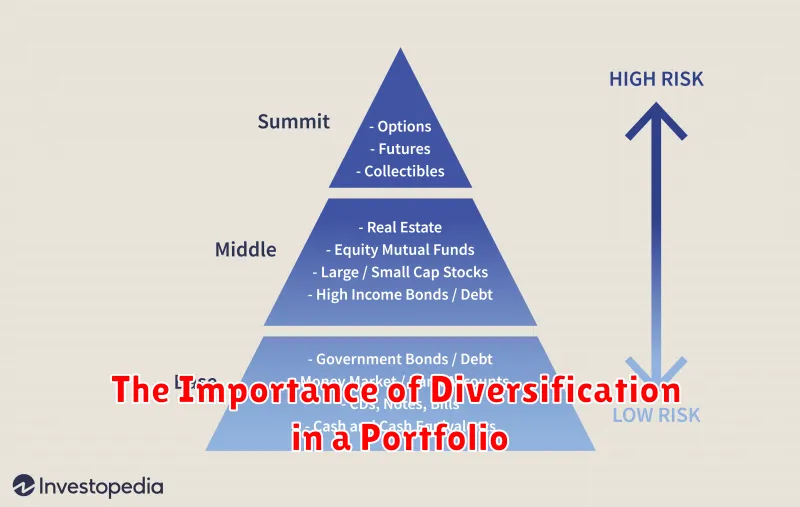

The Importance of Diversification in a Portfolio

Diversification is a crucial aspect of investing, especially for risk-averse individuals. It involves spreading your investments across different asset classes, such as stocks, bonds, real estate, and commodities. This strategy helps mitigate risk by reducing the impact of any single investment’s performance on your overall portfolio.

Imagine putting all your eggs in one basket. If that basket falls, you lose everything. Diversification is like having multiple baskets, so even if one falls, you still have others to rely on. By investing in a variety of assets, you can reduce the volatility of your portfolio and potentially achieve steadier returns over the long term.

Here are some key benefits of diversification for risk-averse investors:

- Reduced risk: By spreading your investments, you lower the chance of significant losses due to the poor performance of any single asset class.

- Improved returns: Diversification can potentially lead to higher returns over time by capturing growth opportunities across different asset classes.

- Peace of mind: Knowing that your portfolio is diversified can provide peace of mind and reduce anxiety about market fluctuations.

Remember, diversification is not a guarantee of success. However, it is a fundamental principle of sound investment strategy, particularly for those seeking to minimize risk.

High-Yield Savings Accounts and Money Market Accounts

For risk-averse investors, high-yield savings accounts (HYSA) and money market accounts (MMA) offer a safe haven for your money. They provide FDIC insurance up to $250,000 per depositor, per insured bank, meaning your principal is protected from loss. These accounts are excellent for emergency funds, short-term savings goals, or simply building a safety net.

High-yield savings accounts are a type of savings account offered by online banks and credit unions that typically pay higher interest rates than traditional brick-and-mortar banks. While interest rates fluctuate, they generally offer a competitive return compared to traditional savings accounts. Money market accounts are similar to HYSA but often come with a few additional features, such as check-writing privileges or debit cards. However, they typically have higher minimum balance requirements and might have transaction limits.

Here’s a breakdown of the advantages and disadvantages:

Advantages of High-Yield Savings Accounts and Money Market Accounts:

- Safety and Security: FDIC insurance protects your principal.

- Liquidity: Your funds are readily accessible.

- Potential for Higher Returns: Compared to traditional savings accounts, you can earn higher interest rates.

Disadvantages of High-Yield Savings Accounts and Money Market Accounts:

- Lower Interest Rates: While higher than traditional savings accounts, they still offer lower returns compared to other investments.

- Limited Investment Options: These accounts are primarily for savings, not for growing your wealth.

Choosing between a HYSA and MMA depends on your individual needs and preferences. If you prioritize accessibility and a higher interest rate, a HYSA is a good option. If you need check-writing privileges or desire additional features, an MMA might be more suitable. Always compare interest rates, fees, and minimum balance requirements before making a decision.

