Planning for your child’s education can feel overwhelming, but it’s one of the most important investments you can make in their future. A good education opens doors to countless opportunities, from higher earning potential to a fulfilling career. With careful planning and smart saving strategies, you can ensure your child receives the education they deserve without weighing down your finances. This guide offers valuable tips to help you navigate the path towards a successful educational journey for your child.

From understanding the cost of college to exploring various savings options, we’ll cover everything you need to know about planning and saving for your child’s education. We’ll also discuss the different types of financial aid available and highlight crucial factors like starting early, maximizing contributions, and making informed decisions. Whether you’re just beginning to think about your child’s future education or are ready to take concrete steps, this article provides valuable insights and actionable advice to guide you through the process.

Estimating Future Education Costs

One of the first steps in planning for your child’s education is understanding the costs involved. Tuition, fees, room and board, books, and other expenses can add up quickly, and these costs are likely to rise over time. Luckily, there are several tools available to help you estimate future education costs.

A helpful resource is the College Board’s “Trends in College Pricing”. This report provides data on average tuition and fees at public and private colleges and universities nationwide. You can also use online calculators, such as those offered by Savingforcollege.com and Unigo, to estimate the cost of attending specific schools.

When estimating future costs, it’s important to consider the following factors:

- Inflation: The cost of education is expected to rise over time, so factor in inflation when estimating future costs.

- Type of institution: Public universities generally have lower tuition rates than private colleges.

- Location: The cost of living and tuition can vary depending on the school’s location.

- Program of study: Some majors may be more expensive than others.

By carefully considering these factors and using available resources, you can get a realistic estimate of the cost of your child’s education. This information will help you develop a savings plan that will ensure your child has the financial resources they need to pursue their educational goals.

Starting Early: The Power of Compound Interest

One of the most powerful tools in saving for your child’s education is the magic of compound interest. This simple concept, where interest earned on your savings also earns interest, can work wonders over time. Imagine planting a seed that grows into a tree, which then produces more seeds. Compounding works the same way, with your initial investment growing exponentially over the years.

Let’s say you start saving $100 per month for your child’s education when they are born, earning a modest 7% annual return. By the time your child turns 18, you’ll have accumulated over $50,000, even though you only invested around $21,600. That’s the power of compounding in action! The earlier you start, the more time your money has to grow, leading to significantly larger savings.

The longer your money has to compound, the greater the impact. Starting early means you can take advantage of this exponential growth. You’ll be amazed at how a small, consistent investment can turn into a substantial amount for your child’s future.

Exploring Different College Savings Plans (529 Plans, ESAs)

Saving for college can seem daunting, but there are tools available to help you reach your financial goals. Two popular options are 529 plans and Education Savings Accounts (ESAs), each offering unique benefits and considerations.

529 Plans

529 plans are state-sponsored investment accounts that offer tax advantages for saving for college. Contributions grow tax-deferred, and withdrawals for qualified educational expenses are tax-free at the federal level. Each state has its own 529 plan with varying investment options and fees.

Benefits:

- Tax-free growth and withdrawals

- Wide range of investment choices

- Flexibility to change beneficiaries

Considerations:

- State residency requirements may apply

- Penalties may apply for non-educational withdrawals

- Investment performance can fluctuate

Education Savings Accounts (ESAs)

Education Savings Accounts (ESAs), previously known as Coverdell Education Savings Accounts, are similar to 529 plans but have a lower contribution limit. These accounts offer tax advantages for qualified educational expenses, including tuition, fees, books, and supplies.

Benefits:

- Tax-deductible contributions (subject to income limitations)

- Tax-free withdrawals for qualified expenses

- Flexibility to use for K-12 education as well

Considerations:

- Income limitations for contributions

- Lower contribution limit compared to 529 plans

- Penalties for non-educational withdrawals

When choosing between 529 plans and ESAs, consider factors like your income, state residency, investment preferences, and future educational goals. It’s crucial to research and compare different plans to find the best fit for your family’s needs.

Understanding the Tax Advantages of Education Savings Accounts

One of the most popular ways to save for your child’s education is through an Education Savings Account (ESA), also known as a 529 plan. ESAs offer significant tax advantages, making them a powerful tool for parents and guardians looking to build a college fund.

Tax-Deferred Growth: Earnings on investments within an ESA grow tax-deferred. This means you don’t have to pay taxes on the interest, dividends, or capital gains until the money is withdrawn for qualified educational expenses. This compounding effect can significantly increase your savings over time.

