In today’s rapidly evolving economic landscape, financial literacy is no longer a mere suggestion but an essential life skill. With the rise of complex financial products, technological advancements, and global economic uncertainties, it’s more crucial than ever to understand the intricacies of managing your finances. Financial literacy empowers individuals to make informed decisions about their money, build a secure future, and navigate the challenges of a dynamic economy. It goes beyond simply knowing how to balance a checkbook; it encompasses a wide range of skills, from budgeting and investing to understanding debt and credit.

From the young adult entering the workforce to seasoned professionals seeking financial independence, financial literacy is a universal necessity. It equips individuals with the knowledge and tools to make sound financial choices, achieve their financial goals, and contribute to a more financially resilient society. Whether you’re saving for a down payment on a home, planning for retirement, or simply managing your day-to-day expenses, understanding the fundamentals of personal finance is paramount to success in today’s economic climate.

What is Financial Literacy?

Financial literacy is the ability to understand and manage your finances effectively. This includes knowledge and skills in areas like budgeting, saving, investing, borrowing, and managing debt. Financial literacy empowers individuals to make informed decisions about their money, enabling them to achieve their financial goals.

It encompasses a broad range of concepts, including:

- Understanding basic financial concepts like interest rates, inflation, and compound interest

- Creating and sticking to a budget

- Saving money for short-term and long-term goals

- Managing credit and debt responsibly

- Investing wisely for the future

- Understanding insurance and retirement planning

In essence, financial literacy equips individuals with the tools and knowledge necessary to navigate the complexities of the modern financial landscape. It is a crucial skill for everyone, regardless of their age, income, or background.

Key Components of Financial Literacy

Financial literacy encompasses a broad range of skills and knowledge that empower individuals to make informed financial decisions. While the scope of financial literacy can be vast, there are several key components that form its foundation. These components are essential for navigating the complexities of personal finance and achieving financial well-being.

One of the most fundamental components is budgeting. This involves tracking income and expenses, identifying areas for savings, and creating a plan for allocating funds. A well-crafted budget provides a clear picture of financial inflows and outflows, enabling individuals to prioritize spending and make informed decisions about their financial resources.

Understanding the concept of saving and investing is another critical aspect of financial literacy. Saving allows individuals to accumulate funds for future goals, such as retirement, education, or a down payment on a house. Investing, on the other hand, involves using saved money to potentially grow wealth over time through various financial instruments, such as stocks, bonds, and real estate.

Debt management is a crucial element of financial literacy, as excessive debt can have a significant negative impact on an individual’s financial well-being. Understanding different types of debt, such as credit card debt, student loans, and mortgages, is essential for making responsible borrowing decisions and developing strategies for managing debt effectively.

Financial planning involves setting long-term financial goals and developing strategies to achieve them. This component requires considering factors such as retirement planning, estate planning, and insurance needs. A comprehensive financial plan provides a roadmap for navigating financial decisions throughout different stages of life.

In today’s complex economic landscape, financial literacy is no longer an optional skill; it is a necessity for individuals to thrive and achieve financial security. Understanding the key components of financial literacy empowers individuals to make informed financial decisions, manage their finances effectively, and build a brighter future.

Why is Financial Literacy Important in Today’s Economy?

In today’s rapidly evolving economic landscape, financial literacy is paramount for individuals and families to navigate the complex world of money management. It empowers individuals to make informed decisions regarding their finances, ensuring they have the knowledge and skills to achieve their financial goals.

Financial literacy equips individuals with the ability to understand financial concepts such as budgeting, saving, investing, debt management, and credit. This knowledge empowers them to make informed choices that can positively impact their long-term financial well-being.

Furthermore, financial literacy is crucial for navigating the complexities of the modern economy. With the rise of new financial products and technologies, individuals need to possess the skills to understand and utilize these tools effectively. This includes understanding the risks and rewards associated with different investment options, as well as the importance of diversifying one’s portfolio.

In a world where financial stability is essential, financial literacy plays a critical role in fostering economic empowerment. Individuals with strong financial literacy skills are better equipped to make sound financial decisions, reducing their vulnerability to financial hardship and contributing to a more resilient and prosperous society.