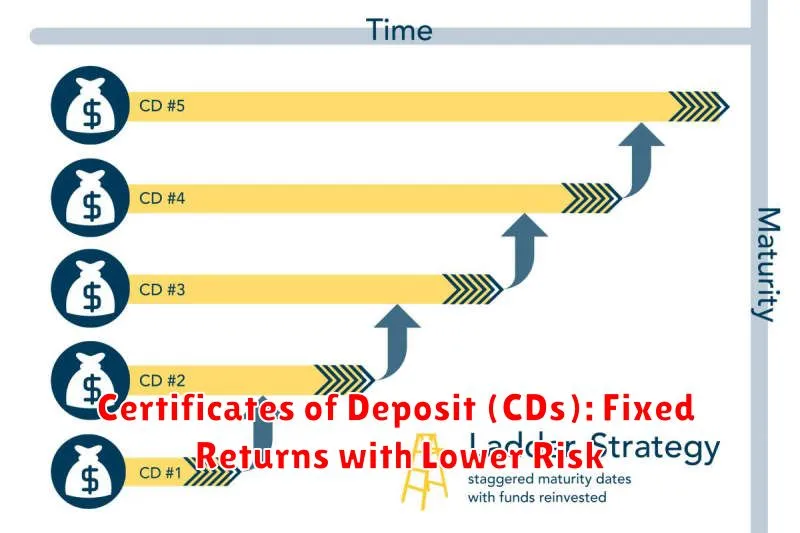

Certificates of Deposit (CDs): Fixed Returns with Lower Risk

For risk-averse individuals seeking a steady stream of income, Certificates of Deposit (CDs) present a secure investment option. CDs offer a fixed interest rate for a set period, ensuring a predictable return on your investment. Unlike stocks or bonds, which fluctuate in value, CDs offer greater stability and minimal risk. This makes them an ideal choice for individuals who prioritize capital preservation over potentially high returns.

When you invest in a CD, you commit to keeping your money deposited for a specified duration, typically ranging from a few months to several years. In return for this commitment, the financial institution guarantees a fixed interest rate, ensuring a predictable return on your investment. This predictable income stream makes CDs a valuable tool for individuals seeking a stable source of funds.

However, it’s crucial to understand the trade-offs involved. CDs generally offer lower interest rates compared to riskier investments like stocks. Additionally, withdrawing your funds before maturity might incur penalties. Nevertheless, for those who prioritize security and predictable returns, CDs can be a valuable investment tool.

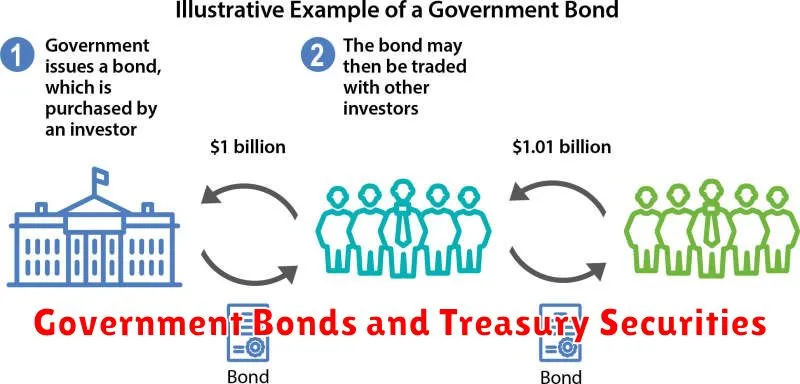

Government Bonds and Treasury Securities

For risk-averse individuals seeking a safe haven for their investments, government bonds and Treasury securities present compelling options. These instruments offer a relatively low risk profile, as they are backed by the full faith and credit of the issuing government. In essence, you’re lending money to the government with the assurance of repayment, making them a popular choice for those seeking capital preservation and steady income streams.

Treasury securities are issued by the U.S. government and are considered the gold standard in terms of safety and liquidity. They come in various maturities, ranging from short-term Treasury bills (T-bills) to long-term Treasury bonds. The longer the maturity, the higher the potential return but also the greater the interest rate risk (the risk that interest rates will rise, decreasing the value of your bond).

Government bonds issued by other countries can also provide diversification and exposure to different economies. However, it’s crucial to consider the creditworthiness of the issuing government. Bonds from countries with strong economic fundamentals and a history of fiscal responsibility tend to carry lower risk and offer competitive yields.