Tax-Free Withdrawals: When you use the money from an ESA for qualified education expenses, the withdrawals are tax-free at the federal level. This is a major benefit, as it allows you to keep more of your hard-earned money for your child’s education.

State Tax Benefits: Many states offer additional tax breaks for contributions to ESAs. These can include state income tax deductions or credits. Be sure to check your state’s specific regulations to see if you qualify for any benefits.

Contribution Limits: There are annual contribution limits for ESAs, so it’s important to plan accordingly. The current annual limit is $2,000 per beneficiary. However, you can often contribute a larger lump sum upfront, subject to the lifetime limit.

Flexibility: ESAs can be used for a wide range of qualified educational expenses, including tuition, fees, room and board, books, and supplies. This flexibility makes them a valuable tool for planning for both undergraduate and graduate education.

Potential for Higher Returns: ESAs often allow investments in a variety of assets, including stocks, bonds, and mutual funds. This can provide the potential for higher returns compared to traditional savings accounts.

Overall, ESAs offer substantial tax advantages that can make them a highly effective tool for saving for your child’s education. Their tax-deferred growth, tax-free withdrawals, and potential for higher returns can help you build a significant college fund over time.

Setting Realistic Savings Goals

The cost of education is rising steadily, making it crucial to start saving early. Setting realistic savings goals is essential for achieving your financial objectives. Here’s a breakdown of how to approach this:

Estimate College Costs: Begin by researching the estimated tuition, fees, room, and board expenses for colleges you’re considering. Utilize resources like the College Board and individual college websites for accurate figures. Remember to factor in inflation, which can significantly impact costs over time.

Consider Your Financial Situation: Evaluate your current income, expenses, and existing debt. Assess how much you can realistically contribute to your child’s education fund without jeopardizing your own financial stability. Aim for a sustainable savings rate that aligns with your budget.

Set SMART Goals: Use the SMART goal-setting framework: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, “Save $5,000 per year for the next 10 years to reach a total of $50,000.” This helps you stay focused and motivated.

Factor in Potential Aid and Scholarships: Research potential sources of financial aid, such as grants, scholarships, and student loans. These can significantly reduce your out-of-pocket costs. Consider setting aside a portion of your savings for these potential contingencies.

Adjust and Review Regularly: Life throws curveballs. Adjust your savings goals as needed based on changes in income, expenses, or your child’s educational aspirations. Review your progress periodically and make adjustments to stay on track.

Creating a Budget and Automating Contributions

One of the most important steps in saving for your child’s education is creating a budget and automating your contributions. By setting a specific amount to save each month, you can ensure that you’re consistently contributing to your child’s future.

To create a budget, start by tracking your monthly income and expenses. Once you have a clear picture of your financial situation, you can identify areas where you can cut back to free up more money for savings. Consider setting a specific goal for your child’s education fund, such as saving a certain amount by the time they start college. Then, break that goal down into smaller, monthly savings targets. This will make the goal feel more achievable.

Automating your contributions is another effective strategy. By setting up automatic transfers from your checking account to your savings account, you can ensure that you’re regularly contributing to your child’s education fund without having to manually do it each month. This also helps you avoid the temptation to spend the money on something else. There are many tools and platforms available to help you automate contributions, including online banking platforms, investment apps, and robo-advisors. Choose the option that best suits your needs and preferences.

Exploring Financial Aid Options and Scholarships

As you plan for your child’s education, it’s essential to explore various financial aid options and scholarships that can significantly reduce the overall cost.

Financial aid encompasses grants, loans, and work-study programs. Grants are free money that does not need to be repaid. Loans must be repaid with interest, but they can be a valuable tool for covering education expenses. Work-study programs offer part-time employment opportunities on campus, allowing students to earn money while gaining experience.

Scholarships are another crucial source of funding. They are awarded based on various factors, including academic merit, extracurricular activities, community service, and financial need.

Here are some tips for exploring financial aid and scholarships:

- Start early: Begin researching options early in your child’s high school career to avoid missing deadlines.

- Utilize the Free Application for Federal Student Aid (FAFSA): The FAFSA determines your eligibility for federal grants, loans, and work-study programs.

- Explore state and institutional aid: Many states and colleges offer scholarships and grants specific to their residents or institutions.

- Seek guidance from your child’s high school counselor or college admissions office: They can provide valuable insights into available resources and application processes.

- Leverage online scholarship databases: Several websites, such as Scholarships.com, Fastweb, and Cappex, compile scholarship opportunities from various sources.

