In today’s complex financial landscape, understanding the importance of your credit score is paramount. Your credit score, a numerical representation of your creditworthiness, acts as a cornerstone for securing various financial products and services, from loans and mortgages to credit cards and insurance. It’s a vital indicator of your financial health, influencing everything from interest rates to loan approval.

Beyond personal finance, credit scores play a significant role in maintaining the stability of the financial system. Lenders rely heavily on credit scores to assess risk and make informed lending decisions. A robust credit system, underpinned by reliable credit scores, promotes responsible borrowing and lending, ultimately contributing to a more stable financial environment.

What Is a Credit Score?

A credit score is a numerical representation of your creditworthiness, which is how likely you are to repay your debts on time. It is a three-digit number that ranges from 300 to 850, with higher scores indicating better creditworthiness. Credit scores are calculated using information from your credit report, which is a detailed record of your borrowing and repayment history. This information includes things like:

- Payment history: Whether you have made payments on time, missed payments, or defaulted on loans.

- Credit utilization: The amount of credit you are using compared to the total amount of credit available to you.

- Credit mix: The different types of credit you have, such as credit cards, auto loans, and mortgages.

- Length of credit history: How long you have been using credit.

- New credit: How recently you have opened new credit accounts.

Your credit score plays a crucial role in your financial life, affecting your ability to access credit, secure loans, and even get a job. Lenders use your credit score to assess your risk as a borrower and determine whether to approve your loan application and at what interest rate.

How Credit Scores Are Calculated

Your credit score is a numerical representation of your creditworthiness. It’s a three-digit number that lenders use to assess the risk of lending you money. The higher your score, the lower the risk you are considered to be, which translates to lower interest rates and better loan terms. There are several different credit scoring models, but the most commonly used is the FICO score.

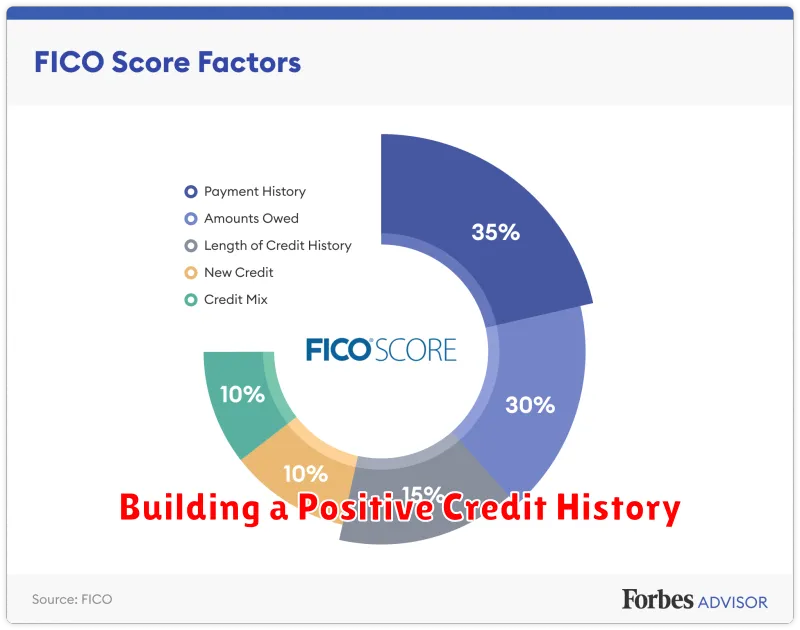

Your FICO score is calculated based on five key factors:

- Payment history (35%): This is the most important factor, as it reflects your ability to pay your bills on time. Late payments, missed payments, and collections can all negatively impact your score.

- Amounts owed (30%): This factor looks at how much debt you have relative to your available credit. Having a high credit utilization ratio (the percentage of your available credit that you’re using) can lower your score.

- Length of credit history (15%): A longer credit history generally indicates a more responsible borrower.

- Credit mix (10%): Having a mix of different types of credit, such as credit cards, loans, and mortgages, shows lenders that you can manage different types of debt.

- New credit (10%): Applying for a lot of new credit in a short period can lower your score, as it can signal to lenders that you are taking on more debt.

Your credit score is constantly changing based on your financial behavior. It’s important to understand how your credit score is calculated so you can take steps to improve it. This can include paying your bills on time, keeping your credit utilization low, and avoiding unnecessary new credit applications.

Factors That Influence Your Credit Score

Your credit score is a numerical representation of your creditworthiness, which plays a significant role in your financial stability. Lenders use your credit score to assess your ability to repay borrowed money, influencing the interest rates and loan terms you receive. Several factors contribute to your credit score, and understanding these factors empowers you to maintain a healthy score.

One of the most crucial factors is your payment history. This reflects your track record of making payments on time, whether it’s for credit cards, loans, or utility bills. Late or missed payments negatively impact your score, highlighting your potential for future defaults.

