Are you looking for ways to maximize your savings and make your money work harder for you? Then understanding compound interest is essential. Compound interest, often referred to as the “eighth wonder of the world,” is a powerful tool that can significantly boost your wealth over time. But what exactly is compound interest, and how can it impact your savings?

This article will delve into the world of compound interest, explaining how it works, its benefits, and how you can leverage its power to achieve your financial goals. We’ll explore real-life examples, strategies to maximize your compound interest gains, and the importance of starting early. Get ready to unlock the potential of compound interest and learn how it can transform your financial future.

What is Compound Interest?

Compound interest is the eighth wonder of the world. It is the snowball effect of money, where you earn interest not only on your initial principal amount but also on the accumulated interest from previous periods. This means that your money grows exponentially over time, like a snowball rolling downhill.

Imagine you invest $1,000 in a savings account with a 5% annual interest rate. In the first year, you’ll earn $50 in interest (5% of $1,000). In the second year, you’ll earn interest not only on the original $1,000 but also on the $50 earned in the first year. This means you’ll earn $52.50 in interest (5% of $1,050). As time goes on, your interest earnings continue to compound, leading to significant growth in your savings.

The power of compound interest lies in its ability to accelerate your wealth accumulation. The longer your money stays invested, the more it compounds, and the faster it grows. It’s a powerful tool for achieving your financial goals, whether it’s buying a house, retiring comfortably, or reaching financial freedom.

How Compound Interest Works

Compound interest is a powerful force that can significantly grow your savings over time. It works by earning interest not only on your initial investment but also on the accumulated interest from previous periods. This means your money starts to grow exponentially, like a snowball rolling downhill.

Imagine you invest $1,000 at a 5% annual interest rate. In the first year, you’ll earn $50 in interest. In the second year, you’ll earn interest on your initial $1,000 and also on the $50 you earned in the first year. This means your total interest earned for the second year will be more than $50, resulting in even faster growth.

The key to maximizing the benefits of compound interest is to let your money work for you for as long as possible. The longer your money is invested and the higher the interest rate, the greater the impact of compounding.

Here’s a simple analogy: imagine a tree. The initial deposit is the seed, the interest rate is the sunlight and water, and the time is the growth. The longer the tree grows, the larger and stronger it becomes. The same goes for your money.

Compounding is the magic of long-term investing. It’s the secret to achieving financial goals like retirement planning, buying a home, or building wealth. By understanding how compound interest works, you can harness its power to reach your financial aspirations.

The Rule of 72

The Rule of 72 is a simple yet powerful tool for estimating how long it will take for your investment to double in value. It’s based on the concept of compound interest, where earnings are reinvested and start generating their own earnings.

To use the Rule of 72, simply divide 72 by the expected annual rate of return. For example, if you expect to earn a 10% return per year, it will take approximately 72 / 10 = 7.2 years for your investment to double.

The Rule of 72 is a helpful mental shortcut for understanding the impact of compound interest on your savings. It highlights that even small differences in returns can make a big difference over time.

Here are some additional things to keep in mind about the Rule of 72:

- It’s an estimate and not a precise calculation.

- It applies to compounding interest, where interest is earned on both the original investment and accumulated interest.

- It can be used to understand how long it will take for inflation to halve the value of your money.

By understanding the power of compound interest and the Rule of 72, you can make informed decisions about your savings and investments, setting yourself up for a more secure financial future.

The Power of Time with Compound Interest

Compound interest is a powerful tool that can help you grow your savings exponentially over time. It’s the interest earned on your initial investment, as well as the interest earned on the accumulated interest. Think of it as your money working for you and earning more money. The longer you let your money compound, the more significant the impact becomes.

The beauty of compound interest lies in its exponential growth. The earlier you start investing and the longer you let your money compound, the greater the returns you can expect. Even small amounts invested regularly can accumulate into a substantial sum over time. This principle is often referred to as the “power of time” when it comes to investing.

Let’s illustrate with an example. Imagine you invest $1,000 at an annual interest rate of 5%. After one year, you’ll have $1,050. In the second year, the 5% interest is calculated not just on the initial $1,000 but also on the $50 you earned in the first year. This compounding effect continues year after year, leading to a significant increase in your savings over time.