The Impact of Low Financial Literacy

Low financial literacy can have a significant impact on individuals, families, and even the overall economy. When people lack the knowledge and skills to manage their finances effectively, they are more likely to make poor financial decisions that can lead to a range of negative consequences.

One of the most immediate impacts of low financial literacy is debt. Individuals who lack financial knowledge may struggle to understand interest rates, credit scores, and the long-term implications of borrowing. This can lead to taking on excessive debt, which can become overwhelming and difficult to manage. High levels of debt can put a strain on household budgets, limiting opportunities for saving and investment.

Low financial literacy can also contribute to financial instability. Without a strong understanding of financial concepts, individuals may be more vulnerable to scams, predatory lending, and other financial risks. They may also struggle to plan for the future, making it difficult to save for retirement, education, or unexpected expenses. This can lead to financial hardship and instability, particularly during times of economic uncertainty.

On a larger scale, low financial literacy can have a negative impact on the overall economy. When individuals make poor financial decisions, it can contribute to economic instability and slower economic growth. This is because individuals with limited financial knowledge may be less likely to invest, save, or participate in the economy in a productive manner.

Benefits of Being Financially Literate

Financial literacy is the ability to understand and manage your finances effectively. It’s a crucial skill in today’s economy, and it can lead to numerous benefits for individuals and families.

One of the most significant benefits of financial literacy is the ability to make informed financial decisions. Understanding your financial situation, including your income, expenses, and debts, empowers you to make choices that align with your financial goals.

Financial literacy also allows you to avoid financial pitfalls. By being aware of common scams, predatory lending practices, and other financial risks, you can protect yourself from potential losses.

Another benefit is the ability to achieve your financial goals. Whether you’re saving for retirement, buying a home, or starting a business, financial literacy provides the knowledge and skills necessary to plan and reach your objectives.

Financial literacy can also lead to improved financial well-being. By managing your finances effectively, you can reduce stress, increase your peace of mind, and enjoy a higher quality of life.

In today’s economic landscape, where financial products and services are constantly evolving, financial literacy is essential for navigating the complexities of personal finance. It empowers you to make informed decisions, protect your financial interests, and achieve your financial goals.

Financial Literacy and Decision-Making: Budgeting, Saving, Investing

Financial literacy is essential for making sound financial decisions. This encompasses understanding budgeting, saving, and investing, which are vital for individuals to navigate today’s complex economy.

Budgeting involves planning how to spend and save money. It requires tracking income and expenses to identify areas for improvement and develop a spending plan. Effective budgeting helps individuals prioritize needs, manage debt, and reach their financial goals.

Saving refers to setting aside money for future needs. It plays a crucial role in financial security, enabling individuals to manage unexpected expenses, invest for the long term, and reach their financial goals. Saving strategies involve setting realistic goals, choosing appropriate savings vehicles, and staying consistent with contributions.

Investing refers to allocating funds for potential growth over time. It allows individuals to build wealth and create a secure financial future. Investing can take various forms, including stocks, bonds, real estate, and mutual funds. Understanding the risks and rewards associated with different investment options is crucial for making informed decisions.

Financial Literacy and Debt Management

In today’s complex economic landscape, financial literacy has become paramount for individuals to navigate the challenges of debt management effectively. A strong understanding of financial concepts empowers individuals to make informed decisions regarding borrowing, spending, and saving, ultimately leading to improved financial well-being.

Financial literacy equips individuals with the knowledge and skills necessary to manage their finances responsibly. This includes understanding the different types of debt, interest rates, and repayment options. With this knowledge, individuals can make informed decisions about when and how much to borrow, ensuring they can manage their debt obligations without overwhelming their financial stability.

A crucial aspect of financial literacy is budgeting, which allows individuals to track their income and expenses effectively. By creating a realistic budget, individuals can identify areas where they can cut back on spending and prioritize debt repayment. This disciplined approach to managing finances helps minimize the accumulation of debt and facilitates timely repayment.

Moreover, financial literacy emphasizes the importance of building a positive credit score. A good credit score unlocks lower interest rates on loans, making it easier for individuals to manage debt effectively. Understanding the factors that influence credit score, such as payment history and credit utilization, empowers individuals to take proactive steps to improve their creditworthiness.

