Are you concerned about your credit utilization and its impact on your financial health? You’re not alone! Many people struggle to understand how much credit they can use before it negatively impacts their credit score. In today’s world, having good credit is essential for everything from securing a loan to getting approved for an apartment. Understanding how your credit utilization affects your financial health can help you make informed decisions about your finances and build a strong credit foundation.

Credit utilization refers to the percentage of your available credit that you’re currently using. It’s a crucial factor considered by lenders when assessing your creditworthiness. High credit utilization can significantly harm your credit score and make it more difficult to obtain loans, credit cards, or even a mortgage. This article delves into the impact of credit utilization on your financial health, providing you with valuable insights to improve your credit standing and secure a brighter financial future.

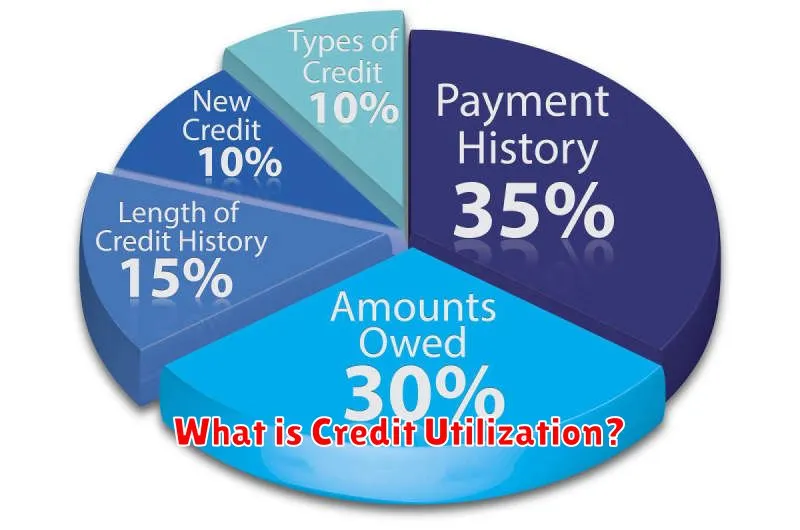

What is Credit Utilization?

Credit utilization is a crucial metric in assessing your financial health and it reflects the portion of your available credit that you are currently using. It is calculated by dividing your total credit card debt by your total credit limit. For example, if your total credit limit is $10,000 and you have $2,000 in outstanding debt, your credit utilization ratio is 20% ($2,000 / $10,000 = 20%).

Credit utilization plays a significant role in your credit score, which is a numerical representation of your creditworthiness. Creditors closely examine your credit utilization ratio to gauge your ability to manage debt responsibly. A high credit utilization ratio indicates that you are heavily reliant on credit, potentially posing a risk to lenders.

A low credit utilization ratio, typically below 30%, is generally considered favorable and can positively impact your credit score. On the other hand, a high credit utilization ratio, exceeding 30%, can negatively affect your score and make it more difficult to secure loans or credit cards with favorable terms.

How Credit Utilization is Calculated

Credit utilization ratio is a key factor in your credit score. It’s calculated by dividing the amount of credit you’re currently using by your total available credit. For example, if you have a credit card with a $1,000 limit and a balance of $500, your credit utilization ratio is 50%.

The formula for calculating credit utilization ratio is: Credit Utilization Ratio = (Total Credit Card Balance / Total Credit Limit) x 100

The lower your credit utilization ratio, the better. Ideally, you should aim for a credit utilization ratio of 30% or less. A higher credit utilization ratio can negatively impact your credit score, as it can signal to lenders that you are carrying too much debt.

It is important to note that credit utilization ratio is only one of many factors that contribute to your credit score. Other factors include your payment history, length of credit history, and the mix of credit you have.

To improve your credit utilization ratio, you can make sure you pay your credit card bills on time and in full each month. You can also try to keep your credit card balances low, or even pay them down to zero.

The Relationship Between Credit Utilization and Credit Scores

Credit utilization is one of the most important factors that affect your credit score. It represents the amount of credit you’re currently using compared to your total available credit. Your credit utilization ratio is calculated by dividing your total credit card balances by your total credit limits.

For example, if you have a total credit limit of $10,000 and you’re carrying a balance of $2,000, your credit utilization ratio is 20%. A lower credit utilization ratio is generally better for your credit score.

Credit bureaus like Experian, Equifax, and TransUnion use credit utilization as a key factor when calculating your FICO score. A high utilization ratio can signal to lenders that you’re carrying a lot of debt and may be a riskier borrower. On the other hand, a low utilization ratio shows that you’re managing your credit responsibly.

The ideal credit utilization ratio is generally considered to be below 30%, but it’s best to keep it below 10% for optimal credit health.

The Negative Effects of High Credit Utilization

Credit utilization is a significant factor in determining your credit score. It is calculated by dividing your total outstanding credit card debt by your total available credit limit. A high credit utilization ratio can have detrimental effects on your financial health.

One major negative effect is a lower credit score. Creditors view a high utilization ratio as a sign of financial instability and risk. This can lead to higher interest rates on loans and credit cards, making it more expensive to borrow money.

Another consequence of high credit utilization is reduced credit availability. Lenders may be less willing to extend credit to individuals with high utilization ratios, making it challenging to secure loans for major purchases like a car or home.

High credit utilization can also result in increased risk of overspending. When you have a high credit utilization ratio, you may be tempted to use more credit, leading to a cycle of debt and financial stress.

To mitigate the negative effects of high credit utilization, it’s important to keep your utilization ratio below 30%. This can be achieved by making regular payments on your credit cards and avoiding unnecessary purchases. Additionally, you can consider requesting a credit limit increase to lower your utilization ratio. By taking these steps, you can improve your credit score and overall financial health.