Understanding the power of compound interest is crucial for any individual looking to achieve their financial goals. By starting early, investing consistently, and letting your money compound, you can unlock the potential to achieve substantial wealth over the long term.

Compound Interest vs. Simple Interest

Understanding the difference between simple interest and compound interest is crucial when it comes to maximizing your savings. Simple interest is calculated only on the principal amount, while compound interest is calculated on both the principal amount and the accumulated interest. This means that with compound interest, your money grows exponentially over time.

Let’s illustrate with an example: imagine you invest $1,000 at a 5% interest rate. With simple interest, you would earn $50 in interest each year. However, with compound interest, your interest earnings are added back to the principal each year, so you start earning interest on your interest. This compounding effect leads to significantly higher returns in the long run.

Here’s a breakdown of how the two types of interest work:

- Simple Interest: Interest is calculated only on the principal amount. The formula is: Interest = Principal x Rate x Time.

- Compound Interest: Interest is calculated on the principal amount and the accumulated interest. The formula is: A = P(1 + r/n)^(nt), where A is the final amount, P is the principal amount, r is the interest rate, n is the number of times interest is compounded per year, and t is the time in years.

The power of compound interest becomes even more evident over longer periods. As the interest earned compounds, the growth accelerates, creating a snowball effect. This is why starting early and letting your investments grow through compounding is often considered the most effective way to build wealth.

Factors Affecting Compound Interest

Compound interest is a powerful tool for wealth building. It works by earning interest on both your principal and accumulated interest. However, the amount of compound interest you earn depends on several factors. Here are some key factors that affect compound interest:

Principal Amount: The higher the principal amount, the more interest you will earn. This is a simple concept: the more money you invest, the more money you will make.

Interest Rate: The interest rate is the percentage at which your money grows. A higher interest rate will lead to faster growth of your savings.

Compounding Frequency: The more often your interest is compounded, the faster your money will grow. For example, interest compounded daily will grow faster than interest compounded annually.

Time: Time is the most important factor in compound interest. The longer you leave your money invested, the more time it has to grow. The magic of compound interest works over the long term.

Inflation: While compound interest helps your money grow, inflation can erode its purchasing power. If inflation is high, your savings may not grow as fast as the cost of goods and services.

Fees and Taxes: Fees and taxes can eat into your returns and reduce the effectiveness of compound interest. Be sure to factor these costs into your calculations.

Calculating Compound Interest

Compound interest is the interest earned on both the principal amount and the accumulated interest. This means that your money grows exponentially over time, as you earn interest on your interest. It’s the magic of compounding that makes it a powerful tool for building wealth.

To calculate compound interest, you’ll need the following information:

- Principal (P): The initial amount of money you invest.

- Interest Rate (r): The annual interest rate, expressed as a decimal.

- Number of Times Interest is Compounded (n): The number of times interest is calculated and added to the principal each year.

- Time (t): The number of years the money is invested.

The formula to calculate compound interest is:

A = P(1 + r/n)^(nt)

Where:

- A is the future value of the investment/loan, including interest

Let’s break down the formula with an example:

You invest $1,000 at an annual interest rate of 5%, compounded annually for 10 years. Using the formula above:

A = 1000(1 + 0.05/1)^(1*10)

A = 1000(1.05)^10

A = $1,628.89

This means that after 10 years, your initial investment of $1,000 will grow to $1,628.89 due to the power of compounding.

By understanding the formula and the key factors involved, you can calculate the potential growth of your savings and make informed decisions about your investments.

Maximizing Your Savings with Compound Interest

Compound interest is the eighth wonder of the world. He who understands it, earns it… he who doesn’t… pays it. This quote emphasizes the power of compound interest. While the concept is simple, its impact on your savings can be truly transformative. It’s essentially “interest on interest,” where earnings from your initial investment are reinvested, generating further interest. To maximize your savings, consider these strategies:

Start Early: The earlier you begin investing, the more time your money has to grow. The magic of compounding works wonders over extended periods. Even small contributions over a long time can accumulate into substantial wealth.

Maximize Your Contribution: Increase your savings contributions whenever possible. Even modest increases can have a significant impact. If you’re eligible for employer matching contributions, take advantage of them. It’s free money you’re leaving on the table if you don’t.