In conclusion, financial literacy plays a vital role in effective debt management. By fostering a deep understanding of financial concepts, budgeting, and credit management, individuals can make informed decisions, avoid excessive debt accumulation, and achieve financial stability in today’s complex economic environment.

The Role of Financial Education

Financial education plays a crucial role in empowering individuals to make informed financial decisions and navigate the complexities of the modern economy. It equips people with the knowledge and skills necessary to manage their money effectively, achieve their financial goals, and build a secure future.

Financial education encompasses a wide range of topics, including budgeting, saving, investing, debt management, and financial planning. It teaches individuals how to:

- Create and stick to a budget

- Set financial goals and develop strategies to achieve them

- Understand different investment options and their associated risks

- Manage debt responsibly and avoid financial pitfalls

- Plan for retirement and other long-term financial needs

By providing individuals with this essential knowledge, financial education fosters financial well-being and helps individuals make sound financial decisions that lead to improved economic outcomes. This, in turn, contributes to a more stable and prosperous society.

Resources for Improving Financial Literacy

In today’s complex economic landscape, being financially literate is more important than ever. Luckily, there are numerous resources available to help you improve your financial knowledge and skills. Here are a few key resources to get you started:

Government websites: The Consumer Financial Protection Bureau (CFPB) provides a wealth of information on consumer finance topics, including credit, debt, and mortgages. The U.S. Securities and Exchange Commission (SEC) offers resources on investing, saving, and retirement planning. These websites provide valuable information and tools to help you make informed financial decisions.

Non-profit organizations: Organizations like the National Endowment for Financial Education (NEFE) and the JumpStart Coalition for Personal Financial Literacy offer educational programs and resources to help individuals of all ages improve their financial literacy. They provide free online courses, workshops, and publications covering various financial topics.

Online learning platforms: Several websites and apps offer interactive courses and resources to enhance your financial knowledge. Platforms like Khan Academy, Coursera, and edX provide free or affordable courses on personal finance, investing, and entrepreneurship. These platforms offer flexible learning options, allowing you to learn at your own pace and convenience.

Financial advisors and counselors: If you need personalized guidance and support, consider consulting with a financial advisor or counselor. They can help you develop a financial plan, manage your debt, and make investment decisions based on your individual circumstances. However, it is crucial to choose a reputable and qualified professional.

Financial literacy programs: Many schools, libraries, and community centers offer financial literacy programs for individuals and families. These programs often cover topics like budgeting, saving, investing, and credit management. They can provide practical skills and knowledge to help you achieve your financial goals.

By taking advantage of these resources, you can empower yourself with the financial knowledge and skills to navigate today’s economic challenges and build a secure financial future. Remember, financial literacy is a lifelong journey, so continue seeking out resources and opportunities to enhance your financial well-being.

Financial Literacy for Different Age Groups

Financial literacy is crucial at all ages. The path to financial well-being starts early and continues throughout life, requiring different skills and knowledge at each stage. Here’s a breakdown of financial literacy for different age groups:

Children and Teenagers (Ages 5-18)

This is the foundation stage for financial literacy. Parents and educators play a vital role in teaching basic financial concepts like saving, spending, and budgeting. It’s essential to make financial education engaging and age-appropriate. Board games, piggy banks, and allowance systems can help them understand the value of money and make informed choices.

Young Adults (Ages 18-25)

This age group is often navigating independent life for the first time. Financial literacy focuses on managing finances independently, learning about budgeting, saving for future goals, managing credit, and understanding student loan debt. This is also a crucial time to start building a good credit score.

Adults (Ages 25-65)

This stage emphasizes long-term financial planning. Financial literacy for adults includes investing, retirement planning, managing mortgages, and potentially starting a family. Understanding insurance, estate planning, and tax implications is also vital.

Seniors (Ages 65+)

Seniors need to focus on managing their retirement funds, healthcare expenses, and potential long-term care needs. Financial literacy for this age group involves understanding Social Security benefits, estate planning, and potentially reverse mortgages. They also need to be aware of scams and protect themselves from financial exploitation.