The Benefits of Maintaining Low Credit Utilization

Credit utilization is the amount of credit you’re using compared to your total available credit. It’s a critical factor in your credit score, and maintaining a low credit utilization ratio can significantly benefit your financial health.

One of the biggest advantages of low credit utilization is that it can boost your credit score. Credit scoring models consider credit utilization as a significant factor, and a lower ratio generally results in a higher credit score. This, in turn, can lead to lower interest rates on loans, credit cards, and mortgages, saving you money over the long term.

Moreover, a low credit utilization ratio can improve your chances of getting approved for new credit. Lenders often use credit utilization as a gauge of your financial responsibility. A lower ratio signals to lenders that you’re a responsible borrower, increasing your likelihood of approval for loans, credit cards, and other forms of credit.

Beyond credit scores and loan approvals, maintaining low credit utilization can help you avoid overspending. By keeping your credit utilization low, you’re less likely to max out your credit cards or take on more debt than you can manage. This can help you stay within your budget and avoid the potential for financial strain.

In summary, keeping your credit utilization low is a crucial step towards a healthier financial future. It can boost your credit score, improve your chances of getting approved for credit, and help you avoid overspending. By making a conscious effort to maintain a low credit utilization ratio, you’re putting yourself in a better position to achieve your financial goals.

Strategies for Lowering Your Credit Utilization Rate

Credit utilization is a critical factor in determining your credit score. It represents the percentage of your available credit you are using. A high credit utilization rate can negatively impact your credit score and make it more difficult to secure loans or credit cards at favorable terms. Fortunately, there are several effective strategies you can employ to lower your credit utilization rate and improve your financial health.

1. Pay Down Your Balances: The most straightforward approach to reducing credit utilization is to pay down your outstanding balances on credit cards and other revolving accounts. Aim to pay more than the minimum payment each month, or even make multiple payments throughout the month if possible. This will quickly decrease your balances and lower your utilization rate.

2. Increase Your Credit Limits: Another way to lower your credit utilization rate is to increase your credit limits. This can be achieved by requesting a credit limit increase from your existing credit card providers. However, be mindful that increasing your credit limit doesn’t automatically improve your credit score. It only lowers your utilization rate if you maintain your current spending habits.

3. Use a Balance Transfer Card: Balance transfer cards offer a temporary period of 0% interest on transferred balances. This can be a useful strategy to lower your credit utilization if you have high-interest debt. However, it’s important to remember that these offers typically have a limited time frame, and you’ll eventually be responsible for paying interest on the transferred balance.

4. Avoid Opening New Credit Accounts: Opening new credit accounts can temporarily lower your credit score and increase your credit utilization rate. This is because inquiries from new applications can harm your score, and new accounts increase your available credit, thus potentially lowering your utilization rate. It’s generally advisable to avoid opening new credit accounts unless absolutely necessary.

5. Shop Around for Lower Interest Rates: If you have credit card debt with high interest rates, consider transferring your balances to a card with a lower interest rate. This can significantly reduce your monthly payments and help you pay down your debt faster, leading to a lower credit utilization rate.

Monitoring Your Credit Report for Accuracy

Your credit report is a vital document that reflects your financial history. It plays a crucial role in determining your creditworthiness and can impact your ability to secure loans, mortgages, and even employment. Therefore, it is essential to ensure the accuracy of your credit report. Errors in your report can negatively affect your credit score and lead to higher interest rates, making it more expensive to borrow money.

To monitor your credit report for accuracy, follow these steps:

- Obtain Your Credit Report: You are entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year. You can request your reports through the Annual Credit Report website (https://www.annualcreditreport.com/).

- Review Your Report Thoroughly: Carefully examine each section of your report, including your personal information, account details, and any negative items like late payments or collections. Look for any inaccuracies, such as incorrect account balances, disputed charges, or accounts that shouldn’t be listed.

- Dispute Errors: If you find any errors, promptly dispute them with the credit bureau through their website or by sending a letter. Include supporting documentation, such as receipts or payment history, to support your claim.

- Monitor for Changes: After disputing an error, follow up regularly to ensure the correction has been made. You should also continue to monitor your report for any new errors or changes that may occur.

By taking these steps to monitor your credit report for accuracy, you can protect your financial well-being and ensure that you have a clear and accurate representation of your credit history.

Building Healthy Credit Habits for the Long Term

Credit utilization is a crucial aspect of your financial health, and building healthy credit habits can have a long-lasting positive impact on your financial well-being. A healthy credit utilization ratio, generally considered to be below 30%, demonstrates responsible credit management and can benefit you in several ways.

Firstly, it can help you secure better interest rates on loans. Lenders view individuals with low credit utilization as less risky borrowers, which translates to more favorable interest rates on mortgages, auto loans, and personal loans. This can save you a significant amount of money over the long term.

Secondly, establishing good credit habits can lead to higher credit limits. As you consistently demonstrate responsible credit use, lenders may increase your available credit, giving you greater flexibility and financial buffer.

Lastly, healthy credit habits can improve your credit score. Your credit score is a numerical representation of your creditworthiness, and a higher score unlocks various advantages, including access to better loan terms, lower insurance premiums, and even better job opportunities.

Building healthy credit habits requires a conscious effort. Start by setting realistic spending goals and tracking your expenses diligently. Make sure to pay your bills on time and strive to keep your credit utilization ratio below 30%. By establishing these habits, you can set yourself up for a brighter financial future.

{kind=link}