Invest in High-Yield Accounts: Seek out accounts with favorable interest rates. Explore options like high-yield savings accounts, certificates of deposit (CDs), or investment accounts that provide solid returns. Consider diversifying your portfolio to mitigate risk.

Avoid Withdrawals: Withdrawals disrupt the compounding process. Try to limit unnecessary withdrawals and maintain a long-term perspective. Remember, the goal is to let your money grow over time.

Compounding is a powerful force that can significantly boost your savings. By understanding its principles and employing these strategies, you can set yourself up for a financially secure future.

Common Examples of Compound Interest in Action

Compound interest is the eighth wonder of the world. He who understands it, earns it… he who doesn’t… pays it. – Albert Einstein.

While the concept of compound interest may sound complex, it’s a powerful force that works silently in our everyday lives. Here are some common examples of compound interest in action:

- Savings Accounts: When you deposit money into a savings account, the interest earned on your principal amount is added back to your account. This new principal amount then earns interest in the next period, leading to a snowball effect. The higher the interest rate and the longer you leave your money in the account, the greater the impact of compound interest.

- Retirement Funds: Retirement accounts, like 401(k)s and IRAs, often utilize compound interest. Regular contributions combined with interest growth create a significant amount over time. The power of compound interest is especially evident in retirement savings, as you have decades for your investments to grow.

- Mortgages: While not as exciting as earning interest, compound interest also works against you when you have a mortgage. The interest on your outstanding balance is added to the principal, increasing your total debt. Early repayment and higher payments can minimize the impact of compound interest on your mortgage.

- Credit Cards: Credit cards are infamous for charging high interest rates. If you carry a balance, the interest charges compound over time, significantly increasing your debt. This is why it’s crucial to pay off your credit card balance in full each month to avoid the negative impact of compounding interest.

- Investments: Many investments, like stocks and bonds, grow in value through compounding. Over time, the dividends and capital gains earned on your investments are reinvested, leading to further growth. This is how investors can build wealth through the power of compound interest.

Understanding these examples will help you appreciate the power of compound interest. Whether you’re saving for the future, paying off debt, or investing for growth, harnessing the power of compound interest can make a significant difference in your financial well-being.

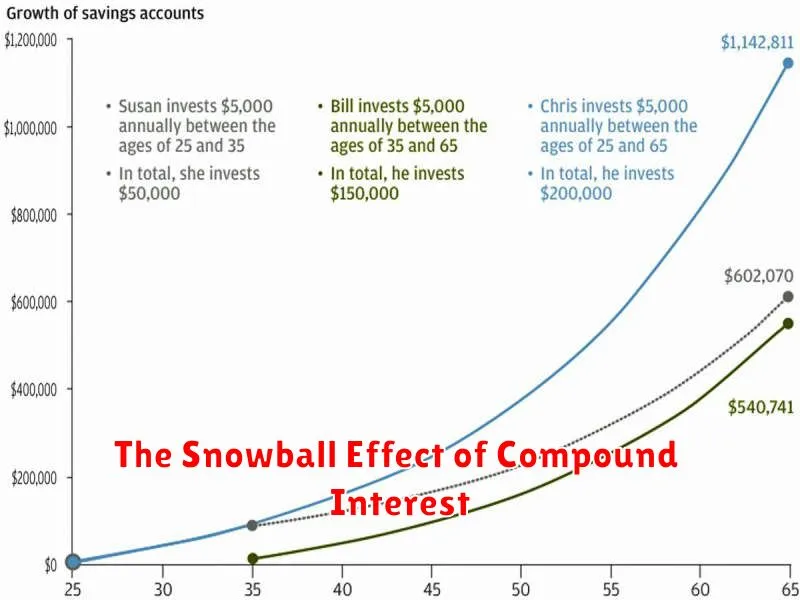

The Snowball Effect of Compound Interest

Compound interest is often called the “eighth wonder of the world” for a reason. It’s the power of earning interest on your initial investment, and then earning interest on that interest, and so on. This snowball effect can make your savings grow exponentially over time, even with small, consistent contributions.

Imagine you invest $1,000 at a 10% annual interest rate. After the first year, you’ll earn $100 in interest, bringing your total to $1,100. The following year, you’ll earn interest on that $1,100, which means you’ll earn $110. This pattern continues, and as your principal grows, so does your interest earned. The key to maximizing compound interest is to invest early and consistently, allowing time for your money to work for you and grow exponentially.