Financial literacy is an ongoing process that requires continuous learning and adaptation. Regardless of age, staying informed and making proactive financial decisions is crucial to achieving long-term financial security.

Financial Literacy in the Digital Age

The digital age has brought about a dramatic transformation in the way we manage our finances. With online banking, mobile payments, and investment platforms readily accessible, navigating the financial landscape has become more complex than ever before. This is where financial literacy takes center stage, playing a crucial role in empowering individuals to make informed financial decisions in this rapidly evolving digital world.

Understanding the intricacies of online banking security, the potential pitfalls of digital financial products, and the nuances of online investing are essential for thriving in the digital economy. Financial literacy equips individuals with the knowledge and skills to navigate these complexities, ensuring that their financial well-being is not compromised in the digital age.

From discerning legitimate financial advice amidst a barrage of online information to understanding the implications of digital currencies, financial literacy is a vital shield against financial scams and misleading marketing tactics. By equipping individuals with the ability to evaluate financial products and services critically, financial literacy promotes responsible financial decision-making in the digital age.

Moreover, financial literacy in the digital age transcends mere knowledge. It encompasses the ability to adapt to new technologies, stay updated on financial trends, and embrace emerging financial tools. This includes understanding the impact of artificial intelligence on financial services, the rise of fintech solutions, and the evolving regulatory landscape of digital finance.

In conclusion, financial literacy is not just a necessity but a cornerstone of financial well-being in the digital age. It empowers individuals to navigate the complexities of the digital financial landscape, make informed decisions, and secure their financial future in a world increasingly dominated by technology. By embracing financial literacy, individuals can seize the opportunities and mitigate the risks presented by the digital economy.

The Importance of Financial Literacy for Young Adults

Financial literacy is essential for young adults as they navigate the complexities of today’s economy. With the rising cost of living, student loan debt, and the ever-evolving financial landscape, having a strong understanding of personal finance is crucial for achieving financial stability and independence.

Managing Finances: Financial literacy equips young adults with the skills to budget effectively, track expenses, and save for future goals. It helps them make informed decisions about spending, saving, and investing, empowering them to control their financial well-being.

Avoiding Debt Traps: Understanding the risks and consequences of debt is crucial. Financial literacy teaches young adults about different types of debt, how to manage it responsibly, and how to avoid falling into debt traps that can hinder their financial progress.

Building a Secure Future: Financial literacy empowers young adults to plan for their future by setting financial goals, investing wisely, and making informed decisions regarding retirement planning and asset accumulation. This lays the foundation for a financially secure future.

Empowering Financial Independence: Financial literacy empowers young adults to take control of their finances, making them less dependent on others for financial assistance. It fosters a sense of responsibility and confidence in managing their money.

In conclusion, financial literacy is of paramount importance for young adults in today’s economy. It equips them with the skills and knowledge to manage their finances effectively, avoid debt traps, build a secure future, and achieve financial independence.