Another key factor is your credit utilization ratio, which represents the amount of credit you are using compared to your total available credit. A high utilization ratio, exceeding 30%, suggests you are heavily reliant on credit, increasing your risk in the eyes of lenders.

The length of your credit history matters as well. A longer credit history demonstrates your experience in managing credit responsibly. It indicates that you’ve had ample opportunity to build a solid track record and can be trusted to handle future debts.

The types of credit you use contribute to your credit score. A diverse credit portfolio, including credit cards, installment loans, and mortgages, indicates a more balanced approach to credit management and can positively impact your score.

Lastly, new credit inquiries, particularly hard inquiries from lenders, can temporarily lower your score. Hard inquiries indicate that you are seeking new credit, potentially suggesting increased financial strain or a desire for more debt.

By understanding these factors and taking proactive steps to maintain a positive credit score, you can significantly enhance your financial stability, access favorable loan terms, and ultimately improve your overall financial well-being.

The Importance of a Good Credit Score

Your credit score is a numerical representation of your creditworthiness, indicating how likely you are to repay borrowed money. This three-digit number plays a significant role in your financial stability, affecting your access to credit, interest rates, and even employment opportunities.

A good credit score unlocks various financial benefits. It allows you to qualify for loans with lower interest rates, saving you thousands of dollars in the long run. Lenders view individuals with good credit as reliable borrowers, making them eligible for better terms and conditions on loans, mortgages, and credit cards.

Furthermore, a strong credit score can even boost your chances of getting a job. Some employers conduct credit checks to gauge an applicant’s financial responsibility, considering it a reflection of their overall character. Having a positive credit history demonstrates your commitment to financial stability, which can make you a more attractive candidate.

Maintaining a good credit score requires responsible financial management. This includes paying bills on time, using credit responsibly, and keeping credit utilization low. By taking these proactive steps, you can build a solid credit history that will benefit you in numerous ways.

How Credit Scores Affect Loan Interest Rates

Your credit score plays a crucial role in determining the interest rate you’ll be offered on a loan. Lenders use your credit score to assess your creditworthiness, or the likelihood that you’ll repay your debts as agreed. A higher credit score indicates a lower risk to the lender, which translates into a lower interest rate for you. Conversely, a lower credit score signals a higher risk, leading to a higher interest rate.

Here’s a breakdown of how credit scores impact loan interest rates:

- High Credit Score (740 or above): You’re considered a low-risk borrower, eligible for the most favorable interest rates. Lenders are confident in your ability to repay, so they can offer lower rates to attract your business.

- Average Credit Score (670-739): You fall within the average risk range, and your interest rates will likely be higher than those offered to borrowers with excellent credit. However, you’ll still have access to loans with competitive rates.

- Low Credit Score (Below 670): You’re considered a high-risk borrower, facing the highest interest rates. Lenders see you as more likely to default on your loan, so they compensate for that risk by charging a higher rate.

It’s important to remember that interest rates are also influenced by other factors, such as the type of loan, the loan amount, and the current market conditions. However, your credit score remains a significant factor in determining the interest rate you’ll be offered.

Impact of Credit Scores on Renting and Employment

Credit scores play a crucial role in determining your financial stability. They are a numerical representation of your creditworthiness, based on your past borrowing and repayment history. A high credit score demonstrates responsible financial behavior, while a low credit score may indicate financial instability and risk.

Your credit score can significantly impact your ability to secure housing and employment. Landlords often use credit checks to assess a potential tenant’s financial responsibility. A good credit score increases your chances of being approved for an apartment and securing a desirable rental unit. Similarly, potential employers may review your credit score as a gauge of your financial reliability and overall responsibility. A low credit score may raise red flags and hinder your job prospects, particularly in industries that require financial accountability.

Consequences of a Low Credit Score

A credit score is a numerical representation of your creditworthiness, reflecting your ability to repay borrowed money. A low credit score can have serious financial consequences, impacting your ability to access essential financial services and potentially leading to higher borrowing costs.

One of the most significant consequences of a low credit score is higher interest rates on loans. Lenders view individuals with poor credit history as higher risk, leading them to charge higher interest rates to compensate for potential losses. This can significantly increase the overall cost of borrowing, making it more difficult to manage debt and achieve financial goals.

Furthermore, a low credit score can limit your access to credit products. Lenders may be unwilling to extend credit to individuals with poor credit history, making it challenging to secure loans, credit cards, or even mortgages. This can severely restrict your financial options, hindering your ability to make major purchases or invest in your future.

Beyond higher interest rates and limited access to credit, a low credit score can also affect your employment opportunities. Some employers, particularly in financial or security-sensitive roles, may conduct credit checks as part of the hiring process. A poor credit history could potentially raise red flags and impact your chances of securing employment.

It’s crucial to maintain a healthy credit score by paying your bills on time, keeping credit utilization low, and avoiding unnecessary credit inquiries. By proactively managing your credit, you can mitigate the negative consequences of a low credit score and secure a more stable financial future.