The snowball effect of compound interest is most powerful over longer periods. The earlier you start investing, the more time your money has to compound. While it may seem like small amounts won’t make a difference, the power of compounding can transform those small contributions into substantial wealth over time.

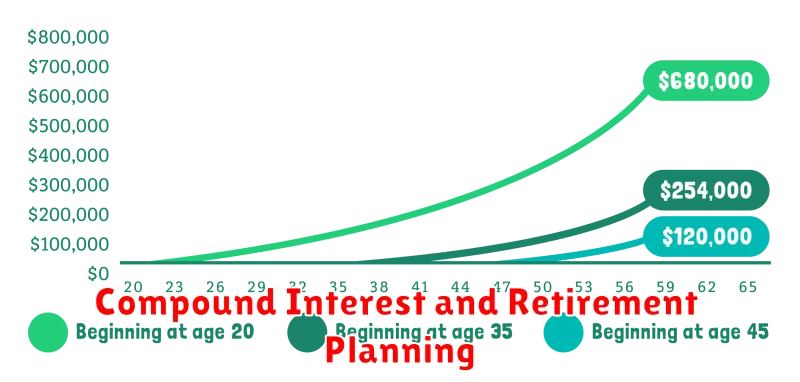

Compound Interest and Retirement Planning

Compound interest is one of the most powerful tools you can use to build wealth, especially when it comes to retirement planning. It’s the interest earned not only on your initial investment but also on the accumulated interest from previous periods. This means that your money grows exponentially over time, making it a key factor in achieving your retirement goals.

Imagine starting with a $10,000 investment and earning a 7% annual return. After the first year, you’ll have $10,700. In the second year, you’ll earn interest on both the initial $10,000 and the $700 interest earned in the first year. This compounding effect continues, accelerating your investment growth over the long term.

For retirement planning, compound interest works wonders because you have a long time horizon. Even small, consistent contributions can grow significantly over decades. Early investment and maximizing your contribution period will play a huge role in maximizing your retirement savings.

To leverage compound interest effectively in your retirement planning, consider:

- Start early: The longer your money has to compound, the more it will grow. The power of compound interest is truly amplified over long periods.

- Invest regularly: Consistent contributions, even small amounts, will accelerate your compounding returns.

- Seek higher returns: While it’s important to invest wisely, aiming for higher returns will boost your compound interest gains. However, always remember that higher returns often come with higher risk.

- Avoid unnecessary fees: High fees can significantly eat into your returns. Choose investment options with low fees to maximize your compounding potential.

Compound interest is a silent force multiplier for your retirement savings. By understanding and leveraging its power, you can set yourself up for a comfortable and secure future.

Avoiding Common Compound Interest Pitfalls

While compound interest is a powerful tool for growing your wealth, it’s essential to be aware of common pitfalls that can hinder its effectiveness. Understanding these pitfalls and taking proactive steps to avoid them will maximize the benefits of compounding.

One common pitfall is failing to make regular contributions. Compound interest thrives on consistent growth, and skipping contributions can disrupt this momentum. Setting up automatic transfers or adopting a disciplined savings schedule can help ensure regular contributions.

Another pitfall is withdrawing from your investments too early. While it’s tempting to access your savings for short-term needs, withdrawing funds before they’ve had time to compound significantly reduces their long-term potential. Consider alternative financing options or establish an emergency fund to avoid depleting your savings.

High fees and expenses can also erode the benefits of compound interest. Fees associated with investment accounts, mutual funds, or other financial products can eat into your returns. Researching low-cost investment options and minimizing unnecessary fees is crucial for maximizing your savings growth.

Finally, ignoring inflation can undermine the value of your savings. Inflation erodes the purchasing power of your money over time, diminishing the real returns you achieve through compound interest. Aim for investment returns that outpace inflation to preserve and grow the real value of your savings.

By avoiding these common pitfalls, you can harness the full power of compound interest and accelerate your path to financial success. Consistent savings, long-term investment horizons, mindful fee management, and inflation awareness are essential for achieving your financial goals through the magic of compounding.

{kind=link}