Investing in government bonds and Treasury securities offers several benefits, including:

- Low risk: Backed by the government, they are considered among the safest investments available.

- Steady income: They generate regular interest payments, providing a predictable income stream.

- Liquidity: Many government bonds are highly liquid, meaning they can be easily bought and sold on the secondary market.

- Inflation protection: Some bonds offer inflation protection, such as Treasury Inflation-Protected Securities (TIPS).

While government bonds and Treasury securities offer a safe harbor for investments, it’s important to consider their limitations. Their returns tend to be lower than those of riskier assets like stocks, and their value can fluctuate with interest rate changes.

In conclusion, for risk-averse investors seeking a stable and secure investment, government bonds and Treasury securities provide a solid foundation for their portfolio. However, careful consideration of maturity, interest rate risk, and creditworthiness is essential before making any investment decisions.

Low-Volatility Stocks and Dividend-Paying Companies

For risk-averse investors, low-volatility stocks and dividend-paying companies offer attractive investment options. These investments prioritize stability and income generation over aggressive growth, aligning with the goals of individuals seeking to minimize risk.

Low-volatility stocks exhibit relatively smaller price fluctuations compared to the broader market. Their consistent performance, characterized by lower beta values, provides a sense of security and predictability, especially during periods of market turmoil. These stocks often represent established companies with mature business models and a history of steady earnings.

Dividend-paying companies provide a regular stream of income to investors, further reducing reliance on volatile capital gains. Dividends offer a source of cash flow, allowing investors to enjoy a tangible return on their investment while potentially increasing the overall value of their portfolio. Companies with a consistent history of dividend payments are often viewed as financially sound and committed to shareholder value.

Investing in a combination of low-volatility stocks and dividend-paying companies can create a diversified portfolio that balances potential growth with risk mitigation. These investments can provide a sense of security and a steady stream of income, making them ideal options for risk-averse individuals.

Annuities: Providing Guaranteed Income Streams

For risk-averse individuals seeking a reliable source of income, annuities offer a compelling solution. Annuities are insurance contracts that provide a guaranteed stream of payments for a specific period, either for a fixed term or for the rest of your life.

Annuities act as a safe haven for your savings, protecting them from market fluctuations and ensuring a consistent income stream. They can be particularly beneficial for retirees, allowing them to live comfortably without worrying about outliving their savings.

There are different types of annuities, each with its own features and benefits. Some popular types include:

- Fixed annuities offer a guaranteed interest rate, providing predictable income payments.

- Variable annuities allow you to invest your money in a range of sub-accounts, offering potential growth but also carrying some risk.

- Indexed annuities tie their returns to the performance of a specific market index, providing a balance between security and potential growth.

Annuities are not without drawbacks. They may have high fees or require a significant upfront investment. However, for those seeking a guaranteed income stream and a secure financial future, annuities can be a valuable investment option.

Working with a Financial Advisor to Create a Customized Plan

A financial advisor can play a crucial role in helping risk-averse individuals create a tailored investment plan. They possess the expertise and experience to assess your financial situation, goals, and risk tolerance. By understanding your individual needs, they can recommend a diverse portfolio that aligns with your risk appetite and helps you achieve your financial objectives.

Financial advisors provide valuable guidance in navigating the complexities of the investment world. They can help you understand different asset classes, investment strategies, and market trends. Their insights can help you make informed decisions about where to allocate your investments and how to manage your portfolio effectively.

Working with a financial advisor offers several benefits for risk-averse individuals:

- Personalized Investment Plan: An advisor will develop a plan that is specifically tailored to your circumstances, goals, and risk tolerance.

- Professional Guidance: They provide expert advice and support throughout your investment journey, helping you make informed decisions and avoid common pitfalls.

- Objectivity and Emotional Detachment: Financial advisors can offer an objective perspective, separating emotions from investment decisions, which is crucial in volatile markets.

- Long-Term Perspective: They focus on achieving your long-term financial goals and help you stay disciplined even during market fluctuations.

When choosing a financial advisor, it’s essential to consider their experience, qualifications, and approach. Look for someone who understands your risk tolerance, financial goals, and investment preferences. Remember to ask questions and clarify any uncertainties before making a decision.

{kind=link}