- Target niche scholarships: Research scholarships focused on specific fields of study, cultural backgrounds, or personal experiences.

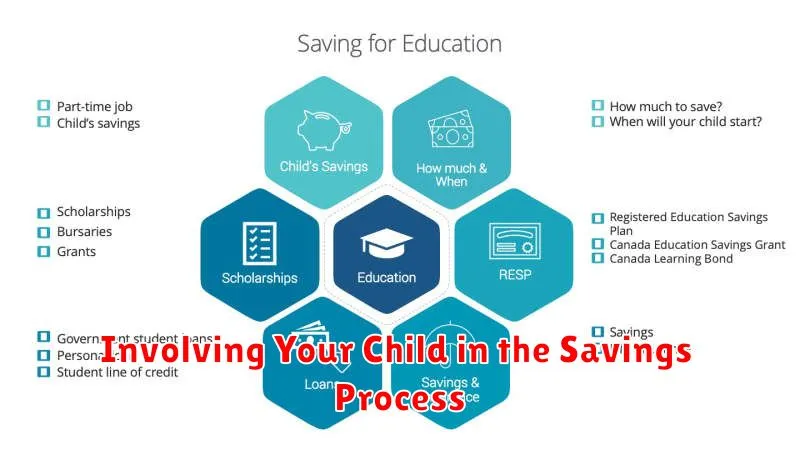

Involving Your Child in the Savings Process

Teaching children about money and saving early on can be beneficial for their future financial well-being. Here are some ways to involve your child in the savings process:

Explain the importance of saving: Make it clear why saving money is important for their education. Talk about the costs involved and how saving can help them achieve their educational goals.

Set up a visual savings goal: Use a chart, piggy bank, or online savings tracker to visually represent their progress towards their education savings goal. This can help them stay motivated and engaged.

Involve them in budgeting: Teach them about budgeting by giving them a small allowance or helping them allocate their own earnings from chores. This can help them learn about spending and saving decisions.

Let them participate in making investment choices: Depending on their age, you can involve them in the process of choosing investment options for their education savings. This can help them learn about different investment strategies and the potential risks and rewards.

Encourage them to set financial goals: Help them identify short-term and long-term financial goals, such as buying books or taking a course. This can motivate them to save and achieve their goals.

Celebrate milestones: When they reach a savings milestone, celebrate their achievement. This will help them feel proud of their progress and encourage them to continue saving.

Investing Wisely for Long-Term Growth

When planning for your child’s education, it’s crucial to think about long-term growth. This means choosing investments that will potentially increase in value over time, helping to offset the rising cost of education. Instead of focusing on short-term gains, prioritize investments that offer a strong foundation for your child’s future.

Consider these strategies for wise investing:

- Diversify your portfolio: Spreading your investments across different asset classes, like stocks, bonds, and real estate, can help manage risk. This reduces the impact of any single investment performing poorly.

- Invest in low-cost index funds: These funds track specific market indexes, offering broad exposure at a lower cost than actively managed funds. They can be a great option for long-term growth, particularly for those who are new to investing.

- Explore 529 plans: These college savings plans offer tax advantages and are designed specifically for educational expenses. Contributions often grow tax-deferred, and withdrawals are tax-free when used for qualified education costs.

Remember, investing is not a get-rich-quick scheme. Patience and a long-term mindset are essential. Review your investments periodically and adjust them as needed to stay aligned with your financial goals and your child’s evolving educational needs.

Providing a Solid Foundation for Your Child’s Future

One of the greatest gifts you can give your child is a solid education. It’s the foundation for a successful and fulfilling life, opening doors to countless opportunities. While the road to higher education can seem long and expensive, starting early and planning strategically can make the journey much smoother. This means focusing on both financial planning and academic support, creating a nurturing environment for your child’s educational journey.

Financial planning for your child’s education is crucial. Start by establishing a dedicated savings plan, even if it’s just a small amount. Explore options like 529 plans, which offer tax advantages for college savings. Consider taking advantage of any employer-sponsored education savings programs. Remember, consistency is key – make saving a regular habit and don’t let life’s ups and downs derail your goals.

Alongside financial planning, nurture your child’s academic growth. Encourage a love for learning from a young age. Support their interests, provide access to books and educational resources, and engage them in stimulating activities. Early exposure to a wide range of subjects and experiences will help them develop a strong foundation for future learning. By investing in your child’s education, you’re not just securing their future; you’re empowering them to reach their full potential.

{kind=link}