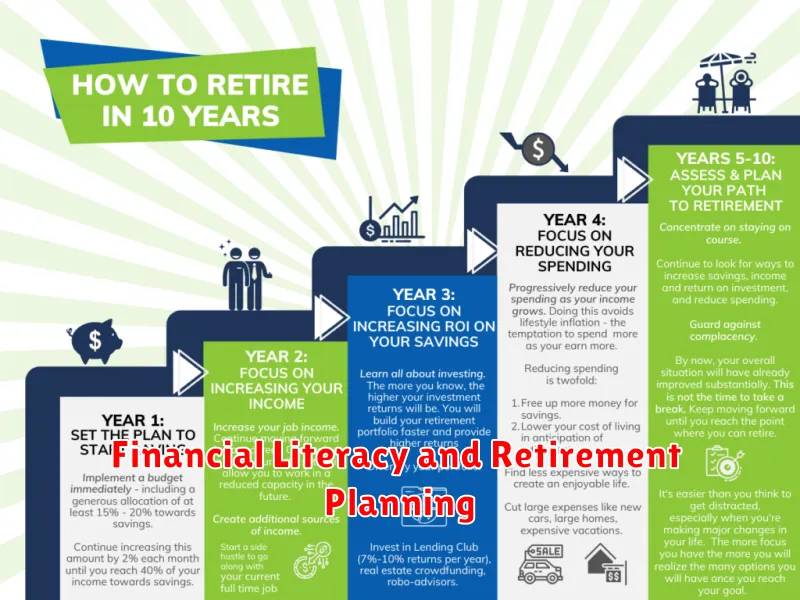

Financial Literacy and Retirement Planning

Financial literacy is essential for a secure retirement. By understanding the basics of budgeting, saving, and investing, individuals can take control of their financial future and plan for a comfortable retirement. Financial literacy empowers individuals to make informed decisions about their finances, ensuring they can meet their retirement goals.

Retirement planning involves setting financial goals, creating a budget, and choosing the right investment strategies. Financial literacy equips individuals with the skills to navigate the complex world of retirement planning, from choosing the right retirement savings accounts to understanding the different investment options available.

By prioritizing financial literacy, individuals can increase their chances of achieving a fulfilling and financially secure retirement. They can make informed decisions about their savings, investments, and retirement planning strategies, setting themselves up for a comfortable and enjoyable post-retirement life.

Financial Literacy and Economic Growth

Financial literacy plays a pivotal role in driving economic growth. When individuals possess a strong understanding of financial concepts, they make informed decisions about saving, investing, and managing debt, leading to increased financial stability and prosperity. This, in turn, stimulates economic activity through various channels.

Firstly, financial literacy empowers individuals to save effectively. By understanding the importance of saving, people can allocate a portion of their income for future needs, such as retirement, education, or unexpected expenses. This leads to increased personal wealth and reduced reliance on borrowing, boosting overall household financial security.

Secondly, financial literacy promotes responsible borrowing and debt management. Individuals equipped with financial knowledge are more likely to understand the implications of taking on debt, such as interest rates and repayment terms. This enables them to make informed decisions about borrowing, avoiding excessive debt and its detrimental impact on their financial well-being.

Thirdly, financial literacy encourages investment. By understanding different investment options, risks, and returns, individuals can allocate their savings effectively, contributing to the growth of the economy. Investment in financial markets, real estate, or businesses fuels economic expansion by generating new jobs, stimulating innovation, and driving overall productivity.

In conclusion, financial literacy is a crucial driver of economic growth by empowering individuals to make informed financial decisions, leading to increased savings, responsible borrowing, and productive investment. By fostering a financially literate population, societies can unlock their economic potential and achieve sustainable prosperity.

Overcoming Barriers to Financial Literacy

Financial literacy is the ability to understand and manage your finances effectively. This includes things like budgeting, saving, investing, and managing debt. In today’s economy, financial literacy is more important than ever. With the rise of complex financial products and services, it is crucial to understand how money works and how to make informed financial decisions.

However, there are many barriers to financial literacy. These can include:

- Lack of access to financial education: Many people do not have access to quality financial education in school or in their communities. This can make it difficult to learn the basics of personal finance.

- Complexity of financial products and services: The financial industry is complex, and many people find it difficult to understand the different products and services available. This can lead to confusion and poor financial decisions.

- Fear and stigma: Some people are afraid to talk about money or seek help with their finances. This can prevent them from getting the education and support they need.

- Time constraints: Many people are busy with work, family, and other commitments. This can make it difficult to find the time to learn about personal finance.

Despite these challenges, there are a number of things that can be done to overcome barriers to financial literacy. These include:

- Providing access to financial education: Governments, schools, and community organizations can play a role in providing access to financial education for all. This can be done through online resources, workshops, and community programs.

- Simplifying financial products and services: The financial industry can make it easier for people to understand financial products and services by providing clear and concise information. This can include using plain language and providing easy-to-understand explanations.

- Creating a culture of financial literacy: Financial literacy should be a priority for everyone, not just those who are struggling. This can be achieved by encouraging open conversations about money and by providing resources and support to those who need it.

Overcoming barriers to financial literacy is essential for a healthy economy. When people are financially literate, they are better equipped to make informed decisions about their money, save for the future, and achieve their financial goals.

{kind=link}