Strategies for Improving Your Credit Score

A good credit score is crucial for financial stability. It influences your ability to access loans, mortgages, and other financial products at favorable rates. If you’re looking to improve your credit score, here are some effective strategies:

Pay your bills on time: This is the most important factor in building a good credit score. Set up reminders or automate payments to avoid late payments.

Reduce your credit utilization ratio: Aim to keep your credit utilization ratio below 30%. This means using less than 30% of your available credit.

Avoid opening too many new accounts: Each hard inquiry from a credit application can lower your score. Only apply for credit when you truly need it.

Become an authorized user on a responsible account: Being an authorized user on a credit card with a long history of on-time payments can benefit your credit score.

Dispute any errors on your credit report: Check your credit report for inaccuracies and dispute them with the credit bureaus.

Consider a secured credit card: A secured credit card requires a security deposit, which can help you build credit if you have limited credit history.

Be patient: Building a strong credit score takes time and consistent effort. Don’t get discouraged if you don’t see immediate results. By following these strategies and making responsible financial decisions, you can improve your credit score and achieve your financial goals.

Monitoring Your Credit Report for Errors

Your credit score is a crucial factor in securing loans, mortgages, and even some job opportunities. It’s a reflection of your financial history and responsibility, influencing the interest rates you qualify for and the overall cost of borrowing. A high credit score is essential for financial stability, allowing you to access favorable loan terms and build a strong financial foundation. However, inaccuracies in your credit report can significantly impact your score, potentially hindering your financial goals.

That’s why it’s vital to monitor your credit report regularly for errors. Mistakes can occur due to identity theft, data entry errors, or even outdated information. These inaccuracies can lead to a lower credit score, making it challenging to secure loans or even get approved for credit cards. By proactively reviewing your credit report, you can identify and rectify any errors, ensuring that your score accurately reflects your financial standing.

You are entitled to a free credit report from each of the three major credit bureaus – Equifax, Experian, and TransUnion – annually through AnnualCreditReport.com. Take advantage of this opportunity to review your report for any inconsistencies or inaccuracies. If you find errors, you can dispute them with the credit bureau and provide supporting documentation to correct the information. By addressing these mistakes, you can protect your credit score and maintain financial stability.

Building a Positive Credit History

A positive credit history is crucial for achieving financial stability. It’s a reflection of your ability to manage debt responsibly and serves as a foundation for accessing various financial products and services. Building a strong credit history is a continuous process that involves consistent responsible financial behavior.

Here are some key steps to building a positive credit history:

- Start Early: Establish a credit history by opening a credit card or taking out a loan, even if it’s a small amount. This allows lenders to track your payment behavior.

- Pay Bills on Time: Consistency is key. Make all payments promptly, whether it’s for credit cards, loans, utilities, or rent. Late payments negatively impact your credit score.

- Keep Credit Utilization Low: Aim to use less than 30% of your available credit limit. High credit utilization can raise concerns about your debt management.

- Avoid Opening Too Many Accounts: While diversifying your credit sources is beneficial, opening too many accounts in a short period can negatively impact your score.

- Monitor Your Credit Reports Regularly: Check your credit reports from all three credit bureaus (Experian, Equifax, and TransUnion) for errors.

- Consider Secured Credit Cards: If you struggle to qualify for a traditional credit card, secured cards offer a starting point. They require a security deposit, which acts as collateral.

Building a positive credit history requires patience and commitment. By following these steps, you can establish a solid foundation for achieving financial stability. Remember, a strong credit history opens doors to better interest rates, loan approvals, and overall financial security.

Maintaining Financial Stability Through Responsible Credit Use

In today’s world, credit scores are often seen as the gatekeeper to financial stability. They play a significant role in determining your access to loans, credit cards, and even job opportunities. While a high credit score can open doors to favorable financial terms, a low score can limit your options and create challenges in managing your finances.

Maintaining financial stability through responsible credit use is paramount. It involves understanding how your credit score is calculated and taking steps to improve it. This can be achieved by:

- Paying your bills on time: This is the most crucial factor in your credit score. Late payments can negatively impact your score, making it difficult to obtain future credit.

- Keeping your credit utilization low: A high credit utilization ratio, which is the amount of credit you’re using compared to your total credit limit, can hurt your score. Aim to keep your utilization below 30%.

- Managing your debt responsibly: Excessive debt can lower your credit score. Focus on paying down debt and avoid accumulating more than you can comfortably handle.

- Monitoring your credit report regularly: Errors on your credit report can damage your score. It’s essential to review your credit report at least once a year to ensure accuracy.

Responsible credit use goes beyond simply having a good credit score. It’s about making informed financial decisions and maintaining a healthy relationship with credit. By understanding your credit score and implementing responsible credit management practices, you can pave the way towards financial stability and achieve your financial goals.

{kind=link}